On July 30, the highly anticipated Robinhood released its Q2 2025 financial report, sparking widespread market attention and discussion.

Behind this financial report is a key glimpse into how Robinhood is reshaping the broker role in the global embrace of the Web3 trend. As a platform transitioning from traditional finance to the forefront of Web3, its growth drivers and strategic layout are worth exploring.

Financial report data analysis

According to official reports (source: Robinhood Q2 2025 Earnings Report), Robinhood's total revenue in the second quarter was $989 million, a 45% year-over-year increase, with net income reaching $386 million and a profit margin of 39%, significantly improved compared to the same period last year. These data strongly reflect its steady progress in the market, showcasing its potential to gradually establish a foothold in the highly competitive brokerage business.

In terms of revenue composition, trading income (including options trading, stock trading, cryptocurrency trading, etc.) was $539 million, a 65% year-over-year increase, which was mainly due to the synchronized increase in cryptocurrency and stock trading volumes. Its proactive Web3 transformation strategy, especially the push for cryptocurrency business, is an important new engine for the growth of trading income.

Interest income reached $302 million, benefiting from the expansion of cash management products, while subscription services (mainly Robinhood Gold) contributed $114 million, a 76% year-over-year increase, with the number of users rising to 3.5 million. This demonstrates Robinhood's success in building high-stickiness revenue sources.

Compared to the second quarter of 2024 (total revenue $682 million, net income $188 million), Robinhood's revenue structure has shown a more pronounced trend of diversification, significantly reducing the risks associated with relying on a single revenue source.

Behind these data, Robinhood demonstrates its balance in user growth and cost management. The significant increase in net income indicates that the company has seized market opportunities while controlling operating expenses, especially under changing interest rate environments and user behaviors, with the growth of interest and subscription income providing strong support for the increase in profit margins.

However, the diversification of the revenue structure also brings new considerations: the rapid growth of trading income, while exciting, still faces the risk of regulatory fluctuations due to its reliance on PFOF (Payment for Order Flow); the expansion of subscription services must continue to enhance user experience to maintain growth momentum. These figures not only reflect current performance but also provide clear guidance for the company's future strategic adjustments, laying an important foundation for the subsequent Web3 transformation.

