In July 2025, the price of Ether soared nearly 50%. Investors are focusing on stablecoins, asset tokenization, and institutional adoption—these areas are the core advantages that differentiate Ethereum as the oldest smart contract platform from its competitors.

The passing of the (GENIUS Act) is a milestone moment for stablecoins and the entire crypto asset class. While market structure-related legislation may still take time to pass in Congress, U.S. regulators can continue to support the development of the digital asset industry through other policy adjustments, such as approving staking features in crypto investment products.

In the short term, crypto asset valuations may experience consolidation, but we remain very optimistic about the outlook for this asset class in the coming months. Crypto assets offer investors the opportunity to engage with blockchain innovation, while potentially being somewhat immune to certain risks of traditional assets (such as the prolonged weakness of the dollar). Therefore, Bitcoin, ETH, and many other digital assets are expected to continue to be favored by investors.

On July 18, President Trump signed the (GENIUS Act), providing a comprehensive regulatory framework for U.S. stablecoins. This marks the 'end of the beginning' for the crypto asset class: public blockchain technology is moving from the experimental phase into the core of the regulated financial system. The debate over whether blockchain technology can bring tangible benefits to mainstream users has ended, and regulators have turned to ensuring that the industry grows while incorporating appropriate consumer protection and financial stability mechanisms.

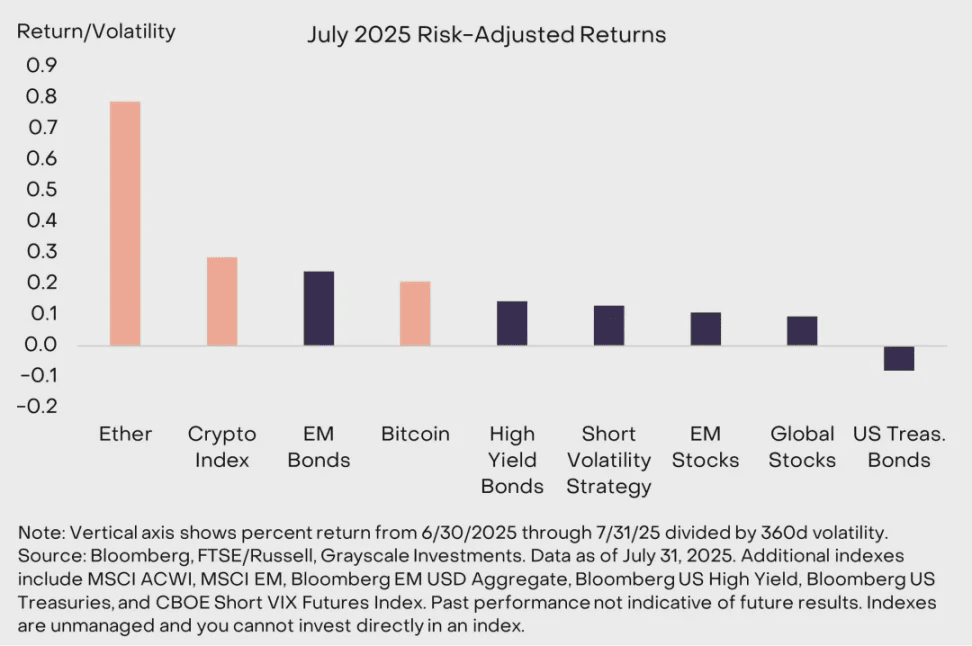

In July, the crypto market was buoyed by the passing of the (GENIUS Act) and also supported by favorable macro market conditions. Stock market indices rose in most parts of the world, and fixed-income market returns were led by high-risk sectors, such as U.S. high-yield corporate bonds and emerging market bonds (see Chart 1). As market volatility decreased, related investment strategies also performed quite well.

The FTSE/Grayscale Crypto Asset Market Index (an investable digital asset index weighted by market capitalization) rose by 15%, and the price of Bitcoin increased by 8%. Meanwhile, Ether's ETH became the star of the month, surging by 49%, with a cumulative increase of over 150% since the low in early April.

