In 2025, the market has undergone major changes, making it much more difficult to select funds.

In 2025, the overall A-share market has shown an upward trend, with the Shanghai Composite Index currently above 3800 points, reaching a new high in nearly 10 years, and investors' willingness to enter the market is continuously increasing.

In the slow bull and fluctuating market, the active excess return ability of public funds is gradually becoming apparent, with the Wind偏股混合型基金指数 rising by 33.31% this year, reaching a new high in nearly 5 years.

However, for fund investors, the difficulty of investing is clearly increasing:

On one hand, the market is not rising and falling in unison, but there is significant differentiation among industries, with some rising sharply and others declining, leading to greater market divergence.

Data source: Choice, as of 2025.10.10

On the other hand, the scale of domestic public funds has greatly expanded, exceeding 36 trillion, with the number of funds reaching 13,128 (as of the end of August).

With more and more funds, the structural market of A-shares is becoming increasingly 'trendy'—today it’s chips, tomorrow it’s new energy, and next week it may rotate back to dividends.

It is unrealistic for ordinary people to precisely step on the wind; what is more realistic is to use asset allocation to embed risk and drawdown management into daily investments.

Gary Brinson, the father of global asset allocation, once said:

In the long run, about 90% of investment returns come from successful asset allocation.

Emphasizing allocation, the work of financial management platforms has become more detailed.

Market volatility has long been present. When investing, the most important thing is not to bet on sectors and earn a lot when prices rise, but to ensure that 'when the east is bright, the west is also bright,' and 'do not put all your eggs in one basket.'

In the market, if one can remain present, using scientific asset allocation to reduce volatility, accumulating small victories into great victories, and avoiding the anxiety caused by large drawdowns, one can hold on, have a high winning rate, and thus achieve long-term returns.

In recent years, some leading third-party wealth platforms serving fund investors in China have also become clearer in their service approach, with the industry gradually shifting from emphasizing 'product selection' to 'helping users with allocation.'

I recently noticed that Ant Fortune has taken a step further: under the allocation framework, it upgraded gold-selected funds. Gold selection 5.0 has made more detailed track classifications and data presentations, and has applied gold selection classifications and indicators to all platform funds.

It is equivalent to not selling a single selection result but selling the concept of allocation and selection tools, allowing everyone to make in-depth choices from the perspective of allocation.

1. The allocation framework is clearer and omnipresent.

The interface of gold selection 5.0 further enhances the allocation function, seemingly having researched ordinary people's financial habits and made it more detailed.

Everyone wants a reference 'password' for financial management. Gold selection places the 'allocation' viewpoint at the forefront, clarifying some directions that can be allocated, making it convenient to use this framework to choose funds as needed.

Not emphasizing individual products but highlighting major category combinations can help more people develop awareness of asset allocation, avoiding the major ups and downs caused by chasing highs and lows and singular styles in the past, thus minimizing detours.

I have noticed that this advocacy for allocation is also hidden in many details.

On one hand, the current gold selection is further subdivided into four major categories, with each category highlighting risk-return characteristics, especially showcasing volatility dimensions.

For example, for stable income + funds, compared to the industry’s common performance display by month/quarter/year or lock-in period, gold selection presents low, medium, and high volatility income + based on the proportion of stocks, making the post-investment experience closer to everyone’s feelings.

On the other hand, people generally buy a specific fund first before considering allocation. Seeing the details of the gold-selected funds clearly indicates asset types and maps, making it easier to choose under the logic of allocation.

2. The tracks are more detailed, enabling deeper allocation.

The recent change in gold selection that has drawn industry attention is the addition of tracks that are closer to market conditions and allocation needs, such as 'rise-resist' funds in advanced actively managed funds.

At this stage, I am particularly focused on funds that can rise while resisting declines, as the market has risen above 3800 points, with valuation factors, geopolitical issues, interest rate cycles, industrial policies, and capital sensitivity all intensifying market volatility and accelerating sector rotations.

