Recently, global financial and technology market focus has frequently appeared: on one side, the stablecoin sector enters a 'compliance window period' due to the implementation of regulations in multiple countries, transitioning from gray tools to diverse financial infrastructure; on the other side, NVIDIA delivers a bright earnings report, yet the stock price falls against the trend by 5%, revealing issues such as supply disruption in the Chinese market and high inventory.

Stablecoins: Regulation paves the way, compliant coins become a new force.

In the second half of 2025, stablecoins will enter a global regulatory 'intensive landing period': the GENIUS Act will take effect in the US in July, and the stablecoin regulation will be officially implemented in Hong Kong in August (the world's first complete regional framework). Japan and South Korea are also accelerating the development of detailed rules, allowing compliant entities to issue stablecoins. This marks the transition of stablecoins from the 'gray growth' stage to a new phase of 'compliance and innovation running in parallel.'

The core value of compliant stablecoins lies in filling the usage gap for traditional institutions. In the past, stablecoins like USDT dominated the market, but due to insufficient transparency and operating on the regulatory edge, they found it difficult to enter scenarios such as corporate treasury and cross-border settlement. Compliant stablecoins (like USDC, PYUSD, FDUSD) are designed to be 'regulatable' from their inception: issued by licensed institutions, with reserves subject to regular audits and meeting local licensing requirements, allowing them to be included in corporate financial statements and becoming an 'official channel' connecting traditional finance with the crypto world.

Different regions' compliant stablecoins have taken differentiated paths:

United States: USDC (issued by Circle, with cash + short-term debt reserves) has become the institutional choice; PayPal's PYUSD directly enters retail payments, targeting daily consumption and cross-border transfers;

Hong Kong: First Digital's FDUSD, based on the stablecoin regulation, has become the local compliance benchmark;

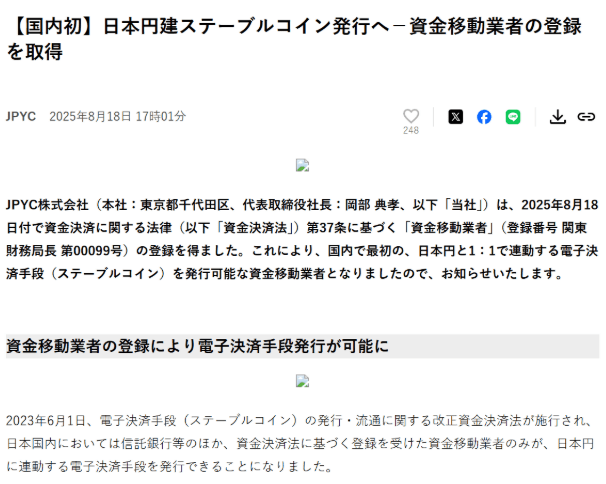

Japan: JPYC obtained a fund transfer service license, backed by government bonds as reserves, and plans to deploy multiple public chains;

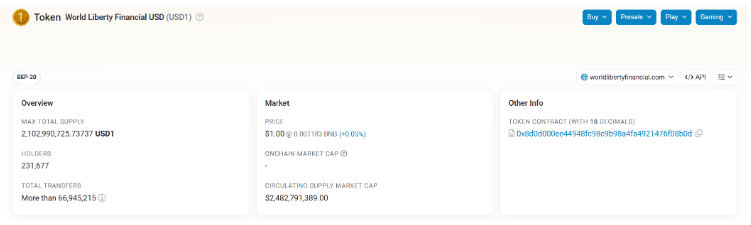

Emerging forces: USD1, leveraging resource advantages, saw its issuance reach $2.1 billion within six months, becoming the fifth largest stablecoin globally, covering major exchanges.

In the future, stablecoins will not simply be 'compliance replacing gray areas,' but will form a multipolar landscape: USDT will continue to serve as the liquidity engine of the crypto market, while compliant coins will penetrate real financial scenarios, with yield-type and non-USD stablecoins filling niche demands, completely moving away from a 'single narrative.'

NVIDIA: Bright earnings report fails to save stock price amid three major challenges.

On August 27, NVIDIA announced its Q2 2025 earnings report: revenue of $46.7 billion and net profit of $26.4 billion, both exceeding market expectations. The data center business (accounting for 88%, with revenue of $41.1 billion) remains the core pillar, and Blackwell chip shipments increased by 17% quarter-over-quarter. However, after the earnings report, the stock price fell by 5%, revealing three major hidden concerns behind the bright data.

1. Supply disruption in the Chinese market: H20 shipments fell to zero, revenue proportion halved.

NVIDIA's Q2 shipments of H20 chips to China were zero—this chip, originally compliant with export rules, completely lost the Chinese market due to the tightening of US regulations in April and instructions to Chinese companies to avoid use. Previously, China accounted for 15%-20% of NVIDIA's revenue, contributing only $2.8 billion this quarter (5.9% of total), showing a significant gap. Although Jensen Huang had expressed hope to promote H20's licensing, policy uncertainty still worries the market.

2. Conservative financial forecast + high inventory: Growth expectations cool down.

NVIDIA's financial forecast for Q3 is only 1% higher than market consensus, and Q2 inventory surged to $14.96 billion (a 30% year-over-year increase). The official explanation is to stock up for the Blackwell chip, but the market questions whether this is related to declining demand for older models H100 and H200, compounded by Microsoft reducing data center investments and tech giants developing their own AI chips, causing investors to worry that growth may 'hit the brakes.'

3. Response strategy: new chips + $60 billion buyback to save the situation.

To alleviate pressure, NVIDIA plans to develop the Blackwell architecture chip B30A compliant with the latest regulations, aiming to restart its business in China (Jensen Huang stated that China's AI market is growing by 50% annually, worth $50 billion, and should not be abandoned); at the same time, it announced a $60 billion stock repurchase plan and will distribute a cash dividend of $0.01 per share in October, attempting to stabilize shareholder confidence.

Conclusion: Regulation and geopolitics are key variables in the market.

The 'compliance transformation' of stablecoins and NVIDIA's 'China dilemma' are essentially reshaping industry logic through external environments: the competition of stablecoins has shifted from 'competing for liquidity' to 'competing for compliance and scenarios,' and NVIDIA's growth has shifted from 'relying on product strength' to 'relying on geopolitical policy breakthroughs.' The future direction of these two types of assets will heavily depend on the implementation of regulatory details and international policy games, and investors need to pay close attention to the dynamics of these two major variables.