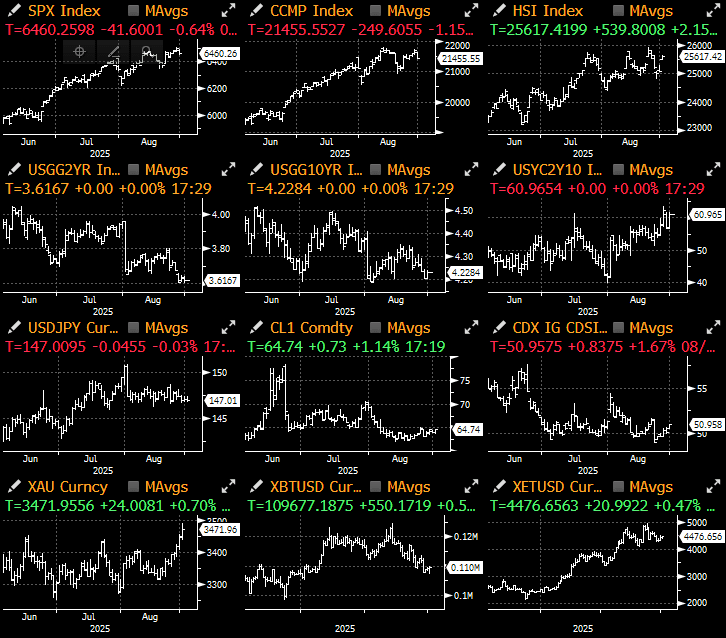

The overall market was dull last week, with the U.S. market nearly ignoring two highly anticipated events — Nvidia's earnings report and Friday's PCE data. Although U.S. stocks saw a slight increase early in the week with low volatility, prices ultimately retraced before the long weekend due to weak tech stocks (Nvidia and Dell's earnings fell short of expectations).

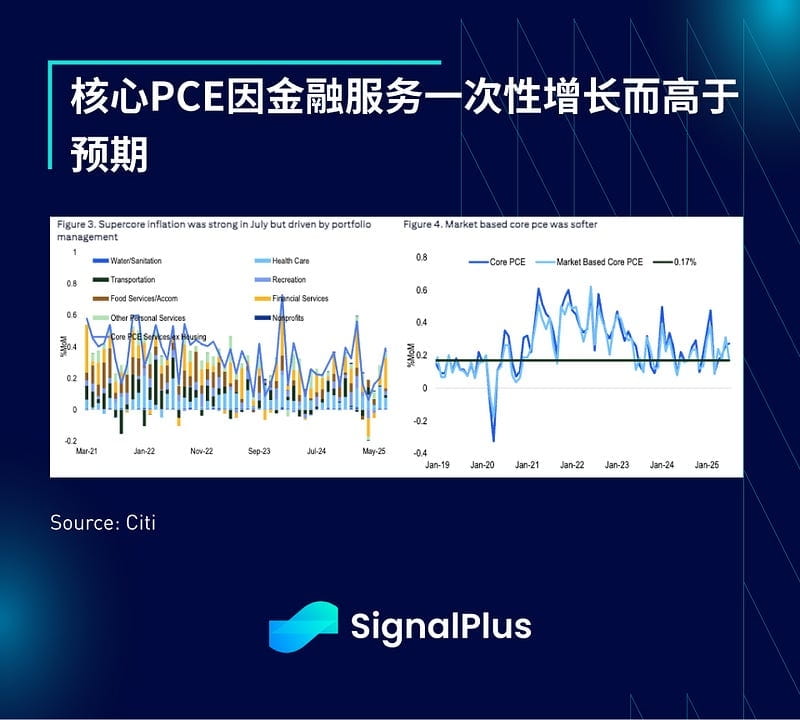

In terms of data, the core PCE inflation rose by 0.27% month-on-month in July and by 2.9% year-on-year, in line with expectations, but the “super core” service inflation unexpectedly remained strong at 0.39%. The market seems willing to overlook a one-time increase in the financial services sector, keeping government bond yields near recent lows.

