In mid-August, ETH strongly broke through $4,700, reaching a four-year high, while SOL mostly fluctuated between $180–$200 during the same period, far behind the price performance of BTC and ETH. Reflecting on the Meme frenzy sparked by Solana on platforms like Pump.fun in 2024, it was once seen as the terminator of ETH. On January 19, 2025, SOL refreshed its historical high to around $293, then retreated, consolidated, and fluctuated in sentiment, forming a divergence with ETH's 'strengthening trend.' Behind the surface lies a systemic difference in funding entry, value anchoring, and network narrative. So what is the reason behind this? Can the Solana ecosystem create glory again, and can the SOL token take off once more?

Solana's growth path is clearly different from Ethereum: it does not capture value through 'high Gas fees + deflation,' but through single-chain high throughput + ultra-low fees supporting massive long-tail and high-frequency trading.

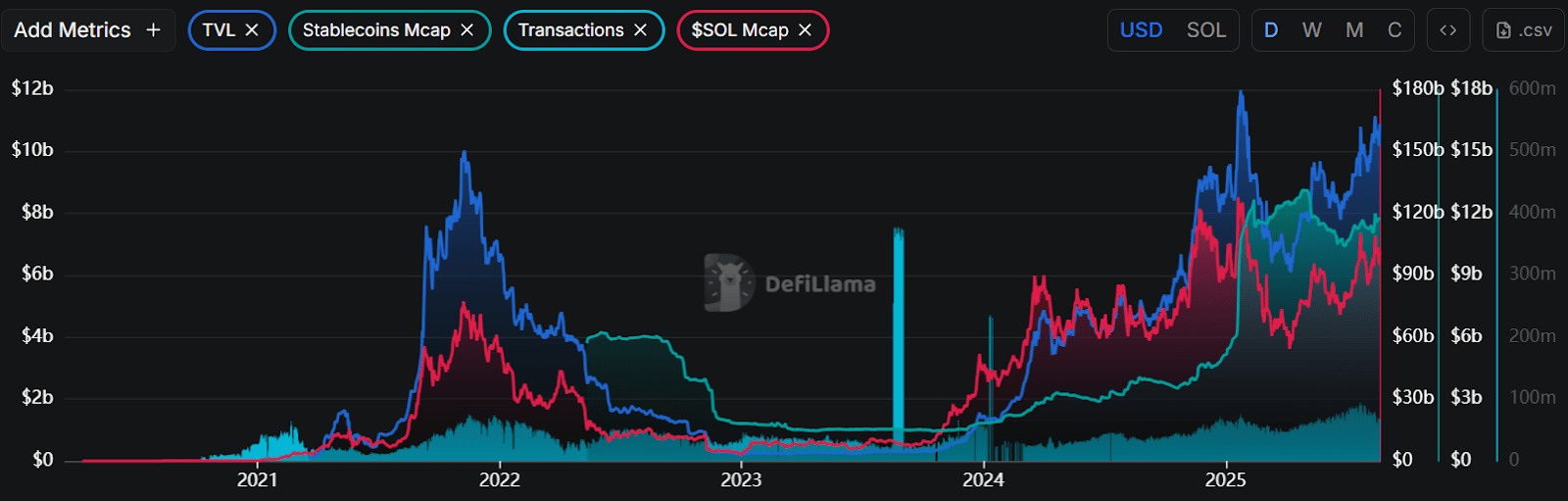

Since the beginning of this year, the Solana ecosystem has shown a 'high-level pullback followed by a rebound' trend. TVL and stablecoin supply have shown stair-step increases, with current TVL around $10.42 billion and stablecoin market capitalization around $11.62 billion, indicating that the on-chain 'underlying dollar liquidity pool' has returned to and stabilized in the $10 billion range; on-chain transaction counts remain high, maintaining an active 'high-frequency/long-tail' trading state; $SOL's total market capitalization sharply fell in Q1 but began to show a wave-like upward rhythm from Q2; from a structural change perspective, the resurgence of Meme enthusiasm has marginally improved DEX/chain fees but has not yet returned to this year's peak.

