Sober Options Studio × Derive.XYZ Joint Production @DeriveXYZ_CN

Written by Sober Options Studio Analyst Jenna @Jenna_w5

1. The Impact of the U.S. Government Shutdown on the Crypto Market

This week, global financial markets continue to be under pressure from a political event currently unfolding—the U.S. federal government shutdown. This has lasted for 24 days and is predicted by the market (such as Polymarket) to potentially set the record for the longest shutdown in history. Polymarket data shows that traders generally expect this deadlock to extend into mid-November or even longer, meaning the market must shift from 'short-term shock' mode to 'long-term systemic pressure' mode.

The so-called U.S. government shutdown essentially occurs when the U.S. Congress fails to timely approve a new fiscal budget or a temporary spending bill (Continuing Resolution, CR), leading to the suspension of most non-essential services of the federal government. In simple terms, the government is facing a 'shutdown' due to a political stalemate.

The fundamental reason for this stalemate lies in the profound differences between the two parties on fiscal spending and priorities, sending a clear signal to the global market: there are flaws in the political governance capacity of the world's largest economy.

The negative impact of this long-term shutdown is profoundly affecting the cryptocurrency market through multiple pathways.

Firstly, it has brought about ongoing liquidity tightening and risk aversion. Institutional investors, facing an uncertain policy environment, are forced to reduce leverage, which not only tightens market liquidity but also exacerbates the volatility and downward pressure on asset prices.

Secondly, due to the shutdown of key government departments and regulatory agencies, important regulatory approvals and policy advancements have come to a complete standstill. This may include the long-term suspension of key favorable policies such as stablecoins, leading to the inability of the market's expected 'catalysts' to materialize, thus creating ongoing 'expectation gap' pressure.

Finally, the persistent information vacuum, namely the interruption of key economic data releases, further exacerbates uncertainty, forcing investors to assign higher pricing to future volatility.

The current 'government shutdown' is a structural macro pressure. It continues to affect the valuation anchoring of risk assets and the central volatility.

II. Analysis of BTC and ETH Volatility Structure: Multi-dimensional Mapping of Uncertainty

The current pricing structure of the BTC and ETH options market clearly reflects the transition of market sentiment from panic to 'cautiously neutral' under the ongoing macro pressure of the 'government shutdown' and the TACO market, as well as the systemic pricing of long-term uncertainty.

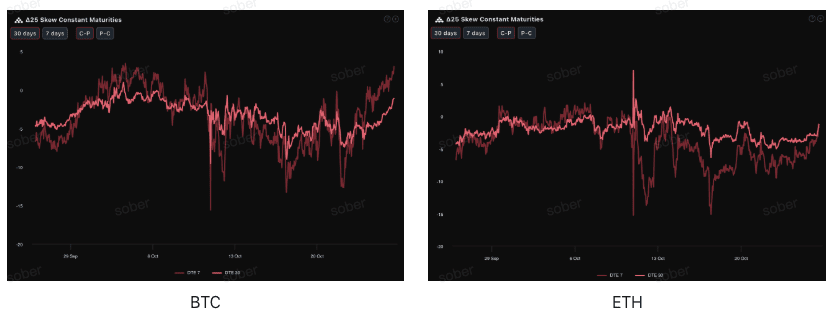

Skew: Significant retreat in bearish sentiment, with BTC confidence higher than ETH.

By observing Delta 25 Skew (implied volatility of call options - implied volatility of put options), the recent indicators for BTC and ETH have shown a significant corrective rebound from the significantly negative range of last week, indicating a decrease in the panic hedging demand for downside (bearish) tail risks, and the pricing of options has shifted from 'extremely pessimistic' to 'cautiously neutral'.

From different assets, the DTE 7 days (7 days until expiration) negative Skew value of ETH is still deeper than that of BTC, and the DTE 7 days negative Skew value of ETH is also lower than its DTE 30 days. This indicates that market confidence in ETH is relatively weaker than BTC, with investors having a stronger awareness of extreme short-term declines and panic emotions.

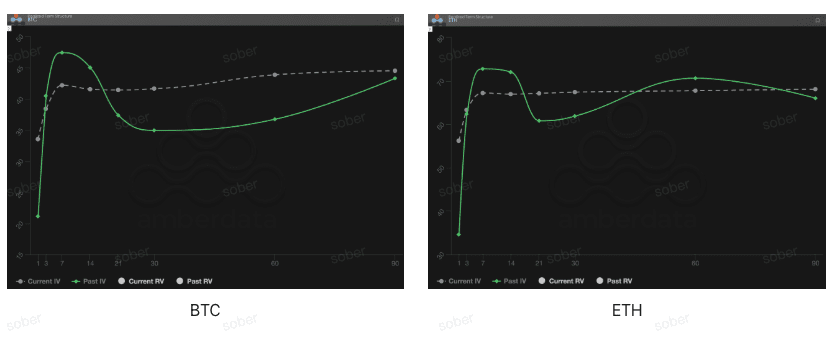

Term Structure: Near-term IV retreated, while long-term volatility remains robust.

