Hello everyone, I am Azu. In discussing BTCFi today, everyone seems to be circling around the same question: What does BTC's yield really depend on to sustain in the long term? Just relying on narratives is not enough, and short-term incentives are also insufficient. What can truly make the 'BTC yield curve' resemble a financial product, rather than just an event page, is connecting on-chain yields with real-world interest rate benchmarks — and RWA (especially tokenized US Treasuries/cash management assets) just happens to provide a sufficiently clear and interpretable anchor point. The rapid expansion of tokenized US Treasuries in recent years shows what the market is looking for: CoinGecko's RWA report mentions that the market value of tokenized US Treasuries is expected to reach about $5.6 billion in April 2025, and has seen significant growth since the beginning of 2024, with a large share also taken by BlackRock's BUIDL. Concurrent news reports have also described it as a 'hedge and yield substitute during crypto pullbacks,' with funds flowing into tokenized US Treasuries that resemble 'short-duration interest rate instruments' during volatility.

So does Lorenzo have a chance to bring this 'real world interest rate' in? I think there is a chance, but it won't be as simple as 'just stuffing a US Treasury bond token into the protocol'. The truly feasible path is actually the 'structured capability' that Lorenzo is already laying out—Financial Abstraction Layer (FAL) and On-Chain Traded Fund (OTF). The official documentation describes the execution logic of FAL very straightforwardly: funds are raised on-chain, strategies can be executed off-chain, and then settled and distributed back on-chain; while OTF, as an 'on-chain fund structure', can carry various strategy combinations, even including 'Tokenized CeFi lending or RWA income' in the supported strategy types. This means that the RWA Lorenzo imagines is not turning you into a retail investor buying US Treasury bond tokens across chains, but more like 'packaging real-world interest rates and cash flows into on-chain holdable, liquidatable, and combinable yield modules', and then piecing them together with the stBTC/YAT BTCFi note system.

The first product form I imagine would be a dual-engine OTF of 'BTC base + RWA yield side': the base uses stBTC to provide a more 'BTC native' yield logic, while the upper layer uses tokenized US Treasury bonds/money market instruments to provide a more stable short-duration interest rate, merging the two cash flows into an on-chain fund share that can be subscribed and redeemed, and tracked NAV. You can understand it as 'BTCFi version of yield barcode': on the left is the on-chain security and staking yield of BTC, on the right is the real-world interest rate curve, both sides are not for stimulation, but to make the yields more interpretable and more like asset allocation. The second form would be more 'exchange/institution friendly', and I think it is the easiest to land: using FAL's 'off-chain execution, on-chain settlement' to access regulated RWA channels, avoiding retail investors handling compliance and redemption details themselves, allowing users to obtain standardized yield tokens or share certificates on-chain, rather than holding a bunch of RWA tokens that require whitelisting and working hours for redemption. This idea aligns with the direction mentioned in OKX's RWA article regarding 'compliance framework, liquidity, and infrastructure synergy': clear regulation and available channels will determine whether RWA can transform from concept to scalable products.

