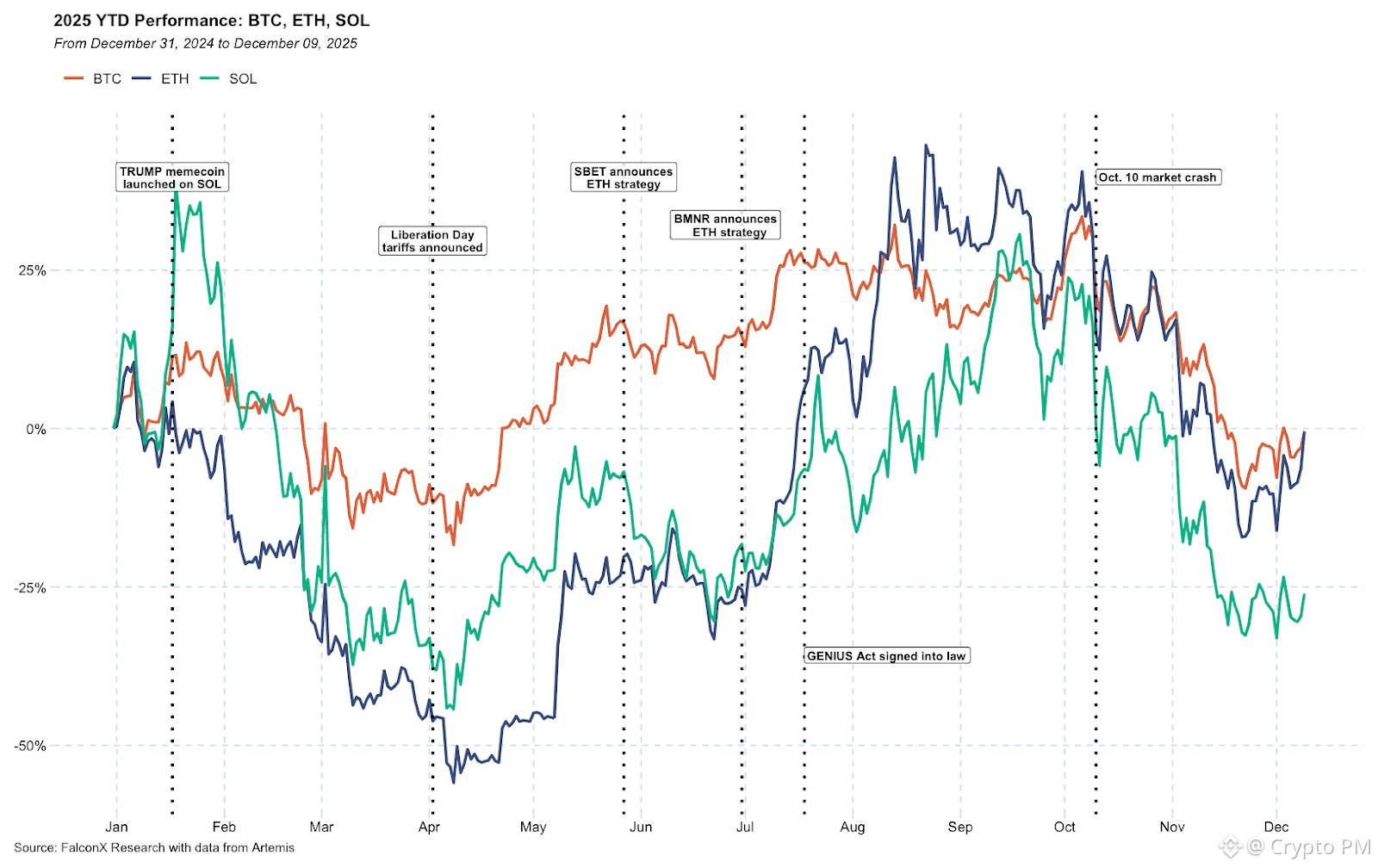

2025 delivered another period of substantial change in the crypto market, including several shifts that unfolded differently from the early-year consensus. While the majors held up fairly well, altcoins largely bled throughout the year, as macro shocks and activity in other markets, such as AI-related equities and gold, distracted from a slew of otherwise positive developments.