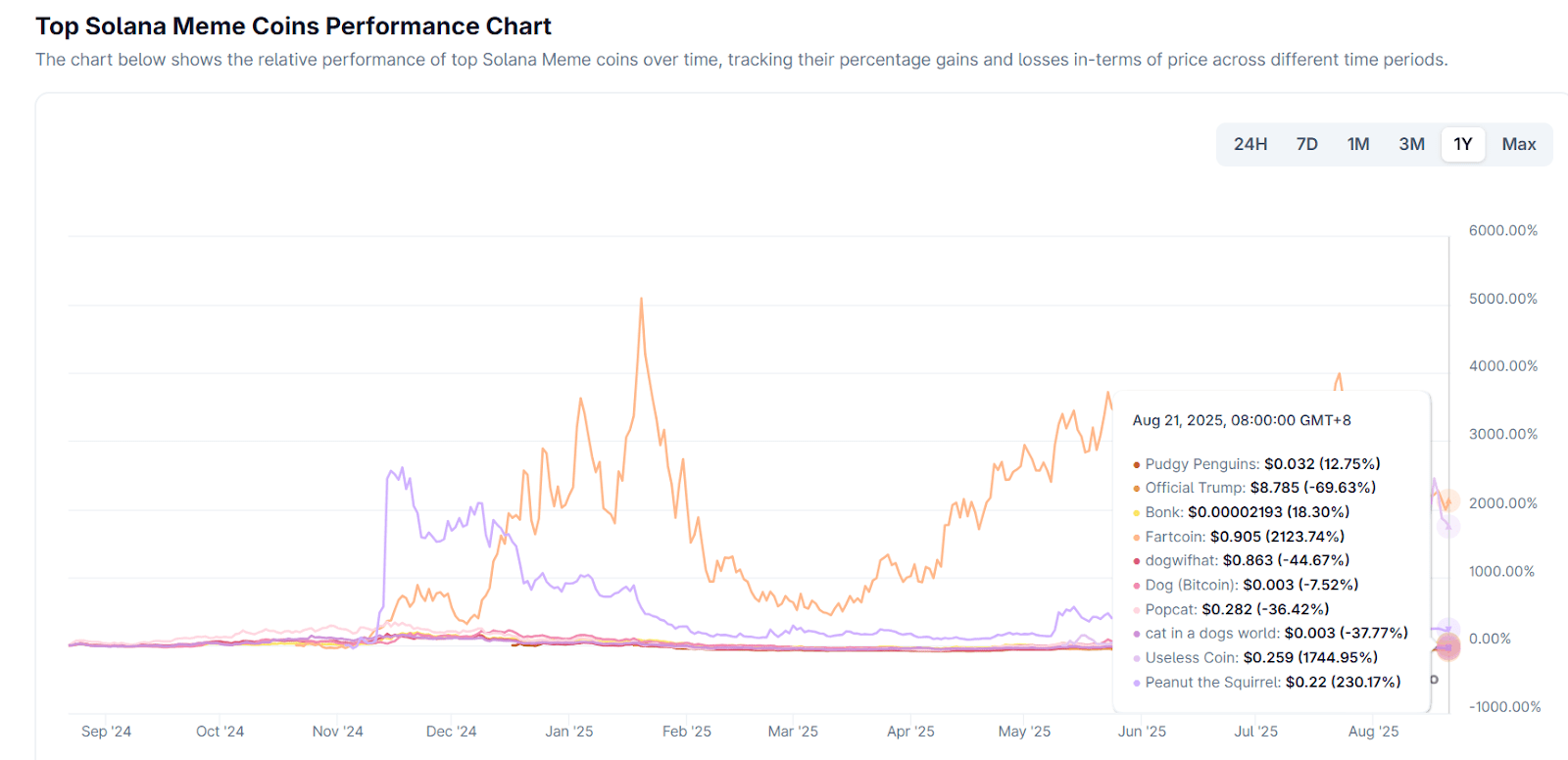

As the leading network for Meme coins, Solana has produced star Meme coins such as BONK, WIF, POPCAT, MOODENG, PNUT, TRUMP, PENGU, FARTCOIN, USELESS, etc. The common characteristics of Solana Meme are 'high volatility + strong rotation + strong event-driven.' Currently, the total market capitalization of the Solana Meme sector is approximately $11.7 billion. The top 5 hottest Meme coins since the beginning of this year are as follows:

PENGU: A 'brand coin' closely tied to popular NFT IP, with physical toy sales exceeding $10 million, covering over 3,100 stores, and Canary Capital has submitted a PENGU ETF application to the SEC.