Also known as 'The Return of the King'

Also known as 'The Return of the King'

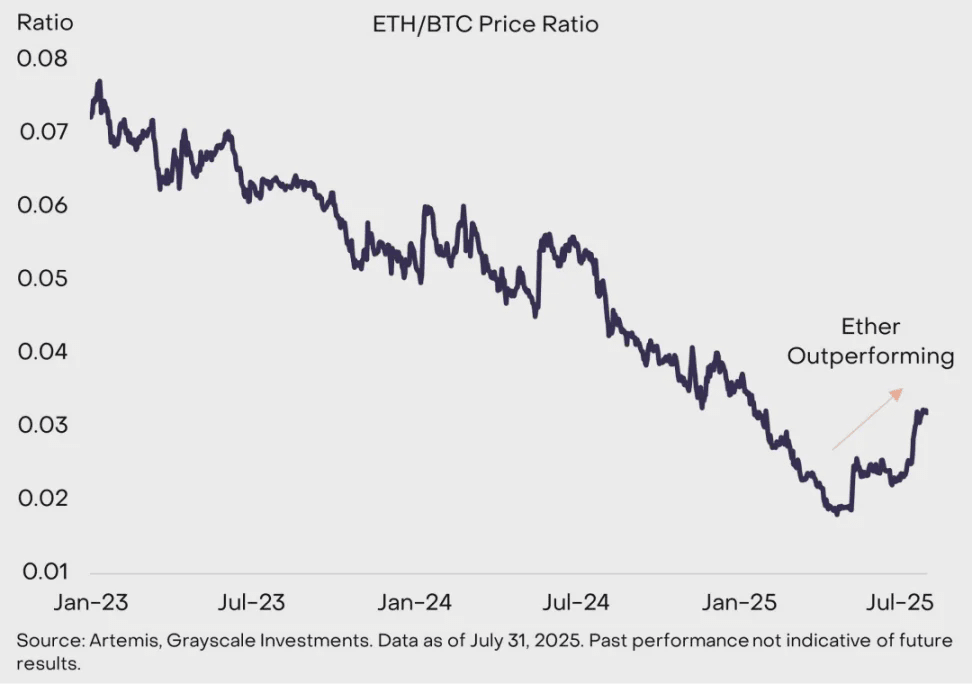

Ethereum is the largest smart contract platform by market capitalization and the infrastructure of blockchain finance. However, until recently, the price performance of ETH lagged far behind Bitcoin and even other smart contract platforms like Solana. This has led some to question Ethereum's development strategy and its competitive position in the industry (see Chart 2).