Meanwhile, we saw all-time highs in crypto-related equities and idiosyncratic runs in a handful of names such as HYPE and ZEC. DATs became commonplace for the majors, while more spot ETFs launched in the US market.

On the regulatory front, the Trump Administration and Republican controlled Congress provided a more accommodative stance, driving key changes to federal crypto regulations and guidance aimed at creating a clear framework to foster innovation. This included the passage of the GENIUS Act, which establishes a comprehensive US regulatory framework for stablecoins.

Crypto performance this year demonstrated the 4-year cycle may no longer hold and could be more tied to macro, forcing investors to be judicious with regards to token selection. Looking ahead to 2026, we may see a continuation of this. Crypto stands to tap into its largest addressable audience yet but will likely see the most success in fintech-like solutions, trading, and payments. Moreover, ever evolving market structure, thanks to new products and regulatory changes, could open different investor bases and impact the venues driving price action.

Market Structure

Inflows for Major Crypto Spot ETFs Were Strong in 2025

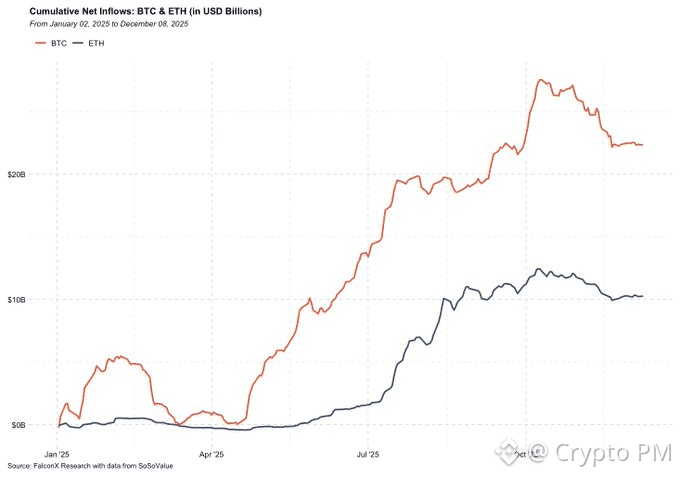

BTC and ETH spot ETFs saw significant investor demand, with BTC seeing over $22B of spot ETF inflows and ETH seeing $10B, as of Dec 8, according to data from SoSo Value. What’s impressive is most of these flows came in late Q2 and Q3, rebounding from a weak Q1.

Looking into next year, we may see a near-term moderation in flows in the majors in part due to compression in basis. However, major investment platforms such as Vanguard opening up access to these vehicles present a previously untapped avenue for new inflows.

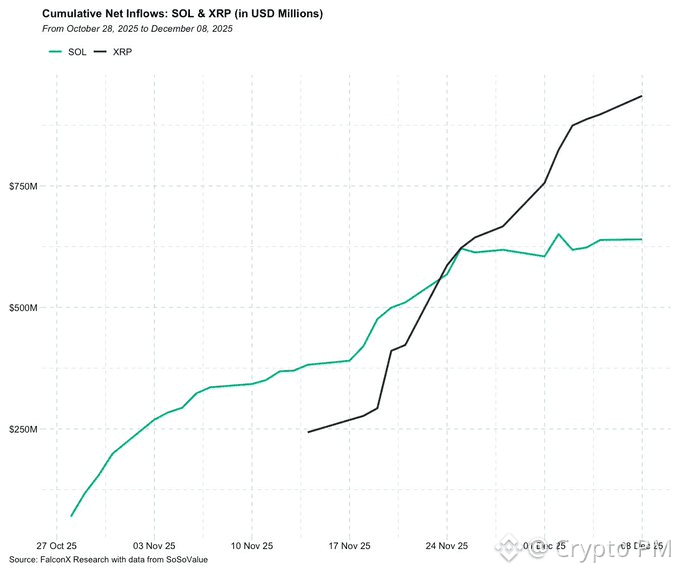

While spot ETFs for BTC and ETH have seen some outflows in Q4, newer ETF launches such as SOL & XRP have seen persistent inflows, suggesting pent-up demand for other leading tokens despite the recent broad-based price declines. With the SEC implementing generic listing standards for crypto ETFs in September, there is likely to be a wave of new product launches throughout 2026, with filings for spot ADA, DOT, SUI, and ZEC ETFs currently under review.