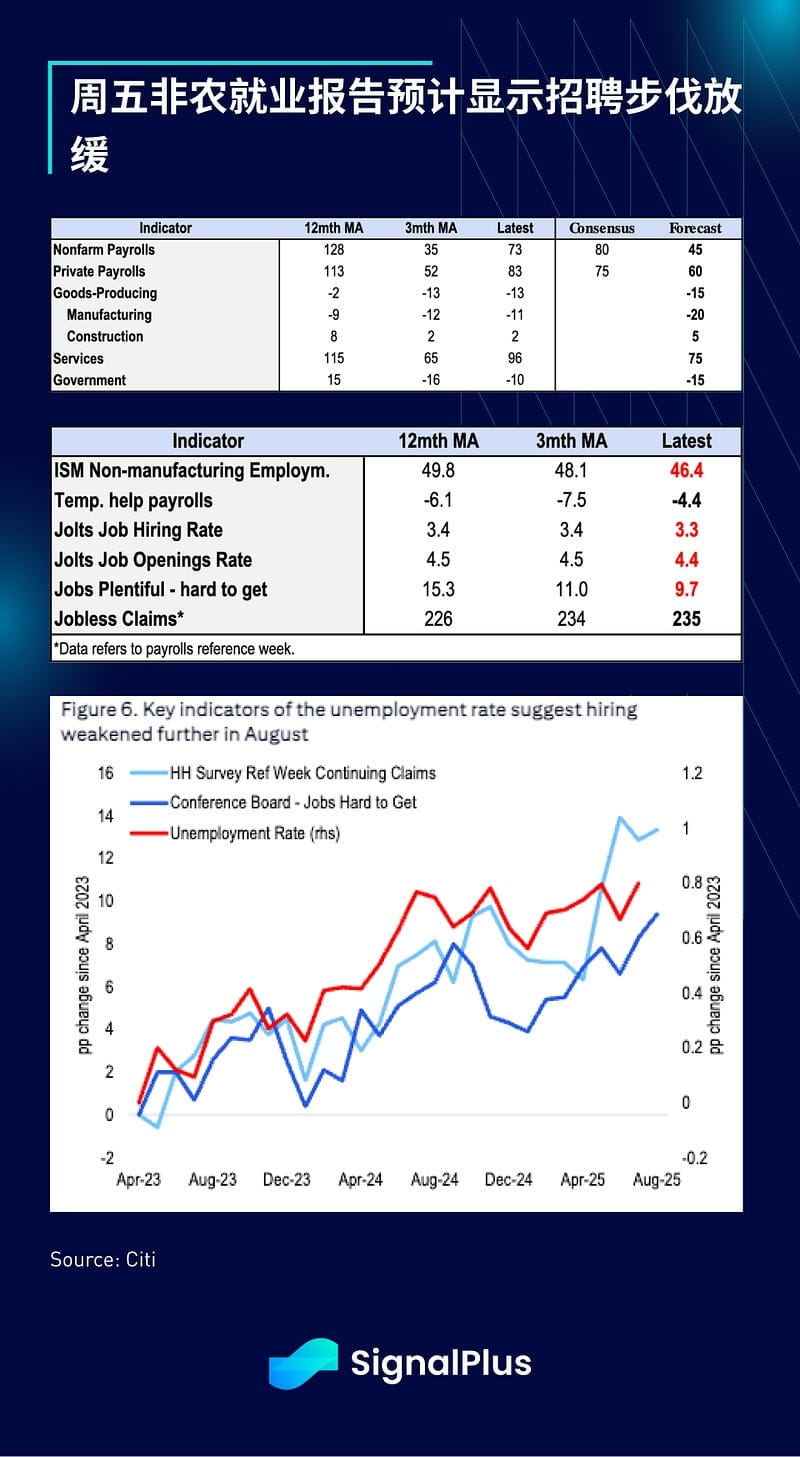

This week's focus will be on Friday's Non-Farm Payrolls (NFP) report, with the market expecting total employment to increase by about 45,000 (60,000 in the private sector) and an unemployment rate of 4.3%. Given the weak hiring demand, the trend of slowing job growth is expected to continue, with new jobs added each month reflecting the reality of economic slowdown and reduced immigration.