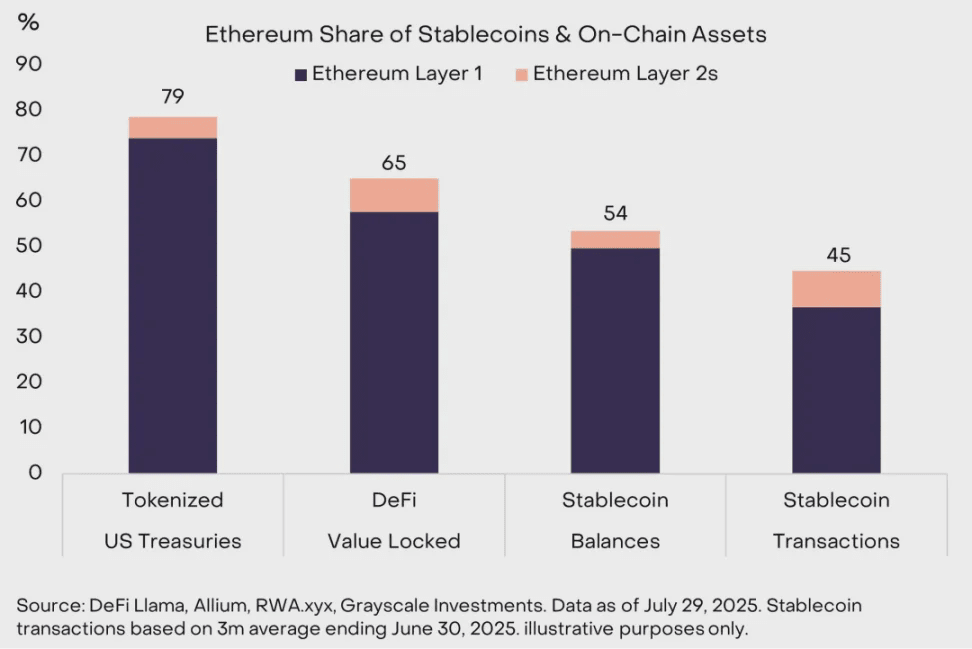

The renewed enthusiasm for Ethereum and ETH may reflect the market's focus on stablecoins, asset tokenization, and institutional blockchain adoption—these are Ethereum’s strengths (see Chart 3). For example, including its Layer 2 network, the Ethereum ecosystem holds over 50% of stablecoin balances and processes about 45% of stablecoin transactions (measured in U.S. dollar value).

The renewed enthusiasm for Ethereum and ETH may reflect the market's focus on stablecoins, asset tokenization, and institutional blockchain adoption—these are Ethereum’s strengths (see Chart 3). For example, including its Layer 2 network, the Ethereum ecosystem holds over 50% of stablecoin balances and processes about 45% of stablecoin transactions (measured in U.S. dollar value).

Ethereum is also the home of about 65% of the locked value in decentralized finance (DeFi) protocols and nearly 80% of tokenized U.S. Treasury products. For many agents building crypto projects, including Coinbase, Kraken, Robinhood, and Sony, Ethereum has always been the preferred network.

The increase in the adoption of stablecoins and tokenized assets will benefit Ethereum and other smart contract platforms. Grayscale Research believes that stablecoins can potentially disrupt certain areas of the global payments industry through lower costs, faster settlement times, and greater transparency (for more background information, see 'Stablecoins and Future Payments').

The increase in the adoption of stablecoins and tokenized assets will benefit Ethereum and other smart contract platforms. Grayscale Research believes that stablecoins can potentially disrupt certain areas of the global payments industry through lower costs, faster settlement times, and greater transparency (for more background information, see 'Stablecoins and Future Payments').

There are two sources of income related to stablecoins: first, the net interest margin (NIM) earned by stablecoin issuers (such as Tether and Circle), and second, the transaction fees earned by the blockchain processing transactions. Since Ethereum has already taken a leading position in the stablecoin space, its ecosystem seems poised to benefit from the growth in stablecoin adoption through higher transaction fees.

Tokenization (the process of bringing traditional assets on-chain) is similarly promising (for more background information, see 'Public Blockchains and the Tokenization Revolution'). Currently, the market size for tokenized assets is relatively small (around $12 billion), but the growth potential is enormous. Tokenized U.S. Treasuries are currently the largest category of tokenized assets, and Ethereum is the market leader. In the alternative asset space, Apollo Global recently partnered with Securitize to launch an on-chain credit fund.

Furthermore, the tokenized equity market, while small, is growing: Robinhood has launched tokenized shares of private companies such as SpaceX and OpenAI, and eToro also plans to tokenize stocks on Ethereum. Apollo's products are available on multiple blockchains, while Robinhood and eToro's tokenized equity products are within the Ethereum ecosystem.

