From JLP to Neutral

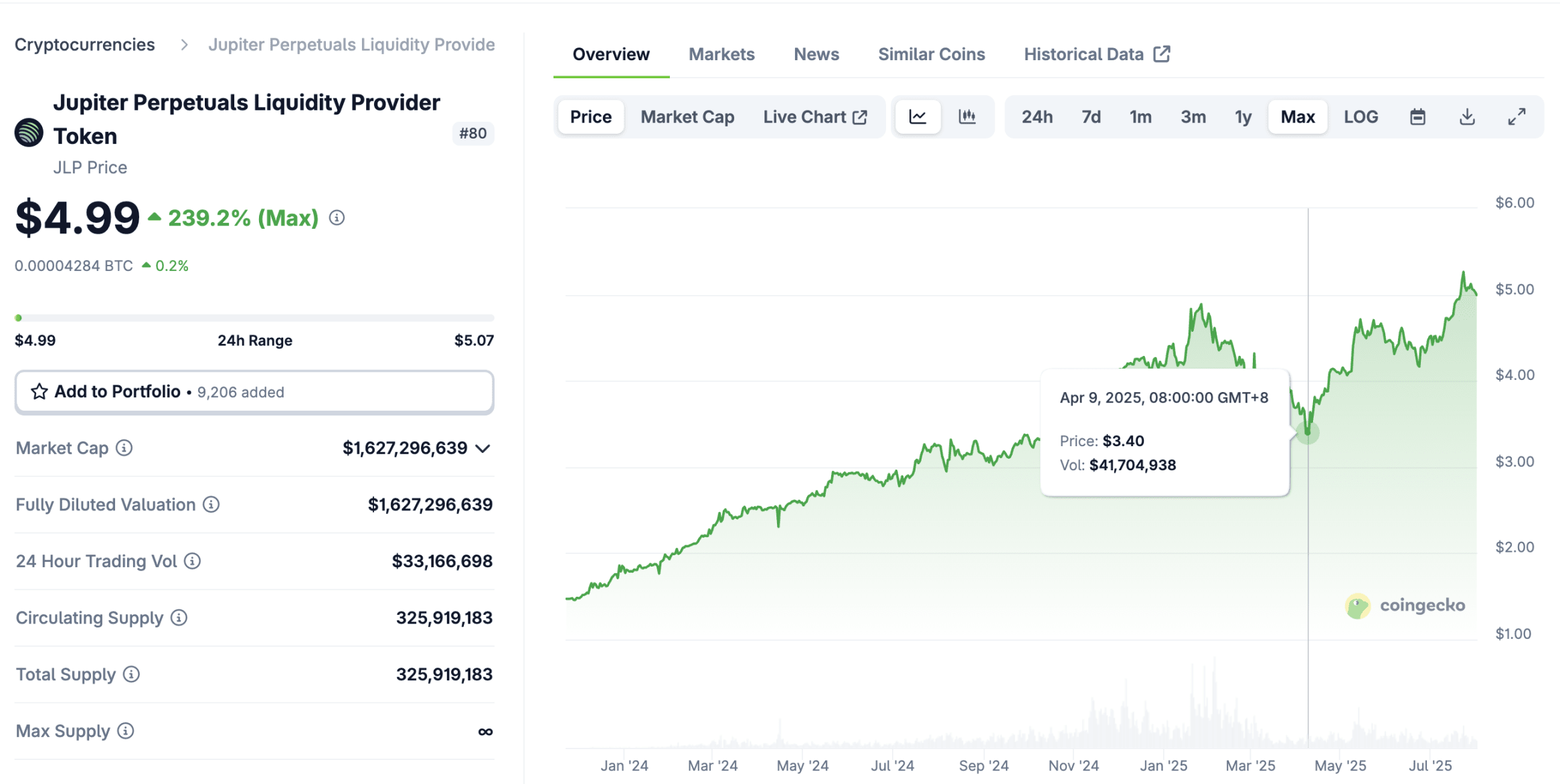

To make money, the first step is often to find quality assets. Not to exaggerate, even looking across the entire crypto world, JLP is among the top quality assets. It has risen 3 times in one year, with a maximum drawdown of 30% in the subsequent three months. While performing excellently, its capital volume exceeds 1 billion USD, which is immense; how did it achieve this?

Price trend of JLP, data: coingecko

JLP stands for Jupiter Perpetual Liquidity Provider Token, which is the liquidity provider token for Jupiter perpetual contracts. Holding JLP is equivalent to depositing money into Jupiter and acting as the counterparty for contract traders. When contract traders profit, JLP will incur losses, and vice versa. After repeated verification of countless similar products over an extended time frame, contract traders are always at a loss; this is the first source of income for JLP.

Furthermore, 75% of the trading fees from Jupiter perpetual contracts will return to JLP, and the generous fee income keeps JLP's annualized income consistently above 30%, and sometimes even exceeds 50%.

