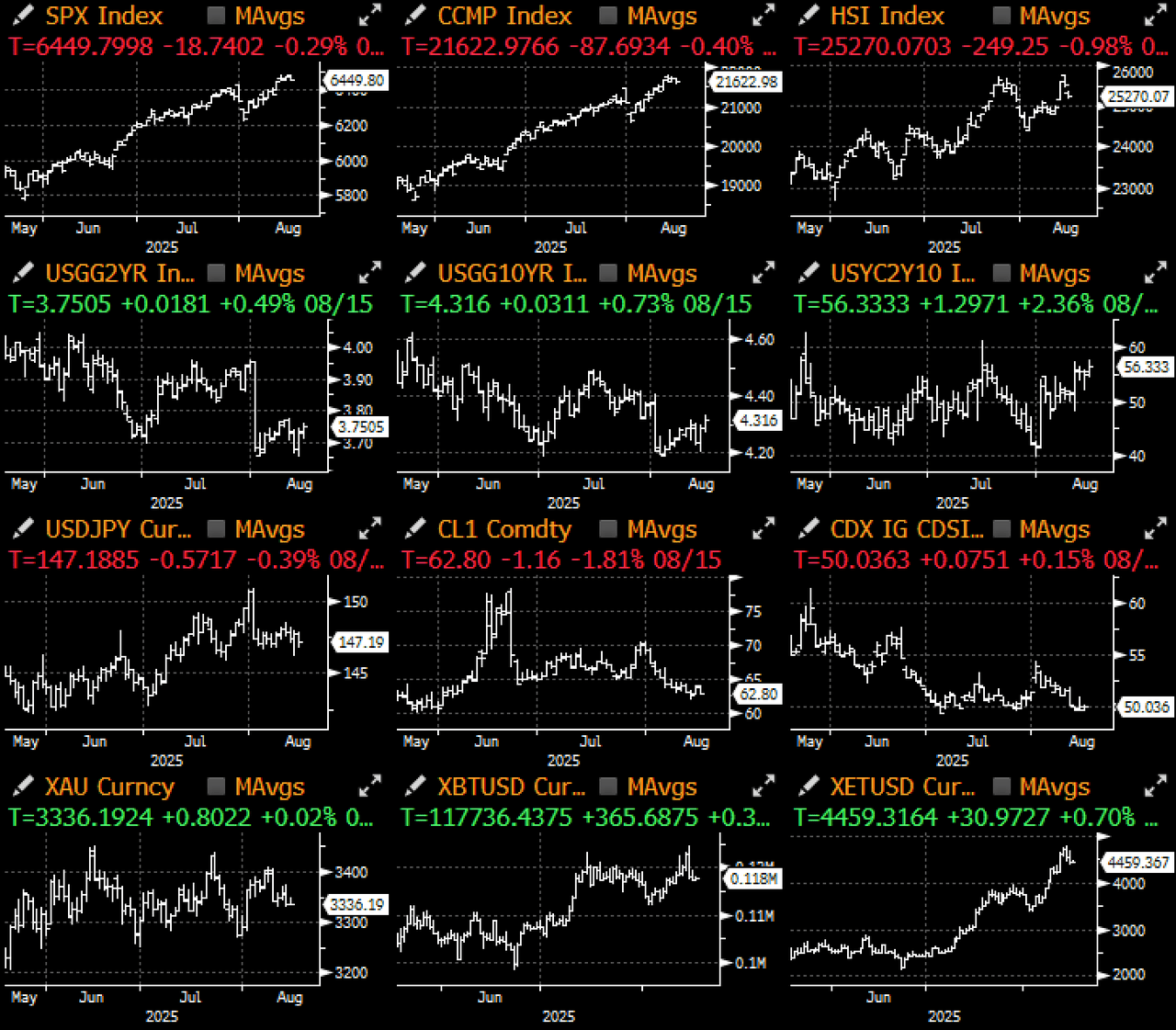

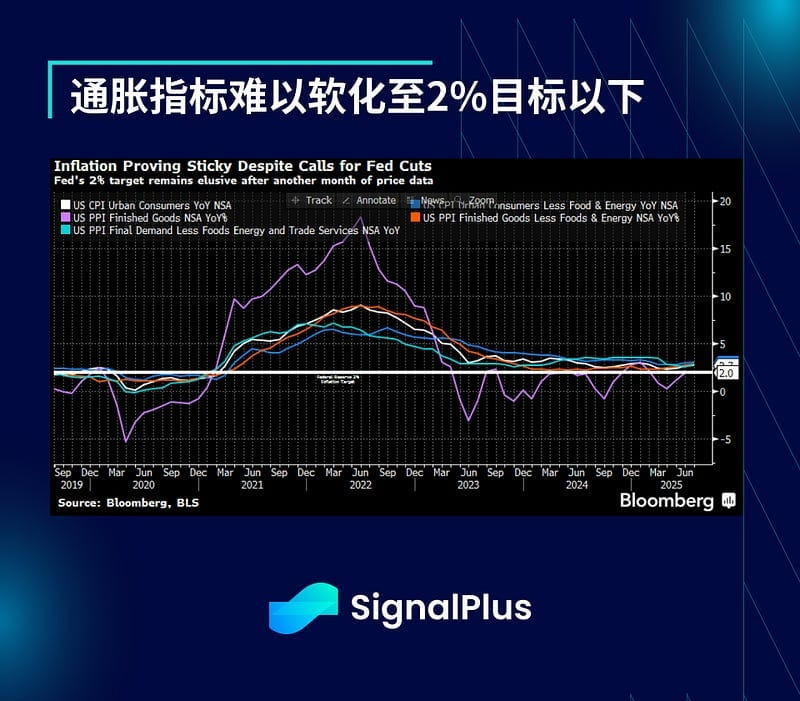

We ended a volatile week that ultimately closed within range, with the latest inflation indicators showing a mixed trend: following a mild CPI (Consumer Price Index) the previous week, July's PPI (Producer Price Index) unexpectedly surged (month-over-month +0.9% vs +0.2% expected, primarily driven by a spike in professional services prices).