Please, significantly strengthen within the year, with market capitalization ranking among the top of Solana Meme.

BONK: Solana's dog-themed 'veteran' and community traffic entry, has seen noticeable growth with the rise of LetsBonk.fun, but currently shows significant withdrawal.

TRUMP: A Trump Meme, driven by political topics and sentiment, has been in overall decline since its launch in January; the Trump crypto dinner in May sparked a wave of recovery, but it is still in a downtrend, sensitive to event catalysts.

FARTCOIN: Its popularity stems from a humorous theme and viral spread: users submit fart jokes or memes to earn coins, with each transaction producing a digital fart sound, combined with AI narratives (created by AI Truth Terminal), being labeled as an AI-meme hybrid, easily triggering FOMO.

USELESS: USELESS emphasizes 'uselessness' as a selling point, mocking the hollow promises of other coins, becoming the most honest meme coin, with higher prices making it more useless, thus attracting speculation more easily.

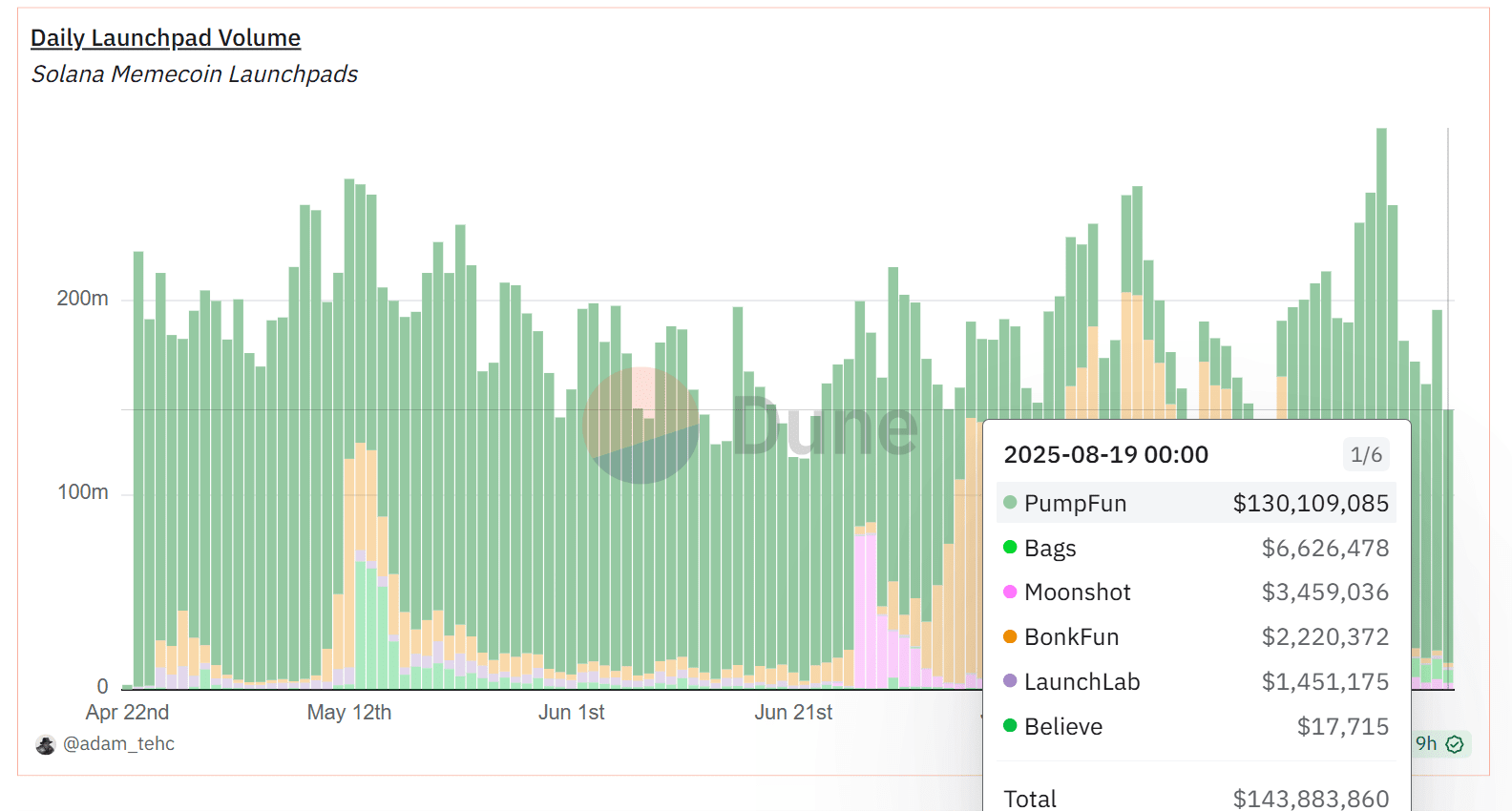

The competition for Launchpads on Solana has evolved from 'who is cheaper/faster to list' to a contest of 'creator economy, token buybacks, and community governance.'

Pump.fun: Ignited the entire chain Meme with a 1% transaction fee and 'foolproof issuance.' In mid-August 2025, its weekly revenue was approximately $13.48 million, returning to a high point; cumulative revenue has surpassed $800 million; simultaneously, the dramatic reversal of market share from 5% to ~90% in two weeks has attracted nationwide attention.

LetsBonk.fun: Rapidly rose after launching in April 2025, capturing over 78% of the issuance share in July, but later experienced a decline in share. Its 'community mobilization + low-threshold issuance' path remains one of the core competitors of Pump.fun.

Bags: Focuses on the 'creator profit sharing/royalty' route, emphasizing creator income and continuous distribution, targeting a niche route connected with opinion leaders/creators, with trading volume surpassing $1 billion in the past 30 days.