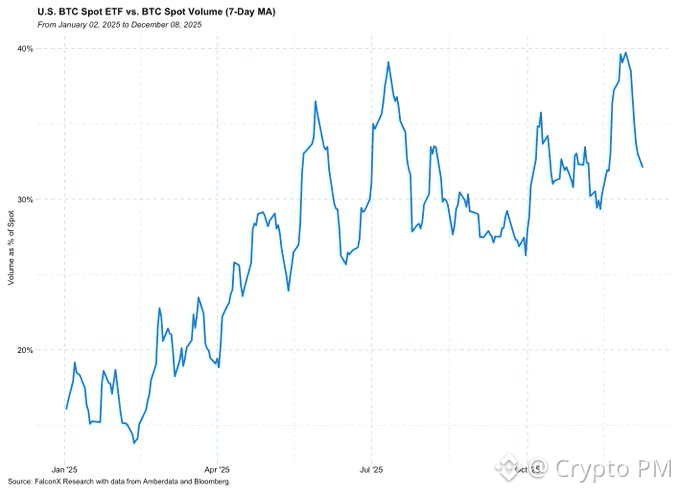

What may be underappreciated is how these vehicles are changing market structure. Spot ETFs captured a growing share of overall BTC volumes, especially as spot volumes softened going into year end. This could impact where and how price discovery happens over time.

Multi-Asset ETPs and Active ETPs are Coming to Market

We are in the very early innings of crypto index products coming to market and expect to see growth in this area in 2026. Grayscale and 21Shares1 are amongst issuers leading the way with these products in the U.S., with the Grayscale CoinDesk Crypto 5 (GDLC) index product converting to an ETF in September 2025 and 21Shares launching two crypto index ETFs in November 2025 (TTOP and TXBC).

Many indices are market cap oriented and may predominantly focus on large caps given the gap in liquidity between majors and the rest of the top 50-100 crypto assets. Consequently, this could result in a paradigm where the big stay big thanks to passive inflows and could favor legacy tokens.

Total AUM in these kinds of products remain relatively small, for now, however, with leading crypto index products still around $1B AUM or less, which compares to AUM of $118B for BTC spot ETFs and $20B for ETH spot ETFs as of Dec 8.

Given growing acceptance of crypto from wealth advisors, with portfolio allocations of up to 4% commonly cited from firms such as Morgan Stanley and Bank of America, index products stand to be attractive ways for passive investors to gain broader exposure to the crypto market. And while the single-asset BTC and ETH ETFs may be starting points for many investors given their size and significance, index ETFs are amongst the next logical steps and would mirror the evolution of ETF investments in mature asset classes such as equities. Such products could create new trading opportunities, such as index arb.

We could see active strategies within crypto ETPs as well, with investment giant T Rowe filing for an active crypto ETF that would seek to outperform the FTSE Crypto US Listed Index. Meanwhile, structured product crypto ETFs, such as income generation through covered calls, could also proliferate given growing activity in crypto options markets and could lead to dampened volatility over time.

Allocators

There is increasingly a growing shift of institutional investors picking up exposure to crypto. Recent 13Fs revealed the Harvard Endowment and SWFs including the Abu Dhabi Investment Council increased their holdings of Bitcoin ETFs in Q3. The state of Texas purchased $5M of BTC ETFs, while the Czech Central Bank also made some crypto purchases. These are clear signs BTC is increasingly being seen as playing an important role in portfolio allocation for institutions. As more institutions get off 0 allocations, BTC and crypto stand to see meaningful inflows.

BlackRock’s Larry Fink himself stated SWFs are buying BTC into the weakness in Q4, further supporting the notion that long-term oriented institutional investors are entering BTC as it matures and as access grows.