The ETP craze and more trends

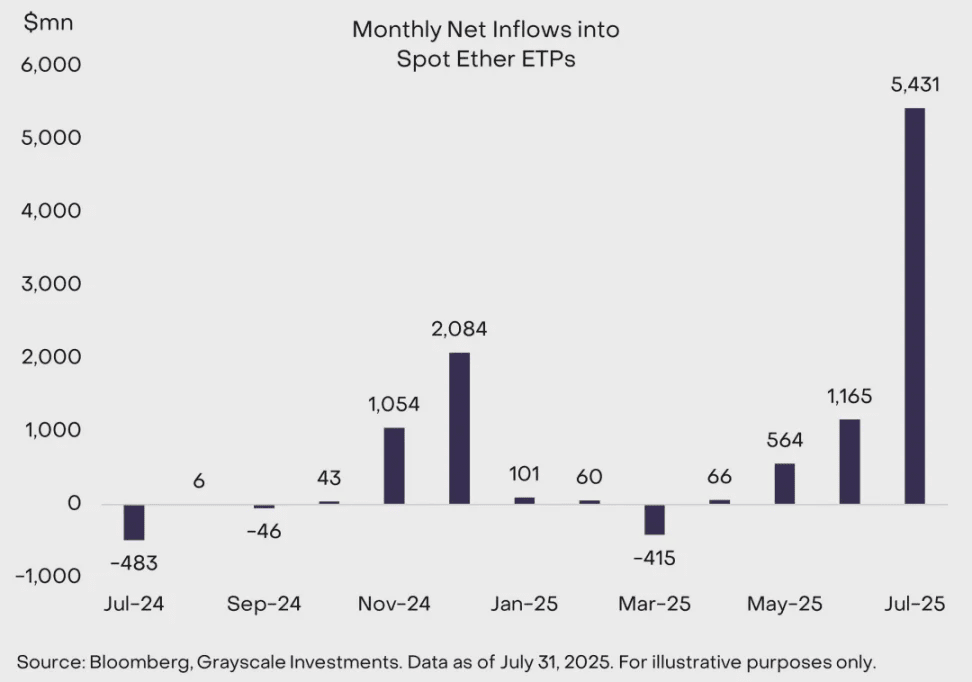

Investor interest in Ethereum has led to a significant net inflow into Ether spot ETPs. In July, the net inflow for Ether spot ETPs listed in the U.S. reached $5.4 billion, the largest single-month net inflow since these products were launched last year (see Chart 4).

Currently, Ether ETP holds about $21.5 billion in assets, equivalent to nearly 6 million ETH, accounting for about 5% of the total circulation. Based on data from the CFTC's trader holdings report, we estimate that only $1 billion to $2 billion of ETH ETP net inflows come from hedge fund 'basis trading,' with the rest being long-term capital.

Some listed companies have also begun accumulating ETH to gain token usage rights through equity instruments. The two companies that hold the most ETH among 'crypto asset management firms' are Bitmine Emersion Technologies ($BMNR) and SharpLink Gaming ($SBET). Together, these two companies hold over 1 million ETH, with a total value of $3.9 billion.

Some listed companies have also begun accumulating ETH to gain token usage rights through equity instruments. The two companies that hold the most ETH among 'crypto asset management firms' are Bitmine Emersion Technologies ($BMNR) and SharpLink Gaming ($SBET). Together, these two companies hold over 1 million ETH, with a total value of $3.9 billion.

The third listed company, BTCS ($BTCS), stated in late July that it plans to raise $2 billion through the issuance of common and preferred stock for additional purchases of ETH (BTCS currently holds about 70,000 ETH, valued at approximately $250 million). In addition to the net inflow of ETH ETP products, buying pressure from Ethereum enterprise fund management companies may also have driven the price up.