JLP itself consists of 47% SOL, 8% ETH, 13% BTC, and 32% USDC, maintaining exposure to crypto asset risks. Therefore, in the strong SOL year of 2024, combined with the previous two types of yields, JLP surged over 3 times. And in the three months where SOL dropped from 295 USD to below 100 USD, due to the limited risk exposure of JLP and the buffering from the previous two types of yields, the decline was 30%. After SOL's price rebounded, JLP had already set a new high.

From this perspective, the scenario of JLP losses is that contract traders make short-term profits in extreme market conditions (but statistics indicate they will eventually lose it back...), and the long-term price weakness of crypto assets. It seems that the long-term risk is only the latter. As long as we hedge this part of the risk, we can obtain a high-yield strategy based on quality assets.

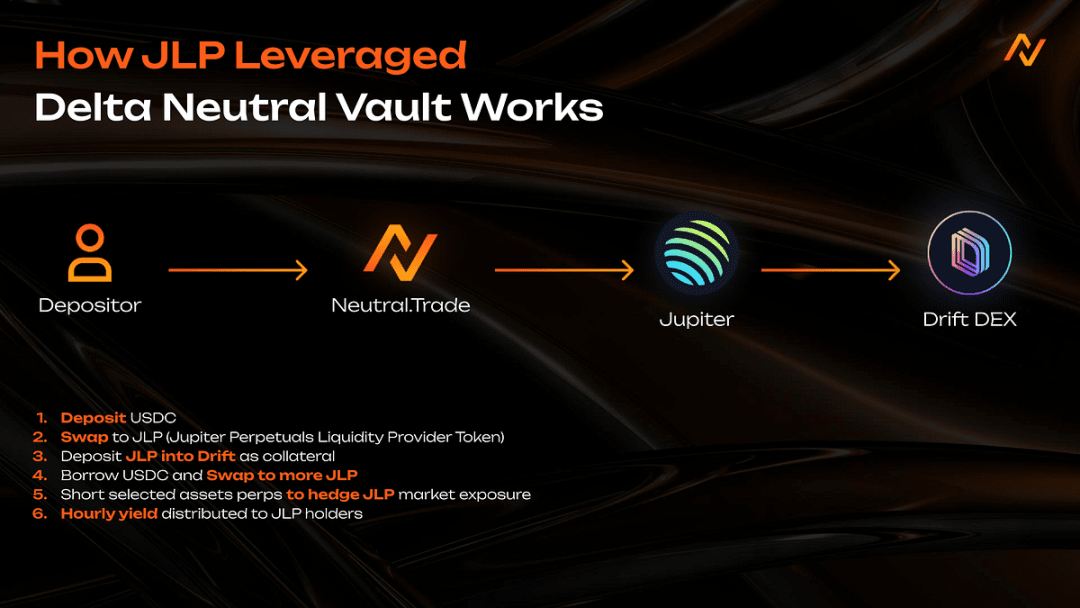

Neutral is an institutional-grade on-chain strategy hedge fund on Solana, providing such a strategy solution:

Users deposit USDC, convert USDC to JLP. They then collateralize JLP in a lending protocol, borrow USDC, and convert it back to JLP. (Profit occurs when the annual yield of JLP exceeds the borrowing interest), and finally use perpetual contracts (Drift) to short the corresponding crypto asset shares (SOL, ETH, BTC) held by JLP to achieve a risk-neutral strategy (theoretically will not incur losses due to price fluctuations).

The Neutral treasury for this strategy currently has a TVL (Total Value Locked) exceeding 12 million USD, with an annualized return exceeding 15%, and the maximum drawdown is generally controlled within 2%.

Retail investor risks vs. institutional advantages

So why don’t I execute this strategy myself and instead leave it to products like Neutral? If I do it myself, I won't be charged any fees (Neutral charges a performance fee of 10% to 25% for various strategies, deducted from the profits).

The reason is simple: retail investors often cannot manage the risk of complex strategy returns well.

In the process of executing the above strategy, short selling hedges have the risk of liquidation, abnormal funding rate risk, and the borrowing leverage part has the risk of losses caused by long-term interest rate inversion. Even if one stays awake and monitors the market, there may not be sufficient funds to add margin or unwind the borrowing cycle in sudden situations.

Institutional-level hedge funds are monitored by teams 24/7 and have rich experience and contingency plans for various systemic risks, indeed outpacing retail investors in risk management by an order of magnitude. The premise of earning is the safety of the principal; it requires careful consideration of personal circumstances whether to believe in the Degen model for maximum returns or to sacrifice some profit for more assured risk management.