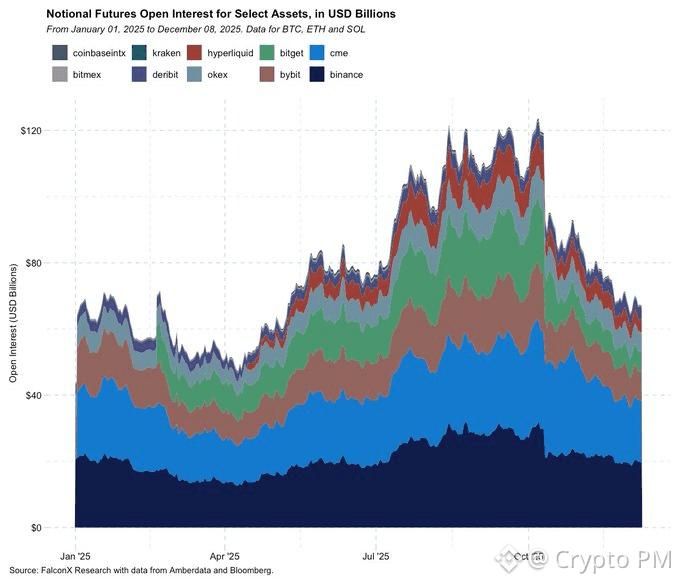

Futures: OI across select majors peaked at $120B before the 10/10 crash

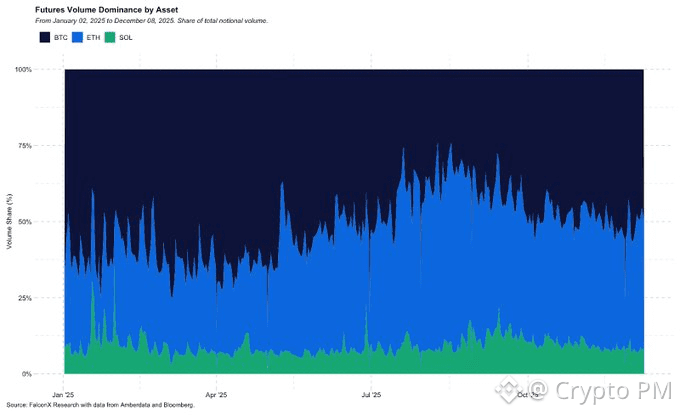

Futures volumes across BTC, ETH, and SOL grinded up throughout the year in aggregate, hitting a YTD high in October prior to the 10/10 crash. Growth was driven by an increase in ETH trading activity, which peaked as a share of majors futures volume in the late summer. Despite strong interest earlier in the year around heightened on-chain activity, SOL futures volumes failed to meaningfully dent BTC and ETH volumes by year end.

CME and Binance further solidified their hold as the top venues by open interest. ETH CME OI exploded 10X from the spring to the start of Q4, signaling increased institutional interest. CME launched SOL futures in March, and their markets have since grown to roughly $1B of OI. Similarly, CME XRP futures had around $800M of OI as of early December, per data from Velo.

Futures for BTC, ETH and SOL recorded over $400B in aggregate volumes around October 10th, highlighting the significance of the market crash. Notably, volumes have trailed down from them, underscoring the lasting impact of this event.

TradFi continues to expand its footprint in crypto derivatives. CME cemented itself as a top venue in terms of BTC open interest. Cboe launched cash-settled options on a spot Bitcoin ETF index and announced plans to roll out continuous futures (effectively perps) for BTC and ETH in December.

The landscape could change meaningfully with US regulators allowing spot crypto trading on registered futures exchanges, with derivatives exchange Bitnomial launching leveraged retail spot crypto trading in December. Moreover, on December 8, the CFTC announced a pilot program of using tokenized collateral in cleared derivatives markets, starting with BTC, ETH, and USDC, which could shift volumes from leading crypto futures venues. It is also possible perp DEXes enter the US market under innovation exemptions from the CFTC and SEC which could add to competition.