Funds that can rise while resisting declines pursue more stability in returns. The gold selection standard is a return rate of more than 0 over the past three years and ranking in the top 50%, with historical volatility <20%, which belongs to low volatility strategy funds. They do not lag in good market conditions and provide protection during market downturns, aligning more with individual pursuits for a balanced attack and defense in their portfolios.

In addition to major categories like broad-based, industry, global, and gold indexes, I personally think it’s essential to focus on broad-based index enhancement funds.

Gold selection funds are selected as index enhancement funds that have outperformed the index for at least two consecutive years, covering major indices such as the CSI 300, CSI 500, and CSI 1000.

In the current context of increased market volatility, 'index enhancement' products are more suitable as core bottom positions and for patient holding, reinforcing the value of 'smoothing volatility and long-term accumulation of excess returns' for fund investors.

Overall, I feel that the design structure of subdivided categories is more aligned with the commonly used 'core-satellite' logic of asset allocation.

When constructing a portfolio, you can combine actively managed funds with index funds:

Core assets can use full market/wide-based index enhancement/low volatility strategies/value styles, providing relatively comprehensive returns and risk control; while satellite assets can use major industry/sub-industry/growth styles to enhance, flexibly allocating to seize market opportunities and enhance overall returns. Additionally, bond funds, gold, and overseas index funds are included to reduce portfolio correlation and smooth volatility.

This classification allows investors with different risk preferences to have a more convenient path for portfolio allocation.

Third, the fund indicators cover the entire platform, making fund selection more transparent.

Another widely noticed change is that the indicator framework of gold selection is no longer limited to 'a few selected funds,' but is generally applied to the display and analysis of all funds on the platform, making it easier for everyone to make more transparent and personalized choices.

What is the difference between gold selection and non-gold selection afterward?

First, the core indicators of the two will differ; second, based on quantitative indicators, they must also be selected after research by the gold selection team. Gold selection will provide research, interpretation, and other reports to facilitate tracking and adjustments after allocation.

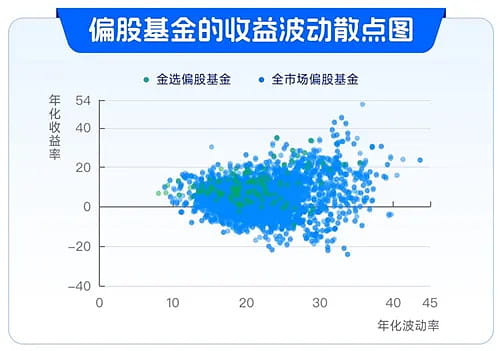

Compared to non-gold-selected funds, 'gold selection' tends to show characteristics of 'low volatility and high returns.' From the scatter plot of return volatility of all equity funds in the market, gold-selected actively managed funds are mostly distributed in the upper left area, making them overall more suitable for balanced allocation.

Data shows that investors holding gold-selected actively managed funds have a 17% higher probability of positive returns and a 7.8% higher holding return rate compared to non-gold-selected funds.

Thus, gold selection is not just 'fund recommendations,' but hopes to become a methodology and tool for allocation, ultimately evolving into a comprehensive, full-scenario investor companionship and service system.

To improve the long-term winning rate of fund investors, persistent effort is needed.

It is foreseeable that with the continuous attempts of Ant Gold Selection, there will be more and more institutions in the industry working on allocation. Research on allocation, which was previously only conducted by professional institutions, will gradually become popularized and democratized through platform services.

According to media reports, Ant Platform data shows that users with 'stock-bond allocation' have a 6% higher probability of profit compared to users holding a single asset—this corroborates the 'allocation priority' methodology.

This indicates that the threshold for professional financial management is lowering, while the holding experience for investors is improving. For fund investors, the future will no longer be just 'watching a single fund' and chasing highs and lows, but being able to select products from an allocation perspective, build a portfolio suitable for themselves, and continuously improve their understanding of the market, thereby genuinely increasing their long-term winning rate.