Moonshot: A fiat-entry-level app that supports Apple Pay direct top-ups and fiat deposits. It once topped the U.S. App Store's 'Finance Free Apps' chart, significantly lowering the entry barrier for newcomers.

Believe: A social media entry point that 'issues tokens for replies,' faced controversy from June due to pausing part of the on-chain revenue sharing/turning to offline payments and adjusting automatic listings to 'manual review.'

Solana's DeFi is more like 'high-frequency/long-tail trading infrastructure.' Raydium/Orca carry out DEX trading and liquidity, Jupiter/Drift handle derivatives trading and route fragmented liquidity, Kamino enhances capital efficiency, and Jito/Marinade provide 'stable yields + liquidity' as underlying assets.

Raydium (AMM + Ecosystem Launchpad): A veteran DEX/AMM on Solana, responsible for most long-tail spot liquidity and launchpad functions; fees and revenue rank among the best in the long term, showing positive feedback on 'platform cash flow - token value.'

Jupiter (Aggregator + Trading Entry): Solana's default-level router, integrating liquidity from Raydium and other DEXes; the JPL pool aggregates a large amount of liquidity and has announced the upcoming launch of a lending section.

Kamino (Unified liquidity/lending/market-making position management): Known for 'active market-making treasury + lending,' consistently ranks at the top of Solana's TVL, becoming a 'hub for LPs and funds.'

Jito (LST + MEV infrastructure): Makes MEV explicit through the Jito client/block engine/'Bundles' and allocates part of the MEV to stakers via jitoSOL. Jito tips have accounted for a significant proportion of the on-chain 'real economic value (REV).'

3. Analysis of reasons why SOL underperformed ETH.

ETH has established a complete closed loop with the spot ETF for 'compliant funds → secondary liquidity → market making/derivatives,' combined with a larger corporate treasury size and the narrative of 'on-chain financial hub,' forming stronger capital attraction and valuation anchors; Solana focuses on a trading ecosystem of 'high-frequency/long-tail applications,' with price elasticity more dependent on thematic prosperity (Meme/Launchpad, etc.), making it easier to 'lose its anchor' during risk aversion or thematic rotation.