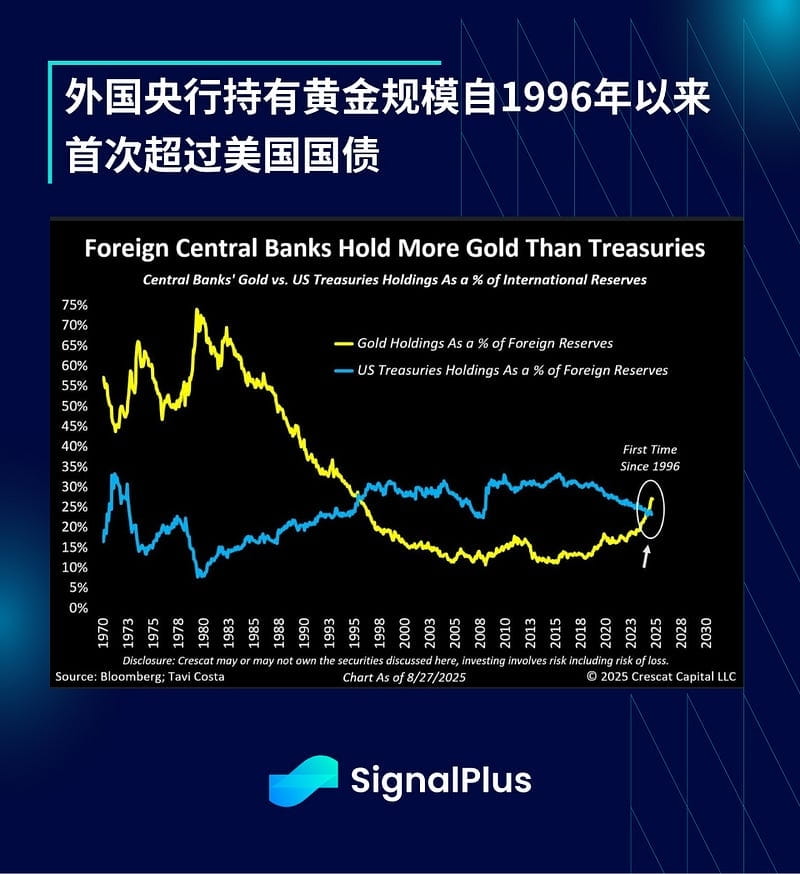

After the Federal Reserve's shift to a dovish stance following the Jackson Hole meeting, precious metals surged significantly, with gold nearing $4,000 and silver breaking above $40/ounce for the first time since 2011. Additionally, due to ongoing geopolitical pressures and persistent inflation, the amount of gold held by foreign central banks has exceeded that of U.S. Treasury bonds for the first time since 1996, and this trend is expected to continue.

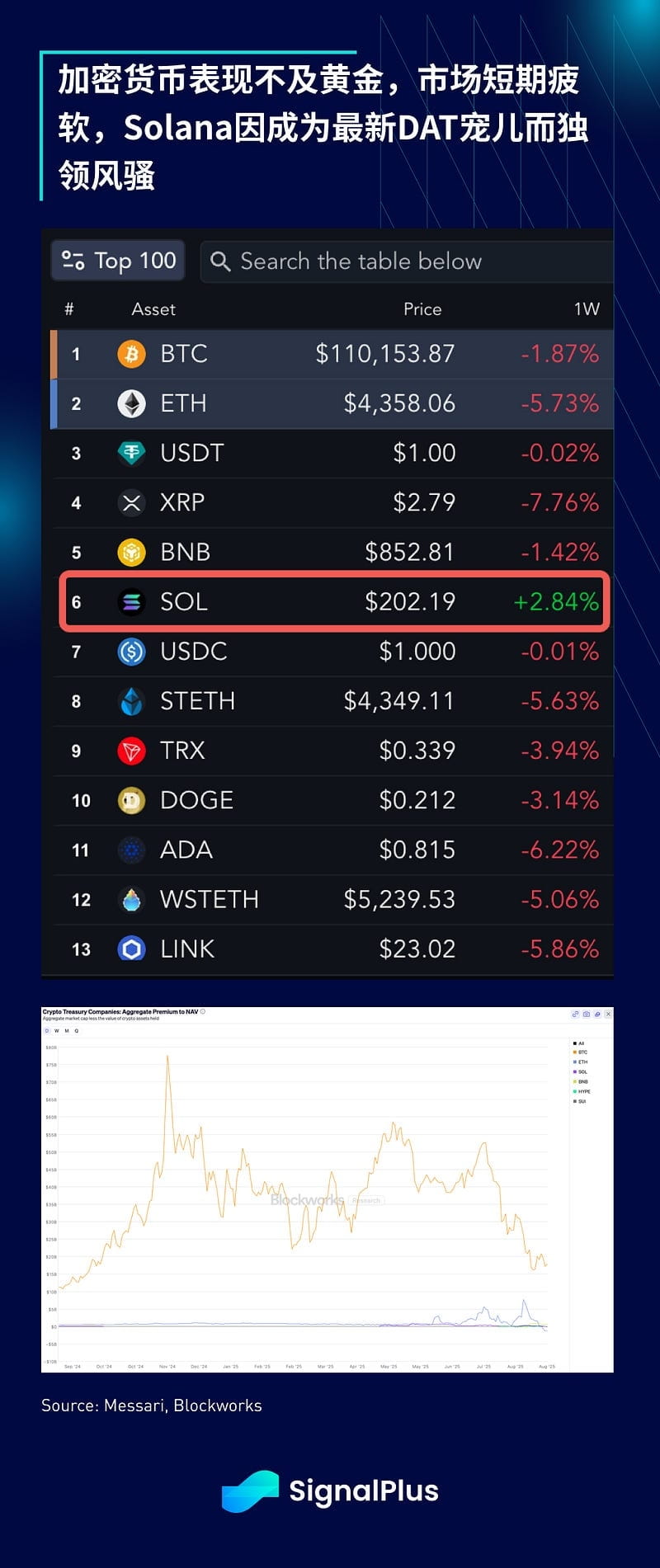

In the cryptocurrency space, despite strong performance from gold, cryptocurrency prices fell last week, and the market bubble seems to be slightly retreating, with the DAT premium overall falling back to long-term lows. New capital inflows appear to have peaked, leading to a rotation of funds, with Solana being the only cryptocurrency to rise this week, and SOL becoming the latest destination for the DAT craze, with total value locked (TVL) on-chain also showing a significant rebound.