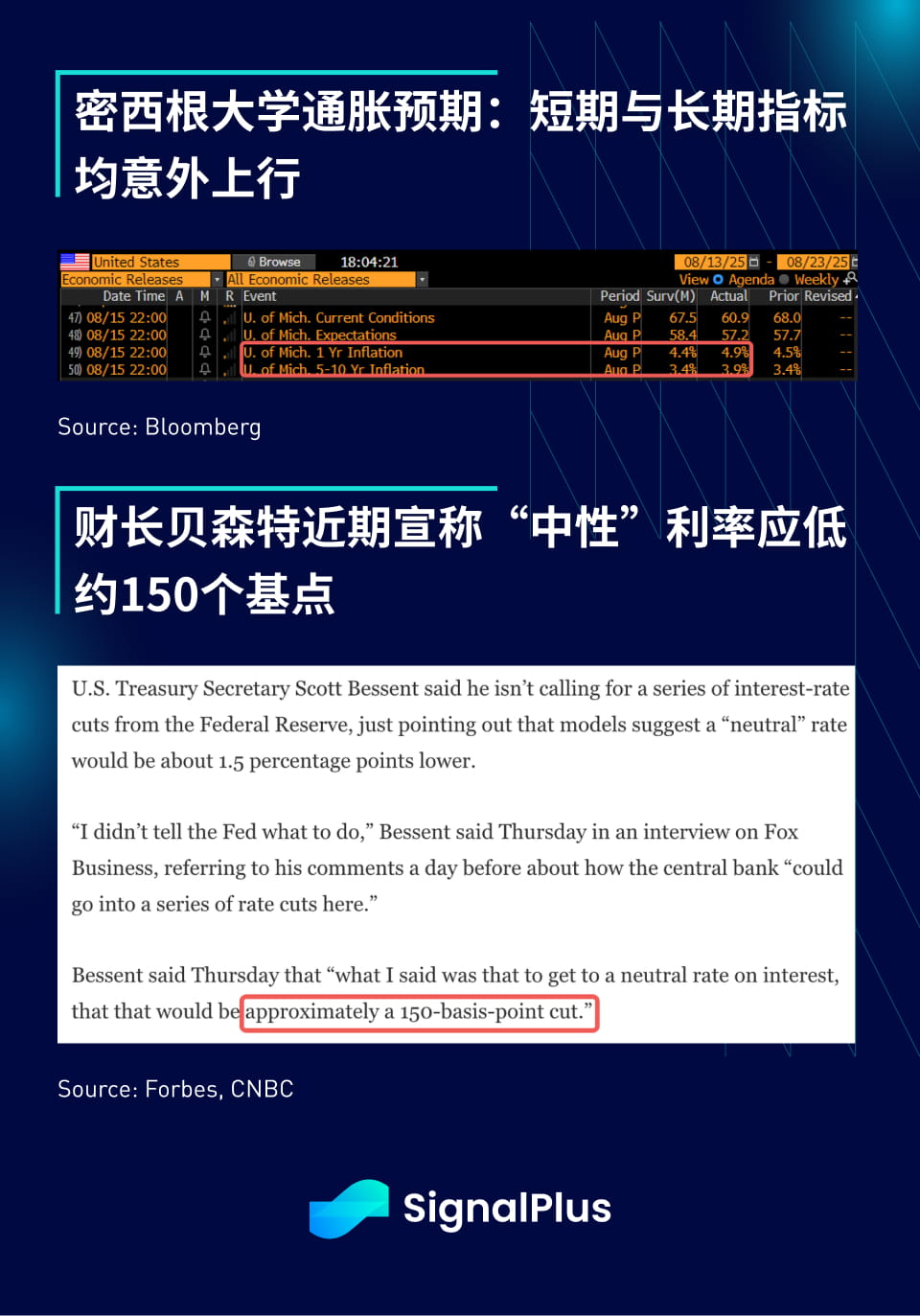

To make matters worse, the Michigan University inflation expectations data is also high, with both 1-year and 5-10 year price expectations significantly exceeding forecasts (1-year: 4.4% vs 4.9% expected; 5-10 year: 3.4% vs 3.9% expected). Despite disappointing inflation data, Treasury Secretary Basent continues his dovish rhetoric, claiming that according to their economic 'model', the neutral interest rate should be 150 basis points lower. This is undoubtedly influenced to some extent by President Trump's ongoing agenda to maintain low interest rates.