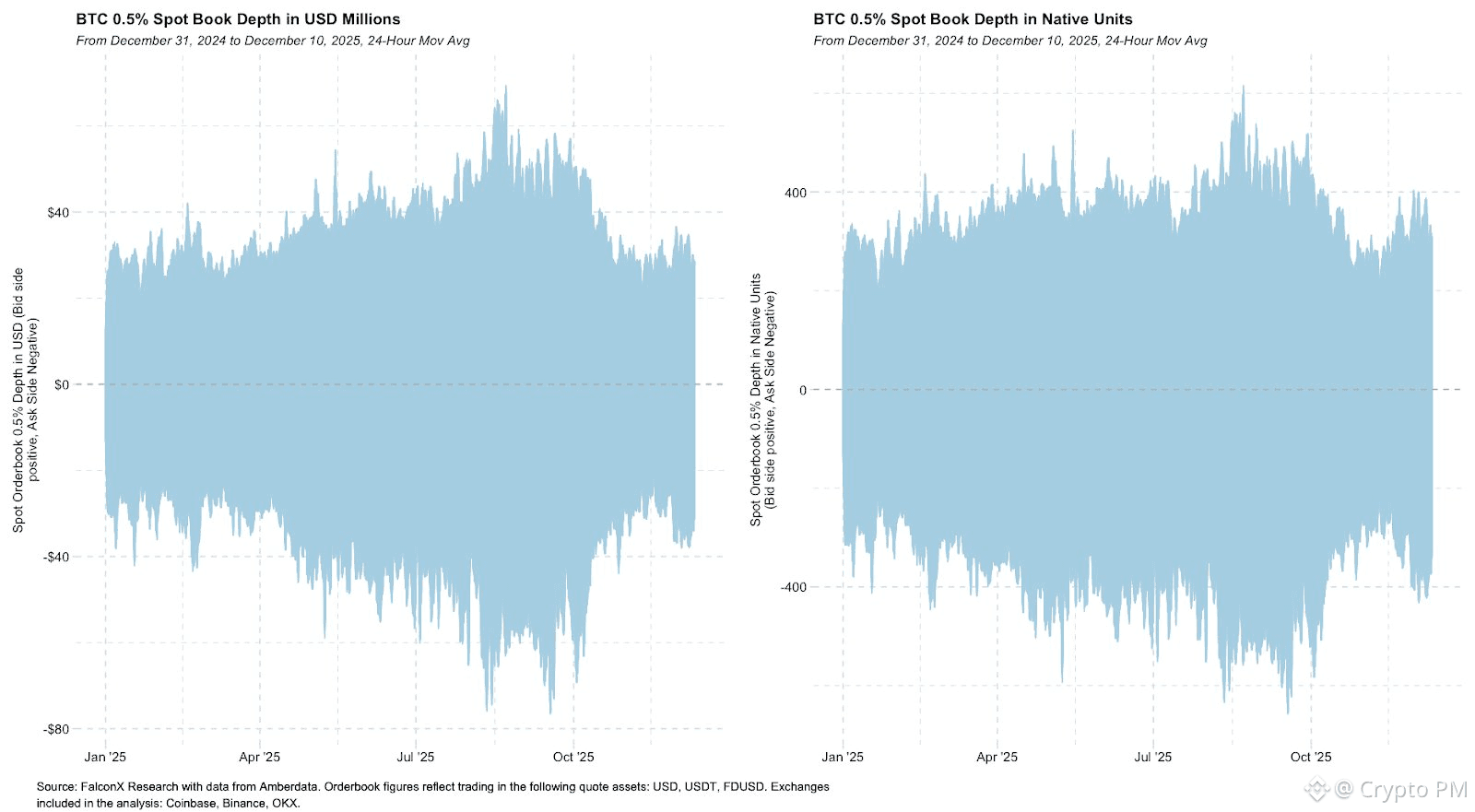

Orderbooks

BTC orderbooks reveal a substantial compression in depth since October, helping drive increased volatility in Q4. Until we see the market and liquidity providers recover from the aftermath of October 10th, it is likely we continue to see sharp BTC moves due to lower liquidity. The positive news is that orderbook depth has started to improve since November.