Project Overview

Back to the Neutral project itself. It is not the only on-chain hedge fund on the market; it is chosen for introduction because it is collaborating with the Solana Chinese community for promotion, which has relatively reliable endorsements. Secondly, it also has an ongoing points system, with expectations for token issuance, allowing for project airdrop layouts while earning strategy yields (its points calculation rule is: 1 point is generated for every 1 USD asset per year, equivalent to depositing 365 USD for 1 point daily).

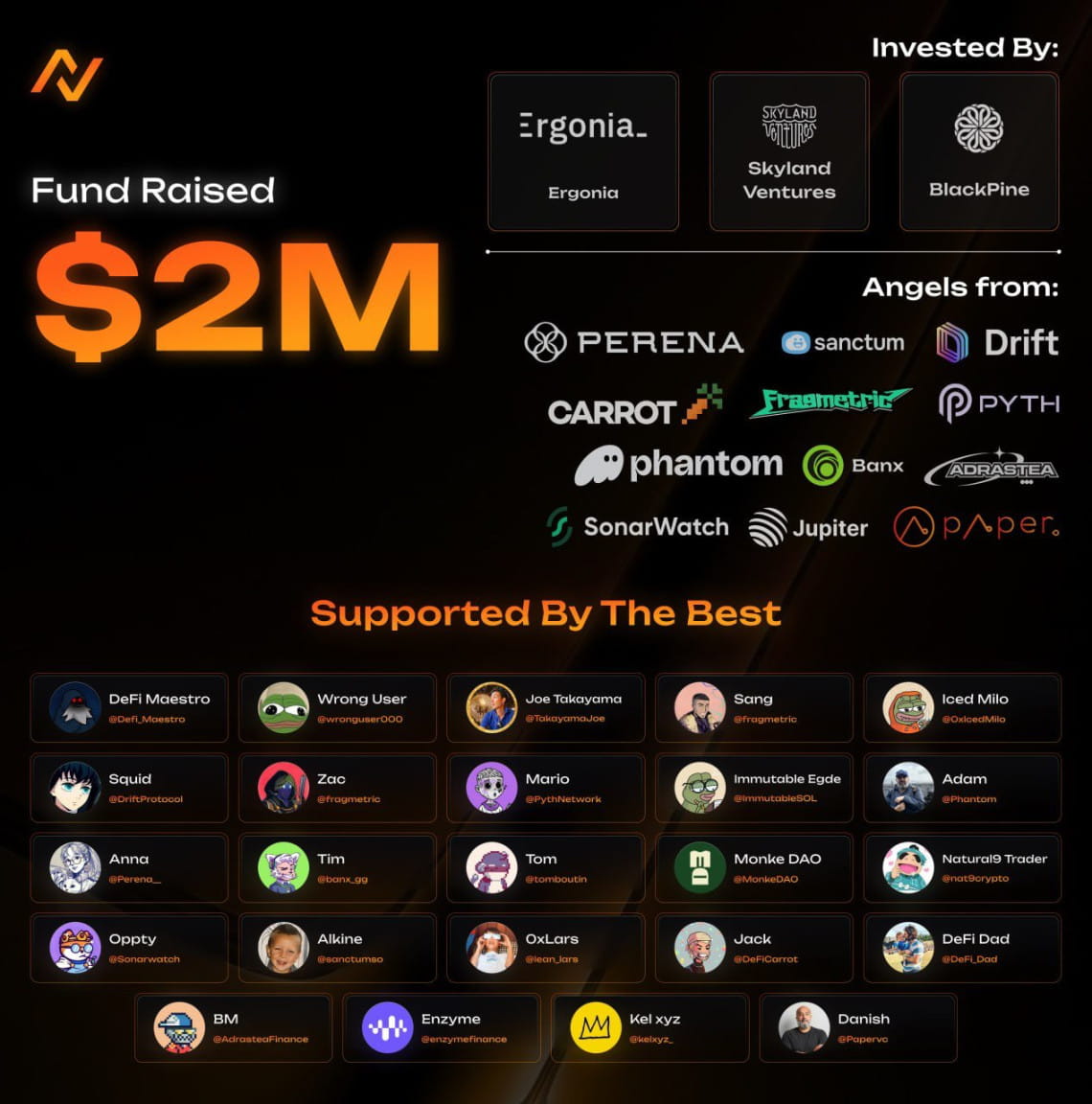

Neutral was initially a winning project at the Solana Radar hackathon and has now grown to a TVL of nearly 36 million USD, generating nearly 2.5 million USD in profits for users, becoming a nascent protocol of considerable scale. Founders Rick and Jared are senior quantitative traders from Goldman Sachs and one of the top three hedge funds globally. On June 1, Neutral announced that it secured 2 million USD in funding from Cumberland and several Solana ecosystem projects and participants.

In addition to the main JLP neutral strategy, Neutral also has multiple yield strategies, including Hyperliquid fee arbitrage. It should be noted that not all strategies are neutral risk; strategies labeled as Directional may experience significant fluctuations with market conditions, which interested readers can research on their own.