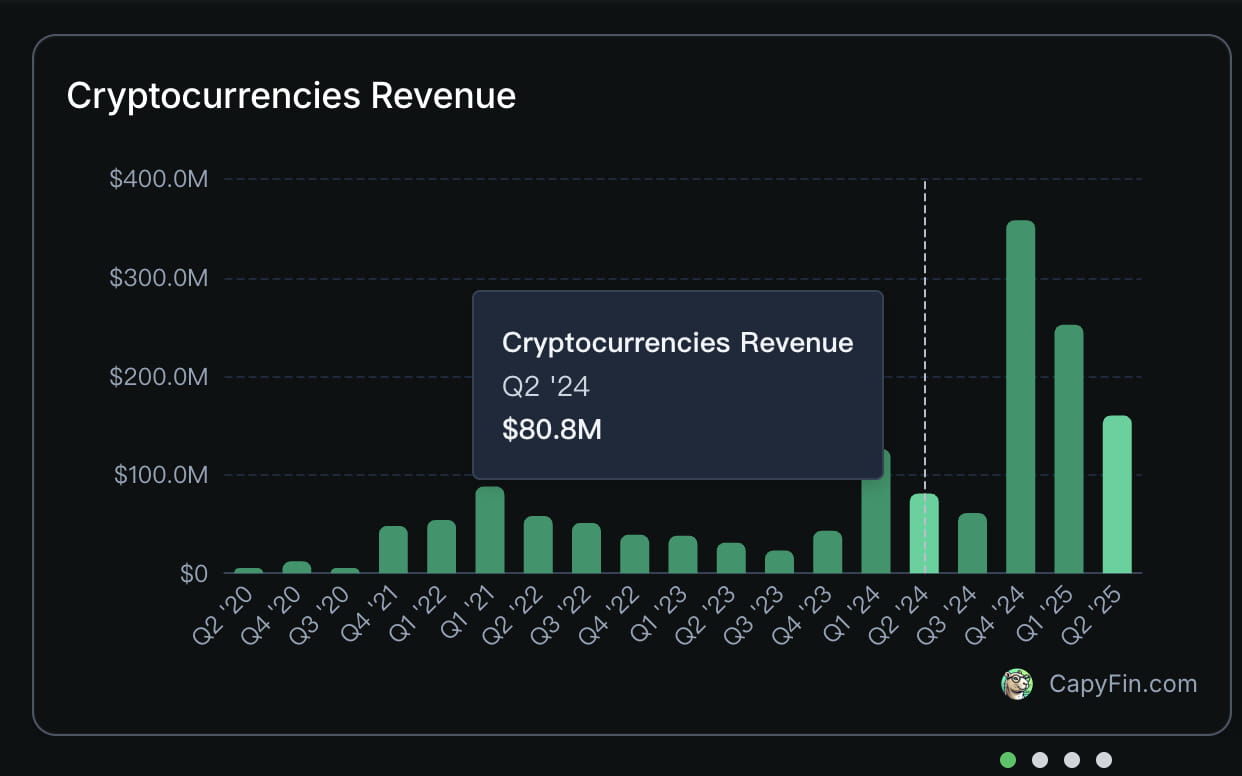

Cryptocurrency business revenue grew by 98%

In the past second quarter, Robinhood's most important innovation was its attempts in the crypto field. According to the financial report, Q2 cryptocurrency trading revenue was $160 million, marking a staggering 98% increase compared to $80.8 million in the same period last year.

Achieving such outstanding growth in the cryptocurrency sector is inseparable from Robinhood's two major moves related to the crypto field this year—acquiring Bitstamp and launching U.S. stock tokenization trading services.

On June 2, 2025, Robinhood announced the official completion of its $200 million acquisition of the global cryptocurrency exchange Bitstamp, one of the longest-operating exchanges worldwide. This acquisition not only brought Robinhood a mature crypto exchange network covering Europe, the UK, and Asia, but also over 50 global regulatory licenses. More importantly, Bitstamp's institutional client base filled the gap of Robinhood's long-standing reputation as a 'retail paradise,' solidifying its position in both retail and institutional markets, and equipping it to compete with world-renowned cryptocurrency exchanges like Binance and Coinbase.

The acquisition of Bitstamp provides significant support for Robinhood's expansion into the crypto sector, and stock prices are the most intuitive reflection of market sentiment: after announcing the completion of the Bitstamp acquisition, Robinhood's stock price surged 13% to $74.42 in pre-market trading on June 4.

The strategic significance of this acquisition may be more important than the data growth; acquiring Bitstamp marks Robinhood's transformation from a retail-oriented trading platform to a global retail + institutional fintech company, and it also enhances Robinhood's competitiveness in the cryptocurrency field.

In addition to the strategic acquisition of Bitstamp, Robinhood has also made significant innovations in technology—launching stock tokenization trading services aimed at the European market.

On June 30, 2025, Robinhood officially announced the launch of U.S. stock tokenization products at the 'Robinhood Presents: To Catch a Token' event held in Cannes, France, and will go live in the EU region on July 1.

Currently, Robinhood supports tokenized trading of over 200 popular U.S. stocks and ETFs, including not only popular companies like Apple and Nvidia but also private popular companies like OpenAi and SpaceX that are not publicly listed. Although the founders of both companies have publicly questioned this, there is no doubt that Robinhood has achieved its goal—attracting the attention of investors interested in U.S. stock trading worldwide.

Competitors

Robinhood's impressive performance in Q2 has also led to discussions in the market comparing Robinhood with traditional broker Futu.

As a traditional brokerage, Futu is forced to face this increasingly powerful 'young competitor,' and some users on platform X have also shared their comparative analysis of the two brokers.

User @bruce_aiweb3's tweet provides a detailed comparison of the two from various aspects. From the product background, Robinhood was created by Stanford high-frequency trading software developers rather than Wall Street, which gives Robinhood a technology-first style from birth, with a smooth user experience and 'gamified' guidance, making it very popular among young retail investors.

In contrast, Futu has the unique 'Tencent' background, inheriting the large company's precise vision and product control capabilities: killer products and highly sticky communication communities. While this background brings many mature experiences and methodologies, it also comes with geopolitical risks.