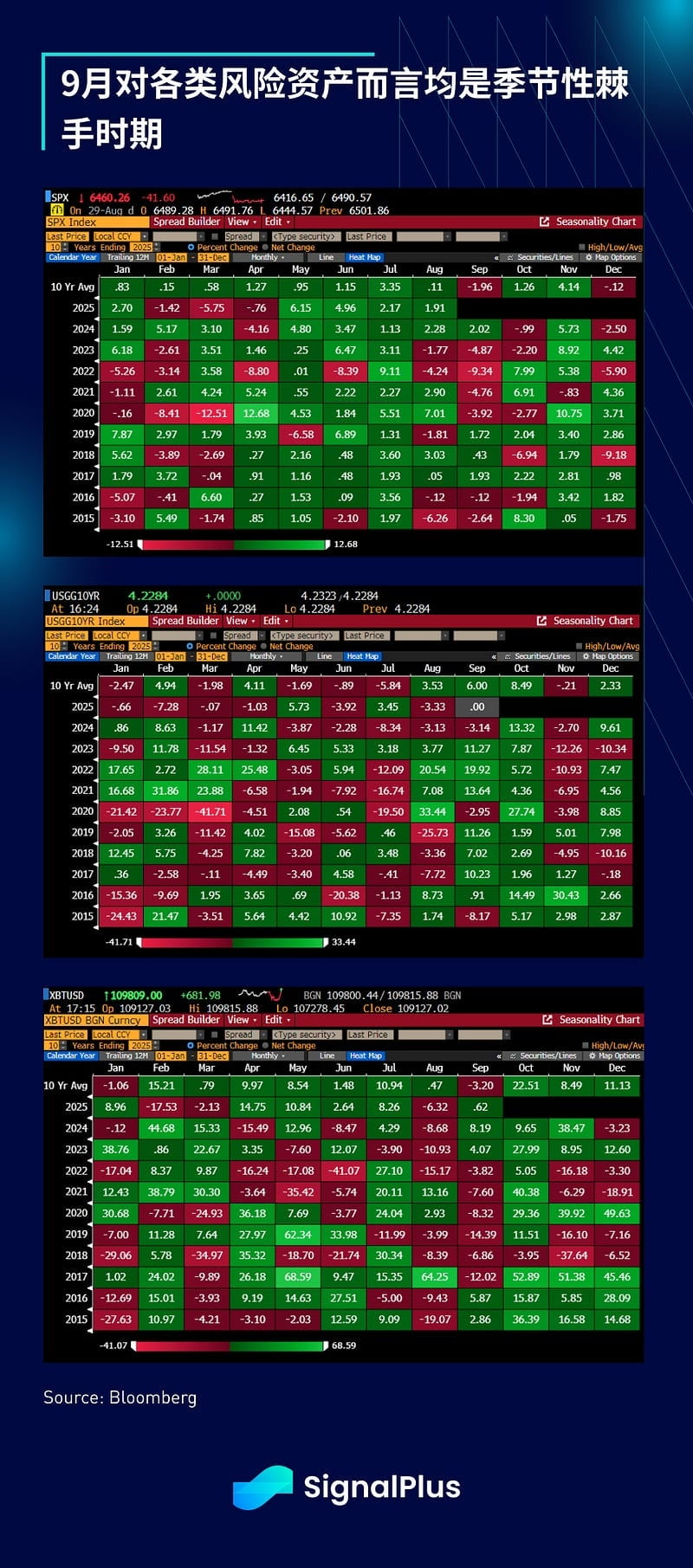

Looking ahead, we expect September to be a month of increased volatility for risk assets overall. Historically, September's seasonal performance has not been friendly to stocks (declining), 10-year Treasury yields (rising), and Bitcoin (declining) over the past decade. Meanwhile, the volatility premium is at a cyclical low, and risk leverage is accumulating. Given that the Federal Reserve has already 'front-loaded' its easing intentions, what cards can be played if risk assets decline in September?

It is currently too early to make a judgment, but as the seasonally tricky months of September to November approach, we advise caution. Wishing friends smooth trading and good luck!