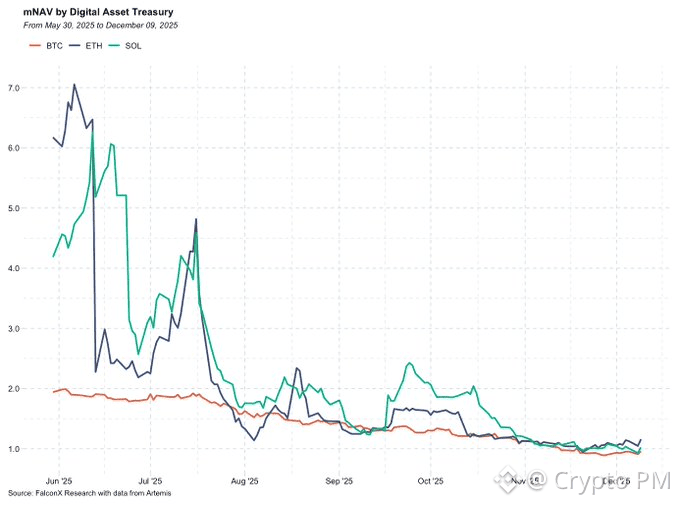

Digital Asset Treasury Companies (DATs)

The DAT trade seems to be losing steam, with 14 out of 20 DATs tracked by Artemis trading below 1x mNAV as of December 9. However, ETH DATs still seem to be going strong, with BMNR trading above 1.20x mNAV and steadily buying ETH.

Given the broad weakness in DATs, we see it likely that the markets consolidate around 1-2 leaders in each asset, considering they still offer investors value through their ability to generate yield, their significant trading volume, and most importantly enabling access to crypto to investors who cannot access spot crypto or crypto ETFs. We anticipate DATs will need to step up their hunt for yield as compressing mNAVs push investors to demand more from these vehicles and as spot ETFs with staking enabled become competitive alternatives to DATs.

MSCI is currently evaluating whether to exclude DATs from its indices. Its consultation period will conclude December 31, and it will release a verdict by January 15, 2026. We note that DATs do not require indices to operate but may see lack of mechanical inflows as a result which would otherwise help support their mNAV and enable selling shares for crypto purchases. Without these flows, DATs may need to resort to generating yield to remain attractive for non-index investors or to roll such proceeds into supporting their share price directly.

Lending and Structured Products

Perhaps the biggest developments in this area in 2025 were TradFi players beginning to accept crypto. JPMorgan began accepting crypto ETFs such as IBIT as collateral for loans and plans to accept spot BTC and ETH as collateral as well. Moreover, it is seeking to launch a structured note tied to BTC’s performance. Cantor launched a $2B BTC lending business earlier in the year.

As more of TradFi steps into crypto, CeFi lending stands to see considerable growth. And as investors seek out the benefits of spot crypto (24x7 trading), crypto-native lending platforms may see outsized growth.

Crypto-Native Themes: RWA Perps and Prediction Markets Stand to be Key Growth Areas

We expect several themes to dominate next year. ETH’s L2s could see more activity on the potential launch of Base’s token and on major improvements to ZK technology. Perp markets on non-crypto assets, such as equities, stand to be a major catalyst for DEXes, with names like Hyperliquid beginning to support such markets. Privacy also stands to be topical with continued interest in names like ZEC and as new privacy projects go to market. Finally prediction markets will remain front and center of growing crypto verticals, on top of record volumes this year, and as leaders like Polymarket prepare to launch a token.

ETH L2s Could See Revival

Ethereum’s scaling roadmap is in full swing following its successful Fusaka upgrade Dec 3, which most notably brought minimum blob fees, helping align L2 success to ETH with incremental ETH burn.

Base

2026 is shaping up to be a seismic year for ETH’s L2 future. The leading optimistic rollup by TVL and DEX Volumes, per DeFi Llama, Base, is expected to launch a token which would be notable considering the significant revenue generation of the L2 ($62M annualized revenue as of Dec 7, per Artemis) and considering Coinbase is a public company.