Term structure data also confirms the easing of short-term sentiment and the continued pricing of long-term risks.

Short-term IV retreat: Whether for BTC or ETH, the current Current IV (implied volatility) curve at the near end (DTE 7-30 days) is lower compared to the historical Past IV (historical implied volatility) during the same period. This corroborates the repair of Skew, suggesting that the immediate impact of short-term macro risks seems to have been partially digested, and the premium for short-term event risk is decreasing.

Long-term IV remains strong: Long-term (DTE 60/90 days) IV remains at a high level, and the market's pricing of mid-term (2-3 months) systemic uncertainty (such as the prolonged government shutdown and the Federal Reserve's interest rate cut process) has not relaxed.

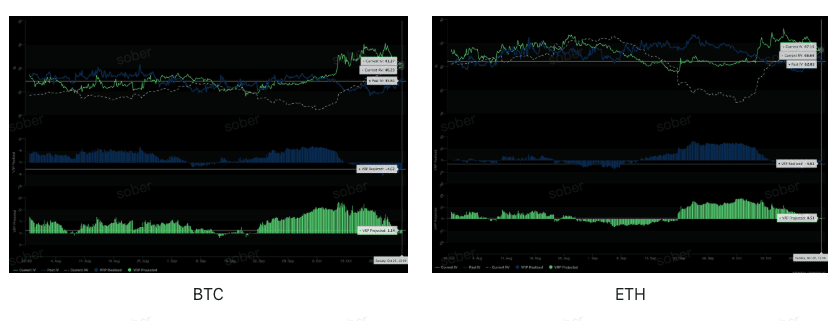

Volatility Risk Premium (VRP): Strategy Alert under Contradictory Signals

VRP (Volatility Risk Premium = Implied Volatility IV - Realized Volatility RV) is an important indicator for assessing whether options pricing is reasonable. In an environment where VRP Realized is continuously deeply negative, blindly believing in the positive values of VRP Projected and shorting volatility (Short Volatility) is extremely dangerous. The market has just experienced the lesson of 'underestimating extreme volatility.' Investors should adopt structured strategies to balance the potential short volatility gains with high tail risks.

VRP Projected is positive: Although the realized VRP is negative, the current expected VRP is positive (BTC +1.14, ETH +0.51). This statistically suggests that the current implied volatility (IV) is generally considered overvalued by the market.

VRP Realized remains deeply negative: Both BTC and ETH show significant negative values (-4.62 and -4.61). This indicates that the market's actual volatility (RV) over the past 30 days has far exceeded the pricing of options contracts (IV). This is a strong warning signal that the market remains in a highly sensitive state, experiencing intense and rapid fluctuations that are not fully captured by option pricing.

III. Options Strategy Recommendations: Structured Deployments to Capture Excess Returns

Given that the current macro risks have shifted to persistent long-term systemic pressures, and options data shows Skew repair, short-term IV retreat, but VRP Realized continues to be deeply negative, we recommend the following two strategies to cope with long-term uncertainty.

Strategy: Bull Call Spread

With short-term IV retreating and the market showing potential upward recovery momentum, locking in limited upward gains at low cost and high win rates is suitable for investors expecting a moderate rebound in prices.

Strategy construction (using BTC as an example): It is recommended to choose contracts with DTE of 30-45 days until expiration.

Buy one at-the-money or slightly out-of-the-money (ATM/Slightly OTM) call option (Long Call).

Sell one deep out-of-the-money (Deep OTM) call option (Short Call).

Core Advantage: The maximum loss of this strategy is limited to net premium expenditure, with risks fully locked. The premium income obtained from selling out-of-the-money call options can significantly reduce the cost of building positions, suitable for those who do not expect a significant price surge but wish to capture moderate corrective rises.

Strategy: Long Strangle

In response to the high volatility revealed by the deeply negative VRP Realized, betting on macro risks, when they eventually materialize, will lead to clearly directional and intense market fluctuations (whether breaking upward or downward).

Strategy Construction: Buy one out-of-the-money call option (OTM Call) and one out-of-the-money put option (OTM Put). It is recommended to choose contracts with DTE of 7-14 days to capture the volatility of short-term macro events (such as the government shutdown deadline).

Core Advantage: Directionally neutral, as long as the price moves sharply either up or down, and the volatility exceeds the net premium paid, profits can be made. Deploying this strategy when short-term IV has retreated but macro event risks have not been eliminated is an effective means to capture future spikes in IV at low cost.

IV. Disclaimer

This report is based on publicly available market data and options theoretical models, aiming to provide investors with market information and professional analytical perspectives. All content is for reference and communication only and does not constitute any form of investment advice. Cryptocurrency and options trading carry extremely high volatility and risks, which may lead to a total loss of principal. Before adopting any trading strategy, investors should fully understand the characteristics, risk attributes of option products, and their own risk tolerance, and must consult a professional financial advisor. The analysts of this report do not bear any responsibility for any direct or indirect losses resulting from the use of this report's content. Past market performance does not indicate future results; please make rational decisions.

Joint Production: Sober Options Studio × Derive.XYZ