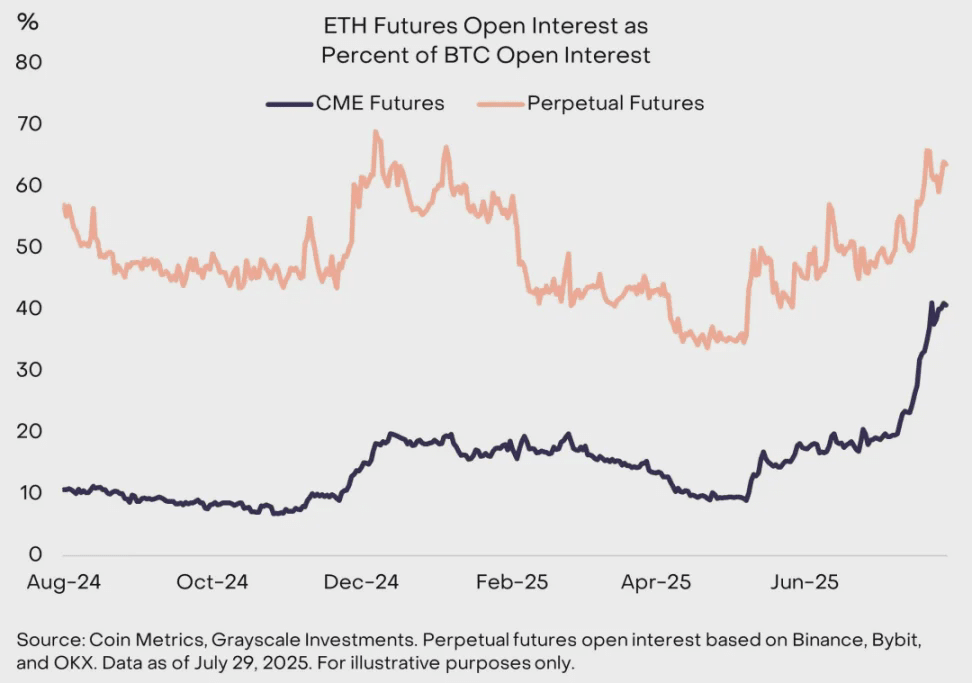

Additionally, Ethereum has gained market share in the cryptocurrency derivatives market this month, indicating rising speculative interest in the asset. In traditional futures listed on the Chicago Mercantile Exchange (CME), the open interest (OI) in ETH futures has increased to about 40% of Bitcoin (BTC) futures open interest (Chart X). In perpetual futures contracts, the number of open contracts for ETH has increased to about 65% of the number of open contracts for Bitcoin (BTC). This month, trading volume for Ethereum perpetual futures also exceeded that of Bitcoin perpetual futures.

Despite ETH being in the spotlight for most of July, Bitcoin investment products also continued to see steady demand from investors. The net inflow for spot Bitcoin ETPs listed in the U.S. reached $6 billion, currently estimated to hold 1.3 million Bitcoin. Several listed companies have also expanded their Bitcoin fund management strategies. Market leader Strategy (formerly MicroStrategy) issued $2.5 billion in new preferred stock to purchase more Bitcoin.

Despite ETH being in the spotlight for most of July, Bitcoin investment products also continued to see steady demand from investors. The net inflow for spot Bitcoin ETPs listed in the U.S. reached $6 billion, currently estimated to hold 1.3 million Bitcoin. Several listed companies have also expanded their Bitcoin fund management strategies. Market leader Strategy (formerly MicroStrategy) issued $2.5 billion in new preferred stock to purchase more Bitcoin.

Additionally, Bitcoin early pioneer and Blockstream CEO Adam Back announced the establishment of a new Bitcoin fund management strategy company - Bitcoin Standard Fund Management ($BSTR). The company will use Bitcoin from Back and other early adopters as capital and will raise equity. The BSTR transaction is very similar to a previous SPAC (Special Purpose Acquisition Company) transaction organized by Cantor Fitzgerald for Twenty One Capital - another large Bitcoin fund management strategy company supported by Tether and SoftBank.