While payments and stablecoin chains like Tempo (Stripe) and Arc (Circle) are top of mind for many, Base could be the first live and broadly accessible fintech chain with a token. Coinbase has considerable reach (100M+ verified users and 8M+ monthly transacting users) already and could use token incentives to drive activity to apps built on it.

ZK L2s

ZK L2s such as ZK and STRK could begin to see increased adoption thanks to breakthroughs in reducing proving times and reducing proving costs. Given ZK proofs are computationally expensive, they have historically been costlier and taken longer to produce, limiting practical applications of ZK L2s. Now that they are effectively real-time (~1 second for ZK and real-time for STRK) and can be proved with consumer hardware (phones) this unlocks major use cases for their ZK tech, such as latency sensitive applications (gaming, social) and ZK identity.

Moreover, the fast finality now possible on ZK L2s stands to be a major advancement. Now that transactions can be proved quickly and can see finality in the next L1 batch submission which can take minutes to hours, ZK rollups could become a preferred choice over optimistic rollups which face a 7-day finality window. As these chains see adoption, batches can be submitted more frequently for cheaper due to more transactions reducing the cost.

The Perpification of Everything

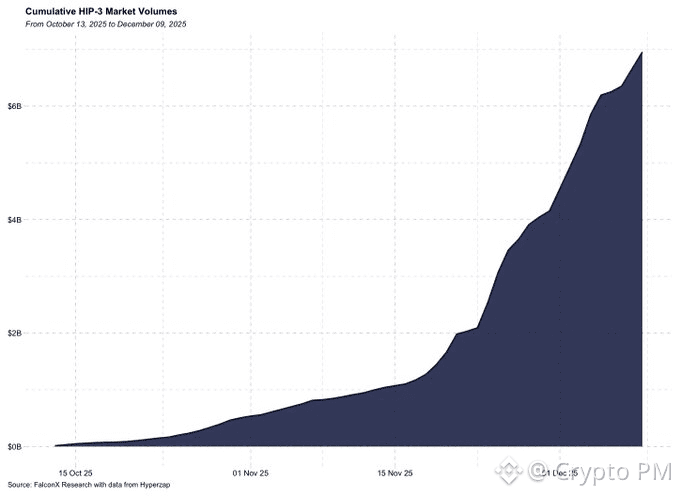

On-chain markets for traditional assets represent a notable area of development for the coming year, with the potential to introduce incremental volume less correlated with broader crypto market cycles. Several perp DEXes are moving towards this vision, including Hyperliquid, Lighter, and Ostium. Hyperliquid has seen the most success here thus far with its HIP-3 markets, which enable permissionless perp deployments, allowing for custom markets. HIP-3 markets regularly do over $100M+ volumes/day and have cleared over $6B in cumulative volume since going live in mid October.

This could be a massive growth area for crypto given the much larger volumes historically for traditional assets, especially equities. Given that there are more crypto-related equities and more platforms, such as Robinhood, are offering both crypto and stock trading, it makes sense for DeFi to mirror such offerings.

At the same time, CLOB perp DEXes are seeing an increasingly crowded field and may compete with prediction markets in the future. Splitting investor capital and attention across too many similar projects could result in a scenario where the aggregate market cap of the sector grows but the market cap of individual names decline.

Privacy To Remain Topical

With Zcash’s strong run and publicity in 2H25, privacy tokens are now front and center. Many investors now see Zcash as complementary to majors such as BTC rather than a competitor, which helps boost its profile. Prominent VCs such as a16z are supporting privacy projects (Aztec, for instance), helping back privacy with real capital and clout. Notably, ZEC has been the one privacy coin that has secured recent CEX listings (OKX relisted it, Bitget listed it) when the trend historically has been delistings for privacy coins.

Moreover, ZEC now has a DAT (NASDAQ: CYPH) seeded by the Winklevoss Twins that held 1.4% of ZEC’s circulating supply as of November 18, which is around $90M at recent levels. A public company holding a privacy coin would have been unlikely a few years ago. There could also be ZEC ETFs in the future, with Grayscale filing in November to convert its ZEC trust into an ETF, though we note this is still pending approval.