1. ETF funding increment gap.

SOL: There is already a Solana ETF (SSK) with staking yields in the U.S. stock market; however, its structure is complex and it is not a SEC-registered spot ETF, with cumulative net inflows of only about $150 million since listing, far less than the fund-raising capability of ETH ETFs. The short-term market focus is on VanEck and Grayscale's application for SOL's spot ETF; if approved around October, it could open similar compliant models and passive funding channels as ETH.

ETH: The scale of the spot ETF has surpassed $22 billion, becoming the main entry point for institutional funds. Leading institutions (such as BlackRock) are advancing applications for 'stakable ETH ETFs.' If successful, it will combine 'staking yields' with 'compliance channels,' further solidifying long-term allocations.

2. Corporate holding size gap.

SOL: Upexi, known as 'SOL micro-strategy,' currently has an NAV of approximately $365 million, holding 1.8 million SOL, and has invited Arthur Hayes to join the advisory committee to strengthen its strategy and voice; other listed companies (like DFDV, BTCM) are also slowly increasing their holdings, but the overall scale still has a significant gap compared to ETH's treasury strategy.

ETH: BitMine Immersion (BMNR), which considers itself 'ETH micro-strategy,' plans to raise its financing scale to $20 billion, with a current NAV of approximately $5.3 billion, second only to Bitcoin's MicroStrategy; at the same time, backed by globally influential opinion leaders like Tom Lee, it significantly strengthens market narratives and funding appeal.

3. Differences in network narrative positioning.

Solana: More inclined towards 'single-chain high throughput + extremely low fees' as consumer-grade applications and speculative hotspots (Meme, Launchpad). Despite several attempts to penetrate RWA this year, most have ended in failure; in August, CMBI × DigiFT issued U.S. dollar money market fund tokens (CMBMINT) on Solana, a rare positive case of compliant RWA, causing SOL to rise above $200 on that day, seen by the market as the starting point for a potential narrative shift.

Ethereum: Ethereum is building compliant and sustainable on-chain financial infrastructure and clearing layer status, receiving 'structural subscriptions' from institutions. Half of the stablecoin issuance volume and about 30% Gas occur on Ethereum; meanwhile, Robinhood is launching stock tokens on Ethereum L2 and Coinbase is fully developing Base.

4. Different value capture mechanisms.

Solana: Achieves ultra-high interaction density through low fees + high throughput, with value capture relying more on total transaction volume and application layer fees/MEV, etc.; as Meme/long-tail activities subside, chain and application fees cool simultaneously, leading to a weakening of valuation anchors.

Ethereum: EIP-1559 burns base fees directly, showing net deflation/low inflation during busy periods, coupled with staking yields, forming a valuation anchor of 'supply-side contraction + cash flow.'

5. Historical risk memory and 'credibility discount.'

Solana: The approximately 5-hour downtime on February 6, 2024, and subsequent decline in certain consensus nodes, though repaired, still remains a risk factor in institutional pricing tables.

Ethereum: 'Non-stop' and a broader developer/compliance ecosystem lead to a lower credibility discount—when macro volatility rises, this discount is magnified by the market.

4. Can SOL take off again: Analysis of strengths/weaknesses.

SOL has the fundamentals of 'high activity + low fees + MEV sharing + application layer cash flow,' coupled with catalysts like spot ETFs and RWA compliance, making it fully capable of riding another trend; however, in the absence of ETF increments, the treasury scale and narrative still lag behind ETH, and historical stability shadows have not been thoroughly digested, the price remains highly 'event-driven.'

1. SOL's advantages and bullish logic.

Single-chain throughput + low fee rates = natural soil for activity and long-tail assets.

Solana handles tens of millions of interactions per day on a single chain, with inherently active trading and market-making, and extremely low fees, which is conducive to the continuous trial and diffusion of Meme, long-tail assets, and high-frequency DeFi.

Compliant RWA is being prototyped.

CMBI × DigiFT plans to tokenize U.S. dollar money market funds and deploy them across multi-chains like Solana/Ethereum, claiming to be the first publicly compliant MMF on Solana, bringing 'cash-like assets interpretable by institutions' and fiat/stablecoin entry. This is a potential 'long-term funding narrative.'

Predictable inflation curve.