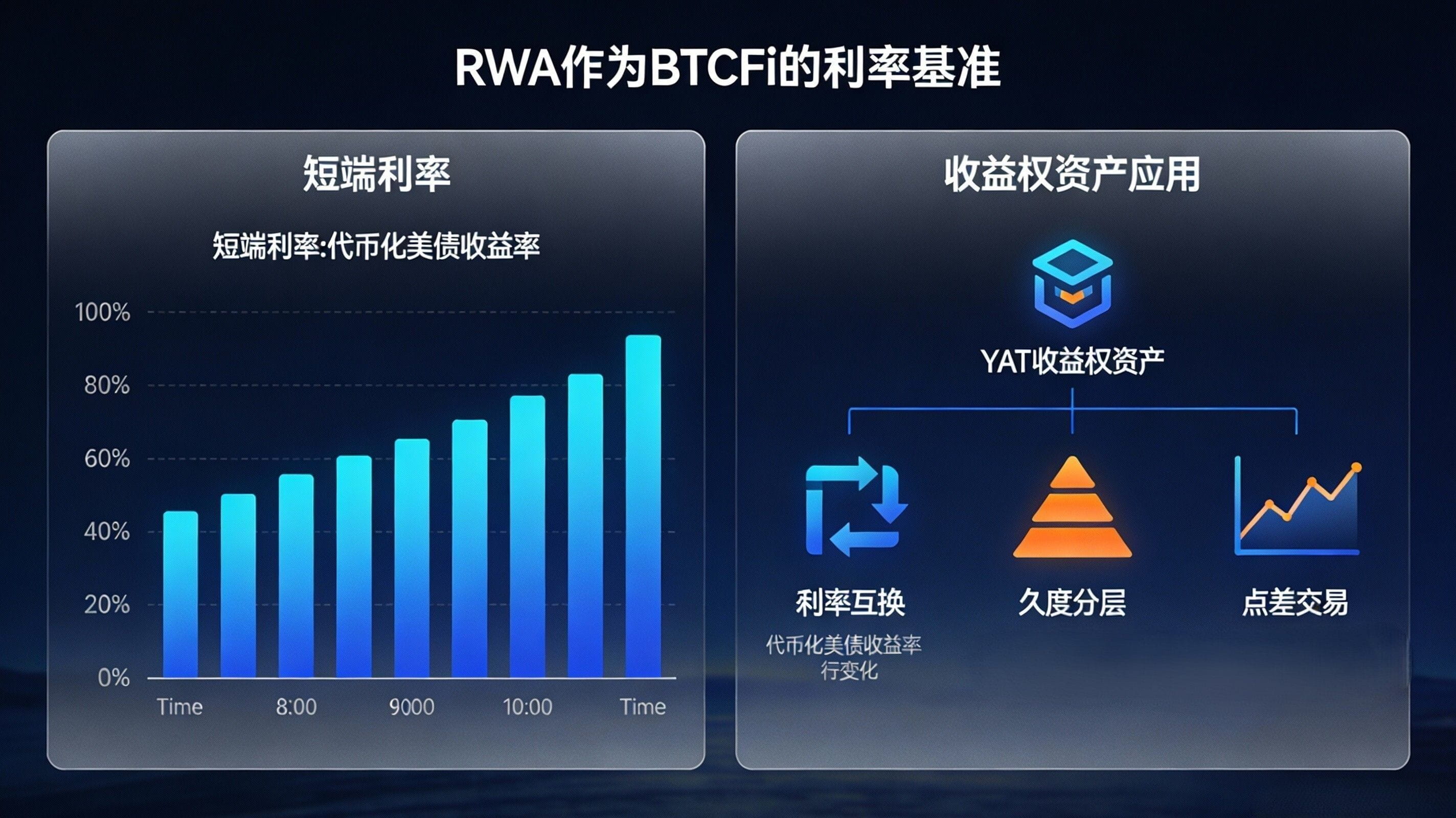

The third form is more like 'turning RWA into the interest rate benchmark for BTCFi': when there is a sufficiently credible 'short-end interest rate' on-chain (like the yield of tokenized US Treasury bonds), yield-bearing assets like YAT will no longer rely solely on emotional pricing, but can be used for interest rate swaps, duration layering, and even for spread trading between 'BTC yield curve vs US Treasury curve'—this will upgrade BTCFi from 'earning yield' to 'engaging in interest rate markets'. Of course, the hardest part of this step is not financial engineering, but 'verifiability'. The good news is that Lorenzo is indeed catching up on safety and verifiability: the Chainlink ecosystem shows that Lorenzo has integrated Data Feeds, CCIP, and Proof of Reserve, and the official description of Proof of Reserve serves the purpose of '1:1 backing and automated risk control for tokenized assets', and even allows reserve checks to be directly integrated into mint/redemption logic. If these tools are combined with the compliant issuance of RWA, it may make 'real world interest rates' enter the on-chain financial stack in a more credible way.

But I want to splash cold water thoroughly: the biggest threshold for BTC × RWA has never been 'whether technology can do it', but 'whether you are willing to accept stronger compliance and slower friction'. OKX's article on the Hong Kong LEAP framework emphasizes keywords like legal clarity, liquidity improvement, and tax incentives, and cites extremely optimistic market size predictions; these signals indicate that regulators and financial centers are actively embracing RWA, but it also means that products are likely to move toward whitelist, tiered access, and stricter disclosure. For users, the changes in rules will be very obvious: in the past, playing DeFi was 'click in and click out', in the future, BTC × RWA is more likely to be 'you can buy a more stable interest rate, but you have to accept clearer identity, asset source, and risk control terms'. The impact on users is also very real: yield fluctuations may be smoother, but you will face new risk combinations—such as redemption rhythm, counterparty channels, off-chain execution transparency, and the 'combination pressure' when stBTC discounts and RWA liquidity contract simultaneously in extreme market conditions.

I give you a segment of Azu's action guide that you can use directly: if you want to ambush BTC × RWA in advance, don't first ask 'is there a product', first ask three things—first, whether the scale and use cases of tokenized US Treasury bonds and similar RWA continue to grow to the extent of 'being the on-chain benchmark interest rate'; second, whether Lorenzo's FAL/OTF has continuously written RWA income into executable strategy modules and made settlement, disclosure, and risk control standard interfaces; third, whether verifiable components like Proof of Reserve are truly used to constrain mint/redemption and risk control triggers, rather than just as marketing labels. Focus on these three things, then decide whether to participate and how much position to take; during the transition from 'concept to product', the safest approach is always to trial run with small amounts, first confirming exit paths and costs, and then discussing amplifying returns.