Shielded (private) ZEC has grown to ~25% of supply, suggesting more users are accepting such features. This is despite the substantial risk that they could be flagged by KYT services or trading venues that would not want to accept transactions from addresses interacting with shielded pools out of caution.

All this points to renewed interest in privacy features for crypto, but may be limited to projects that have opt-in privacy, such as ZEC, rather than privacy by default tokens (XMR). We note that as of Dec 9, ZEC is close to parity with XMR at a $7B market cap and both show signs of consolidation. Notable projects supporting privacy with selective disclosure include Aztec and Fhenix. Aztec recently ran its token sale and is targeting TGE as early as February 2026, making it one of the projects to watch. And considering the Ethereum Foundation also outlined a push for privacy, ETH-related privacy projects may be especially worth monitoring.

Prediction Markets

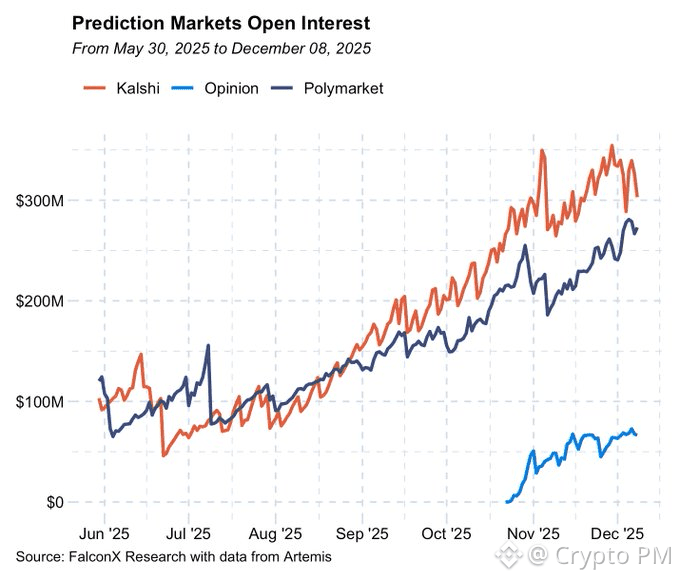

Perhaps the hottest crypto applications in recent months are prediction markets, which have seen impressive funding announcements and record volumes in a period when the broader crypto market generally trended downwards.

Despite the headlines, prediction markets are still minuscule in terms of activity with volume and open interest both totalling around $550M across Kalshi and Polymarket as of Dec 8, according to Artemis.

Market participation may increase as traders adjust to the mechanics of these newer venues. Despite current volumes, the data has found utility in several sectors, with news outlets and politicians themselves leveraging the data as a valuable signal.

Adoption is still in early days, with Polymarket just recently re-entering the US market after getting the green light from the CFTC, and competition between its rival Kalshi could heat up as both seek to expand distribution of their platforms.

Polymarket’s team have publicly stated the platform intends to launch a token – which could help drive further adoption and allow crypto investors to get exposure to this fast growing vertical.

Conclusion

The crypto markets continue to evolve, with maturation of the asset class bringing more institutional involvement. Derivatives open interest is growing, and options OI now sits far above futures for BTC, marking a shift in players and strategies. Moreover, with crypto ETFs now proliferating in the US and allocators suggesting up to 4% allocations to crypto, it is likely that investor interest in crypto will continue to increase over time. With a constructive regulatory outlook ahead (market structure bill, SEC/CFTC innovation exemptions), 2026 stands to bring meaningful growth in the industry.

For crypto projects, 2026 could be a transformative year if accommodative regulations allow Web2 firms and DeFi protocols to offer crypto products more broadly in the US, setting the stage for potential catalysts for many projects. The further entwinement of crypto and TradFi will likely remain a key driver as equities and other RWA come on-chain, via perps, for example, or spot. And with technology improvements over the years, promising solutions like ZK could drive further crypto adoption.