The crypto asset boom

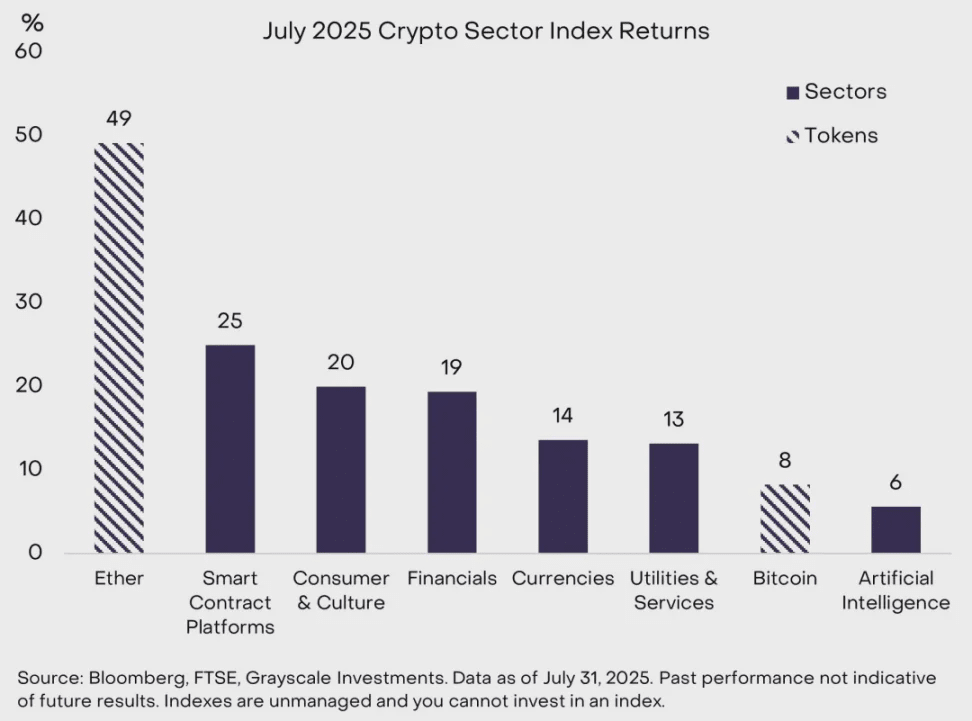

In July, valuations across various sectors of the crypto market rose. From the perspective of the crypto asset sector, the best-performing sector was the smart contract sector (benefiting from ETH's 49% increase), while the worst-performing sector was artificial intelligence, dragged down by the specific weakness of a few tokens (see Chart 6). During July, the open interest and financing rates (cost of financing leveraged long positions) for many crypto assets increased, indicating a heightened risk appetite and an increase in speculative long positions.

After experiencing strong returns, valuations may undergo some degree of pullback or consolidation. The passing of the (GENIUS Act) is a significant boon for the crypto asset class, driving absolute and risk-adjusted returns. Congress is also considering legislation on crypto market structure, with the House's (CLARITY Act) having received bipartisan support on July 17. However, the Senate is reviewing its own version of market structure legislation, and no significant progress is expected before September. Therefore, there may be fewer legislative catalysts to support the rise in crypto asset valuations in the short term.

After experiencing strong returns, valuations may undergo some degree of pullback or consolidation. The passing of the (GENIUS Act) is a significant boon for the crypto asset class, driving absolute and risk-adjusted returns. Congress is also considering legislation on crypto market structure, with the House's (CLARITY Act) having received bipartisan support on July 17. However, the Senate is reviewing its own version of market structure legislation, and no significant progress is expected before September. Therefore, there may be fewer legislative catalysts to support the rise in crypto asset valuations in the short term.

Summary

Nevertheless, we remain very optimistic about the outlook for crypto assets in the coming months. Firstly, even without legislation, regulatory tailwinds still exist. For example, the White House recently released a detailed report on digital assets, proposing 94 specific recommendations to support the development of the U.S. digital asset industry. Of these, 60 fall under the jurisdiction of regulatory agencies (the remaining 34 require action from Congress or joint action with regulators). With the support of regulatory agencies, crypto investment products (such as staking features or broader spot crypto ETPs) may attract new capital into this asset class.

Secondly, we expect the macro environment to continue to favor crypto assets. These assets provide investors with the opportunity to engage with blockchain innovation, while being somewhat immune to certain risks of traditional assets (such as the prolonged weakness of the dollar). In addition to the crypto-related legislation passed in July, President Trump also signed the (One Big Beautiful Bill Act), locking in a large federal budget deficit for the next decade.

He also made it clear that he hopes the Federal Reserve will lower interest rates, emphasizing that a weaker dollar would benefit U.S. manufacturing and increase tariffs on various products and trading partners. Large budget deficits and lower real interest rates may continue to suppress the dollar's value, especially when he receives implicit support from the White House. Scarce digital commodities like Bitcoin and ETH may benefit from this and serve as partial hedging tools in portfolios facing the ongoing risk of a weak dollar.