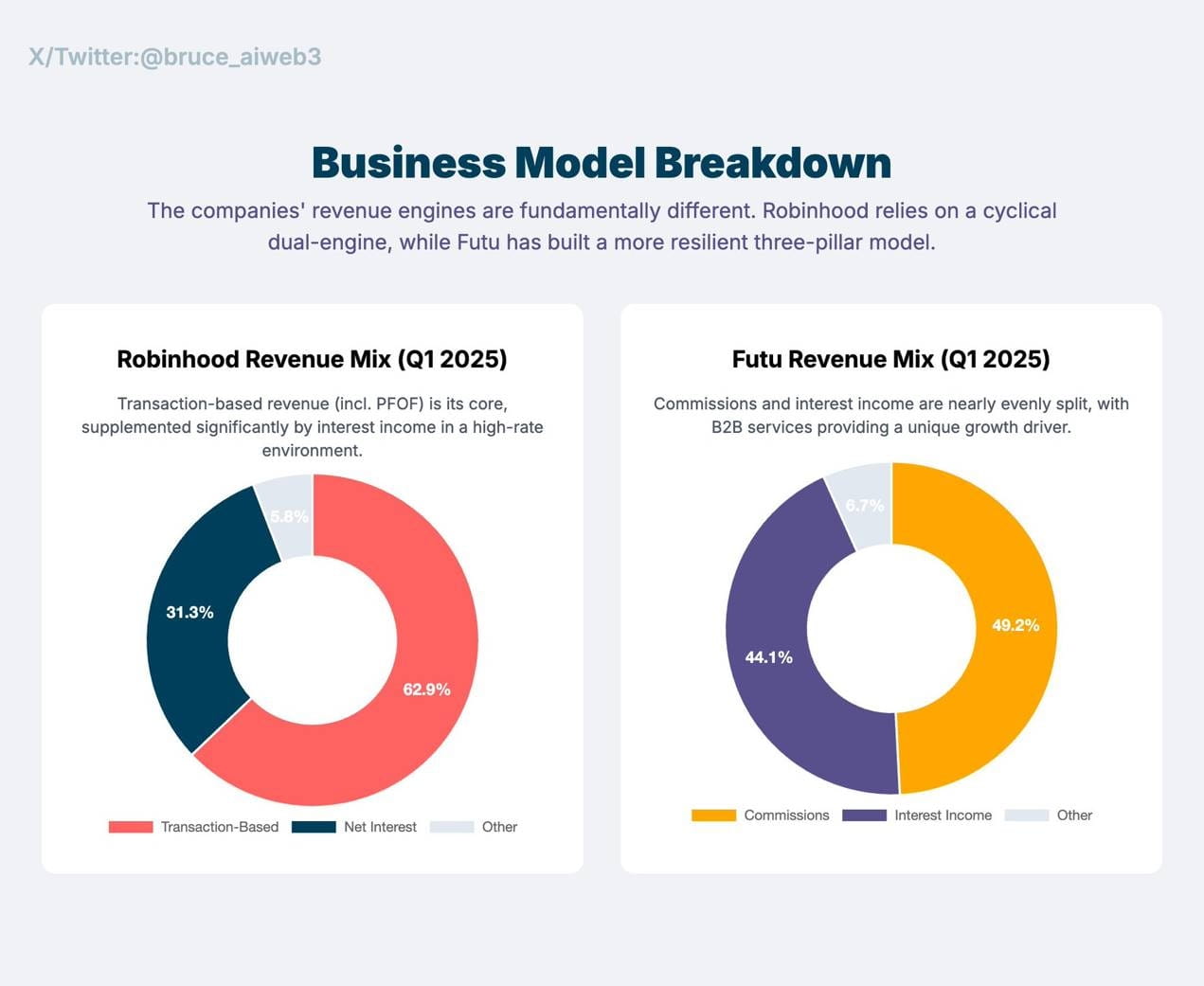

From the perspective of revenue sources, Robinhood's current revenue mainly relies on PFOF (Payment for Order Flow) and interest income, which, although cyclical, brings in very high revenue during the cycle. In contrast, Futu's revenue sources are more diversified; in addition to commissions and interest, Futu also earns high profits from B2B enterprise services (IPO distribution, IR, ESOP management), which also enhances Futu's resilience against market fluctuations.