Solana's established inflation model: initial 8%, decreasing by 15% every 'year' (~180 epochs), long-term 1.5%. The actual annualized rate is expected to be around 4.3%–4.6% in 2025, and there are discussions about community-driven proposals to accelerate deflation. Anticipated downward inflation is favorable for medium to long-term valuation anchoring.

If the spot ETF is approved = 'funding floodgates' open.

Institutions like VanEck have submitted or updated S-1 documents for SOL's spot ETF to the SEC; once approved, it will replicate ETH's 'compliant funds → passive allocation → market making/derivatives' path and attract more corporate treasury participation.

2. SOL's disadvantages and bearish logic.

The true incremental growth of ETFs is still on the horizon.

The scale of ETH's spot ETF is > $22B, forming a closed loop of institutional funds; while SOL is still in the application/communication phase, the current 'staked' products in the U.S. are not standard SEC spot ETFs, thus lacking in attracting funds. Realized vs. expected, directly reflected in relative returns.

The gap in size between treasury strategies and 'spokespersons.'

The 'treasury companies' of the ETH camp (such as BMNR, etc.) are significantly larger than those in the SOL camp (such as Upexi), backed by frontline opinion leaders like Tom Lee; while the SOL treasury is still in the 'catch-up phase.' This means greater ammunition in times of turmoil.

Network narrative of 'financial hub vs. consumer/speculative chain.'

ETH firmly occupies the narrative high ground of stablecoins/clearing/compliant finance; Solana relies more on Meme/Launchpad/long-tail to drive activity and fees, and thematic rotation directly affects on-chain fees and cash flow, making price anchors more 'floating.'

Fee competition stemming from ETH itself.

The reduction in fees on Ethereum's mainnet, along with competition from networks like BSC, Base, and Sui, means that 'low fees' is no longer Solana's sole selling point, leading to a diversion effect on new developers and funding.

5. Q3–Q4 SOL trend outlook and summary.

The essence of Solana is still 'high activity, low fees, and application monetization' as a consumer-grade high-frequency chain. Whether it can 'take off again' in Q3–Q4 depends on whether ETFs can bring in compliant increments, whether RWA can run through a scaled closed loop, and whether network stability continues to improve.

Baseline scenario: Q3 enters a phase of 'trading recovery + narrative waiting' with an upward fluctuation. On-chain activity and DEX/perpetual transactions maintain high levels, with Meme showing a cycle of impulsive activity - retraction - and renewed activity. In terms of price, SOL is roughly pulled back and forth around the 'valuation center raised by fundamentals' and 'risk premium contraction of event expectations,' with a tendency towards upward fluctuation.

Bullish scenario: If the spot ETF is approved or enters a clear effective window around Q4, coupled with the regularization of RWA issuance (not just individual MMFs, but more government bonds/bills/fund products), then the three elements of SOL's 'funding floodgates, sustainable cash flow, and network resilience' will be simultaneously strengthened, and prices are expected to experience a trend upward, potentially breaking previous highs.

Bearish scenario: If the ETF is delayed again or rejected, and Meme/Launchpad activities significantly retreat, while other major chains introduce innovative features or hot topics, it may trigger a loosening of valuation anchors and a contraction of trading beta; if combined with macro tightening or further significant fee reductions on Ethereum mainnet/L2, SOL will enter a structure of 'high volatility downturn - weak rebound.'

Solana experienced rollercoaster-like fluctuations in popularity in 2025. From the dazzling heights of the Meme frenzy at the beginning of the year to relative obscurity facing ETH's aggressive pressure by mid-year, the market's positioning of Solana has oscillated multiple times. However, what is certain is that the unique value of Solana as a high-performance public chain remains prominent, and its ecosystem has not stagnated due to a temporary cooling. In the long run, whether Solana can lead again depends on its ability to convert its high-speed network advantage into sustained user value: it must retain users after the speculative tide recedes and explore broader application boundaries; it must also gain the trust of mainstream capital and share in the compliance process. Fortunately, we are already seeing signs: whether in institutional layouts, technological upgrades, or ecological narrative transformations, Solana is gathering strength. Perhaps the current pullback is more like a buildup, waiting for another opportunity to take off.