When interest rates drop and meet cryptocurrency, the market's anticipated surge did not come, but instead welcomed a $1.7 billion 'great escape'—and the mutual tearing between the big players revealed the harsh truth behind ETH's valuation.

The Federal Reserve's interest rate cut was originally seen as a positive signal, but the cryptocurrency market directly staged a 'plunge performance,' with $1.7 billion in liquidations in one day, setting a record high in over a year. Especially ETH was the hardest hit, with nearly $500 million in leveraged positions wiped out. But while retail investors were crying out for help, Tom Lee, who had been bullish on ETH in the bull market, was still stubbornly holding on to his optimistic view on social media, even calling out a 'long-term target of $60,000,' resulting in a hard slap in the face—his predicted support levels of $4,300 and $4,000 were all breached.

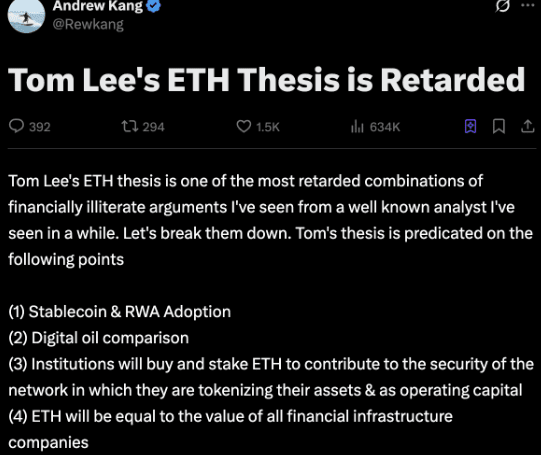

At this time, another big shot, Andrew Kang, couldn't sit still and directly blasted Tom Lee's theory as 'idiotic', throwing out five counterarguments:

Andrew Kang's Five Major Critiques

Stablecoins and RWA? ETH hasn't made any profit at all!

Tom says stablecoins and asset tokenization will allow ETH to earn transaction fees effortlessly, but the reality is: as on-chain efficiency improves, transaction fees haven't risen; chains like Solana are also stealing a large number of transactions. The most painful part is that even if trillions of bonds are placed on-chain, if they are only traded once a year, their contribution to ETH's income is less than a single USDT transfer!The metaphor of 'digital oil' is just nonsense

Oil prices have actually been oscillating in a range for a hundred years, spiking due to short-term events and then falling back. If ETH is truly a 'digital commodity', then it should be a cyclical asset, not the long-term skyrocketing target that Tom claims.Will institutions hoard ETH for staking? Dream on!

Which bank has really put ETH on its balance sheet? Institutions will only use the chain but won't hoard the native assets of the chain—just like you use delivery services but don't buy stock in the delivery company.Is ETH equal to the value of all financial companies? Absurd!

Tom says ETH will one day be worth the sum of all financial infrastructure companies, but this valuation model is purely 'building a spaceship with PPT', completely unrealistic.Technically bearish instead

ETH's price hasn't broken through major ranges for three years, and recently spiked and fell back, showing a pattern identical to crude oil's oscillating trend. If we must talk about the trend, it seems likely to oscillate long-term between $1000 and $4800.

神策's personal opinion

This debate has actually exposed two realities about ETH:

Tom Lee faction (Wall Street narrative): Using grand concepts like 'digital oil' and 'financial infrastructure' to embellish ETH, attracting institutional funds, can pump the price in the short term, but in the long term, it depends on whether the fundamentals match.

Andrew Kang faction (on-chain native faction): Burst the bubble, emphasizing that ETH's value capture ability is being diverted by other public chains, and the high valuation may just be a 'financial illiterates' carnival.'

But be aware, Kang predicted back in April that ETH would fall below $1000, yet this bull market saw ETH surge to $5000—so the big shots often slap their own faces. The key is not to pick sides but to understand that multi-chain competition is already a foregone conclusion: Solana, Arbitrum, and even Tether's own chain are all vying for the cake, and the era of ETH's dominance may truly be over.

“If the financial narrative of ETH is debunked, who will be the next to explode? Solana? Layer2? Or stablecoin public chains? Pay attention to神策, in the next issue we will break down the winning formula of the multi-chain era!#美SEC和CFTC加密监管合作 $ETH