Image source @Bruce_aiweb3

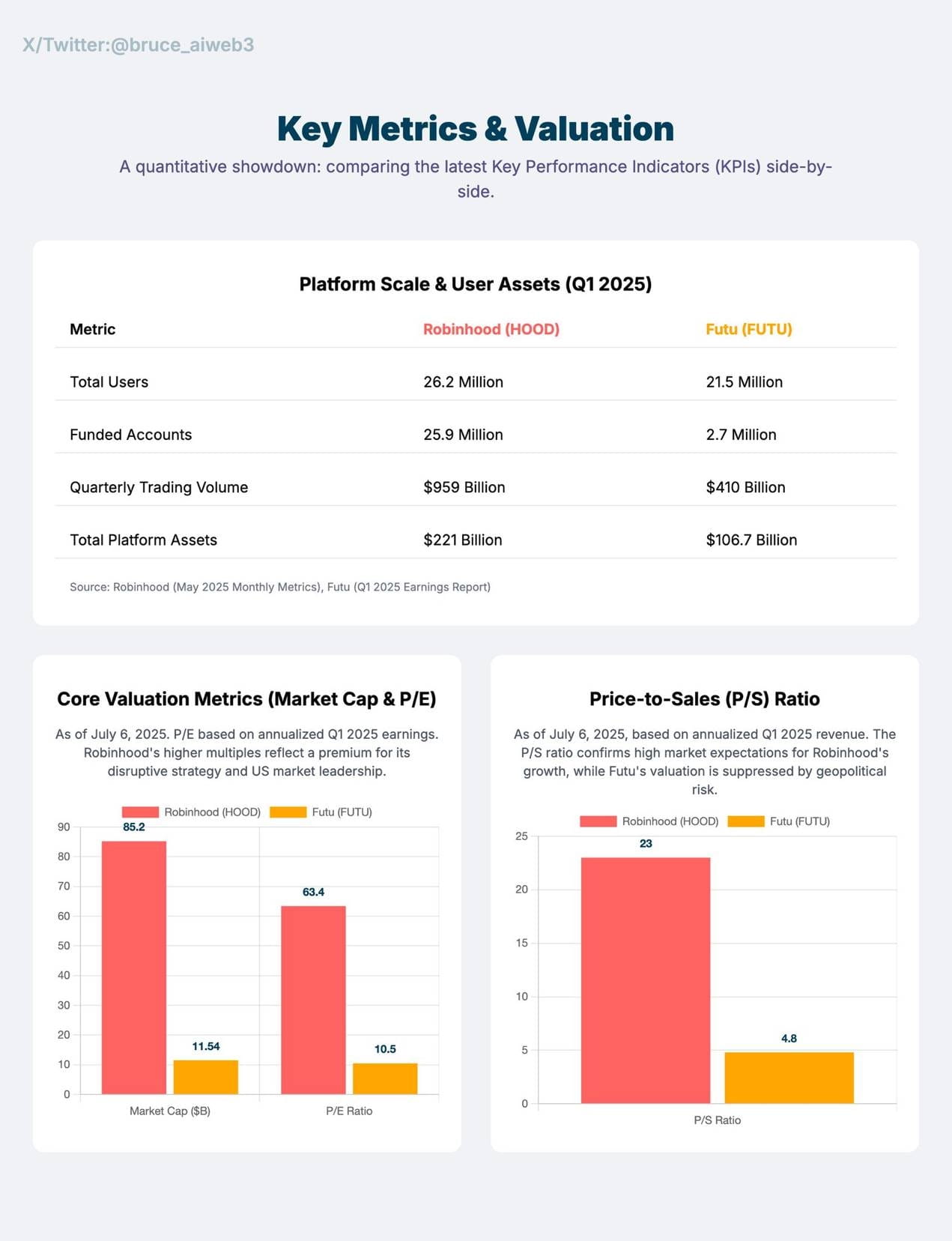

From a data comparison perspective, Robinhood's price-to-earnings ratio is approximately 63 times, far exceeding Futu's 10.5 times. At the same time, Robinhood has a larger user base, with 25.9 million accounts, about ten times that of Futu, although Futu's average user asset is higher.

Image source @Bruce_aiweb3

Since Futu has not yet released its Q2 financial report, this article compares their Q1 financial reports. Robinhood's scale is larger ($927 million vs. $603 million), but its profit margin is lower (36.2% vs. 45.6%). This reflects that although Robinhood is rapidly developing with broader global coverage, it lacks the robust profitability that Futu has built over the long term.

The report comparing the fiscal year 2024 to the fiscal year 2023 also reflects this point: Robinhood's revenue grew by 58.6%, achieving a net profit of $1.41 billion, turning the trend of losses into profits. Futu, on the other hand, saw steady growth: revenue increased by 36.7%, net income grew by 28.3%, reaching $699 million.

In future development, Robinhood is addressing the major threats of regulatory constraints while embracing the global wave of Web3, gradually stepping towards becoming a global brokerage giant. However, the geopolitical risks that Futu has long faced persist and may not have good solutions in the short term.

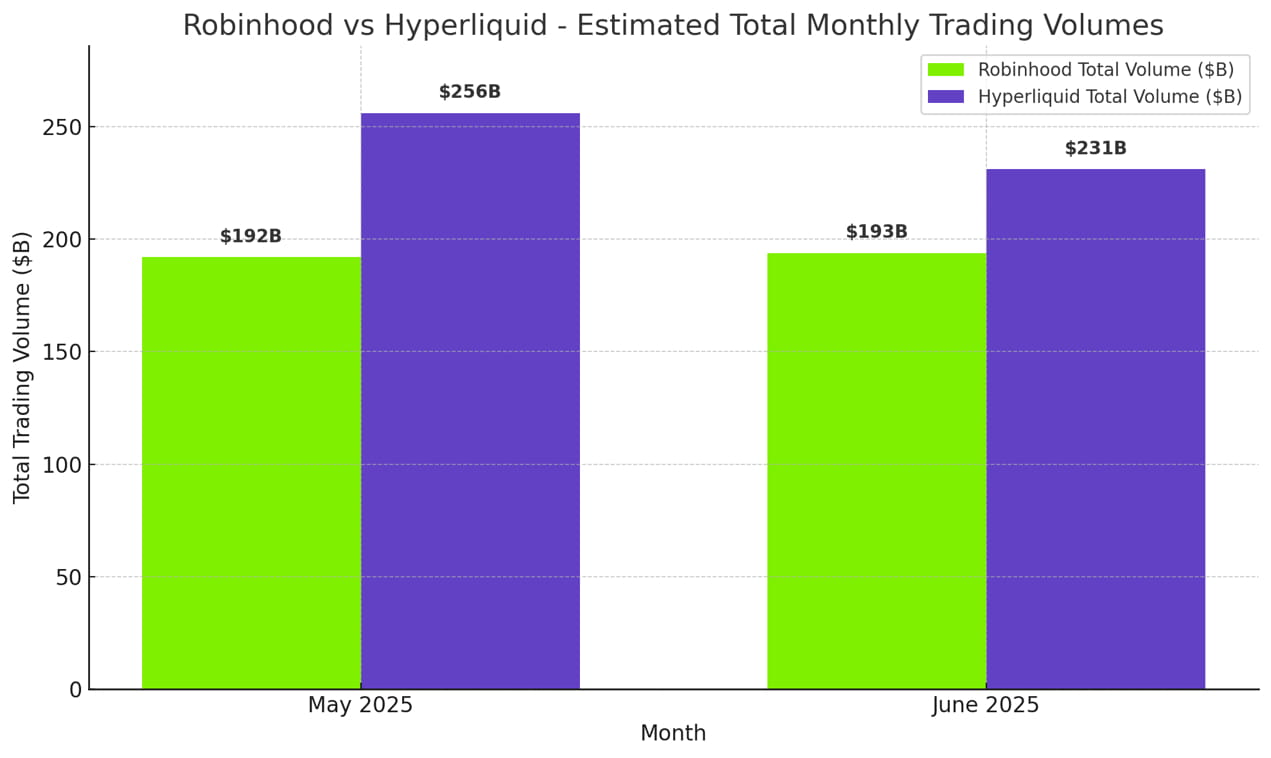

As a fellow 'light of retail investors' and a rising star in the Web3 field, Robinhood has also been compared to the emerging decentralized exchange Hyperliquid over the past two years.

In the data comparison of the past May and June, Hyperliquid's trading data exceeded that of Robinhood.

Image source @jonbma

At the same time, some users have pointed out that Hyperliquid's data source from perpetual contracts has led to a multiple increase in trading volume, which is not a fair comparison.

In addition, there are still many users who believe that Hyperliquid is severely undervalued. This also indirectly reflects how large the demand for cryptocurrency trading is and validates Robinhood’s strategic choice to transition to Web3. Furthermore, Robinhood has a more diversified business model and a broader global market, which gives it a much deeper moat compared to Hyperliquid.

Whether it is Futu or Hyperliquid, Robinhood has its own competitive barriers compared to them, currently positioned in a multidimensional competitive landscape of stable profits, explosive growth, and technological innovation in the Web3 era. Robinhood has solidified its market position with its robust performance in Q2.

Starting the second half

Robinhood's second-quarter financial report provided the market with a clear answer: it is an incredibly correct decision for traditional brokers to embrace crypto.

Currently, in this wave of increasing global acceptance of Web3, Robinhood has undoubtedly become a leader in this wave, and in the second half of this year, Robinhood will launch multiple crypto-related plans, such as acquiring Canadian digital asset service provider WonderFi, launching cryptocurrency perpetual futures trading in Europe, and introducing more cryptocurrency product portfolios for customers.

We look forward to this 'Robin Hood' that has emerged in retail support continuing to drive the integration of crypto and traditional finance, delivering an even better performance in the second half of this year.