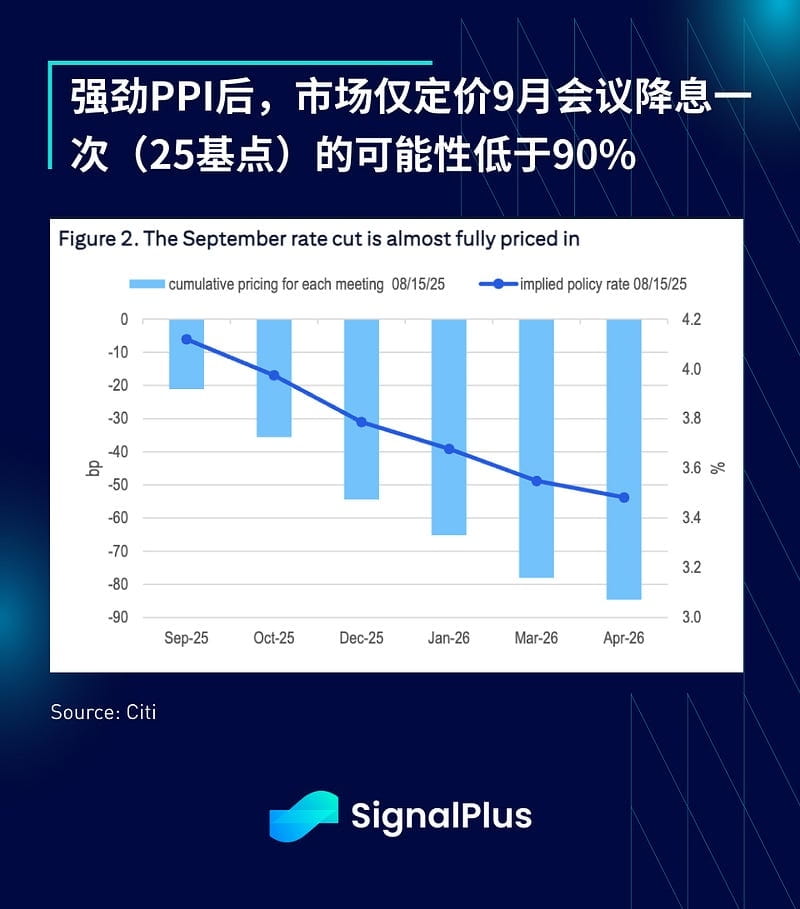

Despite the official optimism, the market naturally has its own judgments. The hotter inflation data suggests that tariff costs may be passing on to consumers at a faster-than-expected rate, leading to a rebound in the dollar/Treasury yields and a drop in gold prices. Hopes for a 50 basis point rate cut at the September meeting quickly evaporated, and as of Friday's close, the market only priced in about a 90% probability of a single rate cut (25 basis points). However, the market still expects slightly more than two rate cuts by the end of the year.

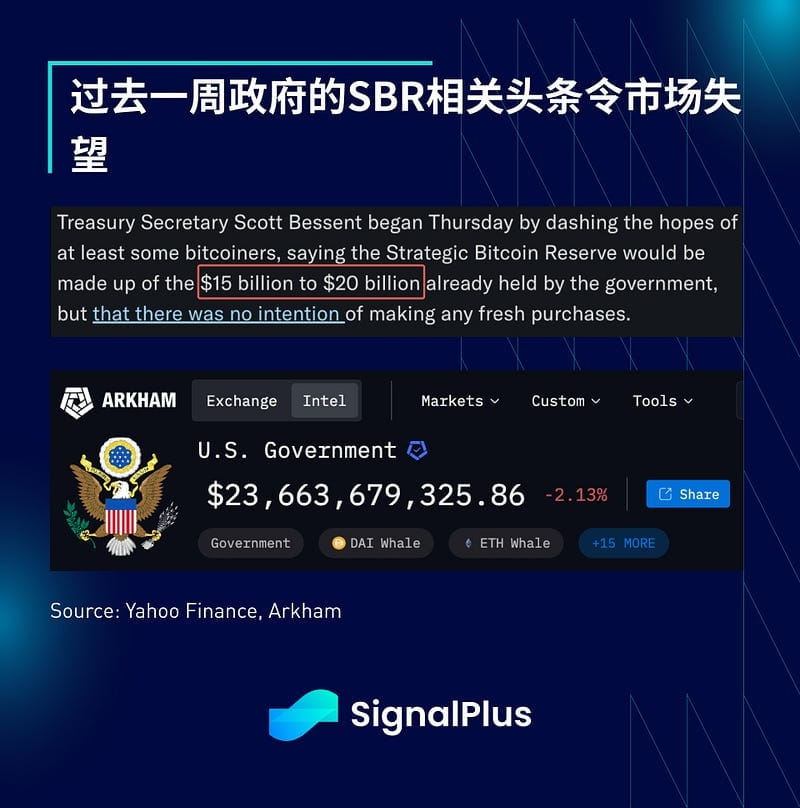

In the past week, cryptocurrency prices have stagnated, with macro factors increasing short-term resistance. Treasury Secretary Basent announced that the value of BTC held by the US government is close to $15-20 billion, rather than the over $23 billion that the market had hoped for, which disappointed the market. More importantly, he further disappointed observers by stating that the government would not purchase more BTC for its 'strategic Bitcoin reserves' and does not expect the government to re-evaluate or sell its gold reserves (valued at $42.22 per ounce) in exchange for Bitcoin.

On the other hand, ETF inflows remain very strong. Bloomberg reports that BTC and ETH ETFs recorded the largest single-week inflow since their launch last week, placing this duo among the top five of all equity ETFs. This movement is mainly driven by a surge in ETF inflows, with a weekly inflow of $17 billion, breaking the previous record.

Looking ahead, the focus will shift to the Jackson Hole meeting later this week. Federal Reserve Chairman Powell's speech will be closely scrutinized by macro observers to assess the policy tone for the remainder of the year. However, given the current inflation backdrop, we do not expect too many new dovish surprises. Unless the September Non-Farm Payroll report (NFP) is very negative, it is unlikely to drive the market to reprice the possibility of a 50 basis point rate cut.

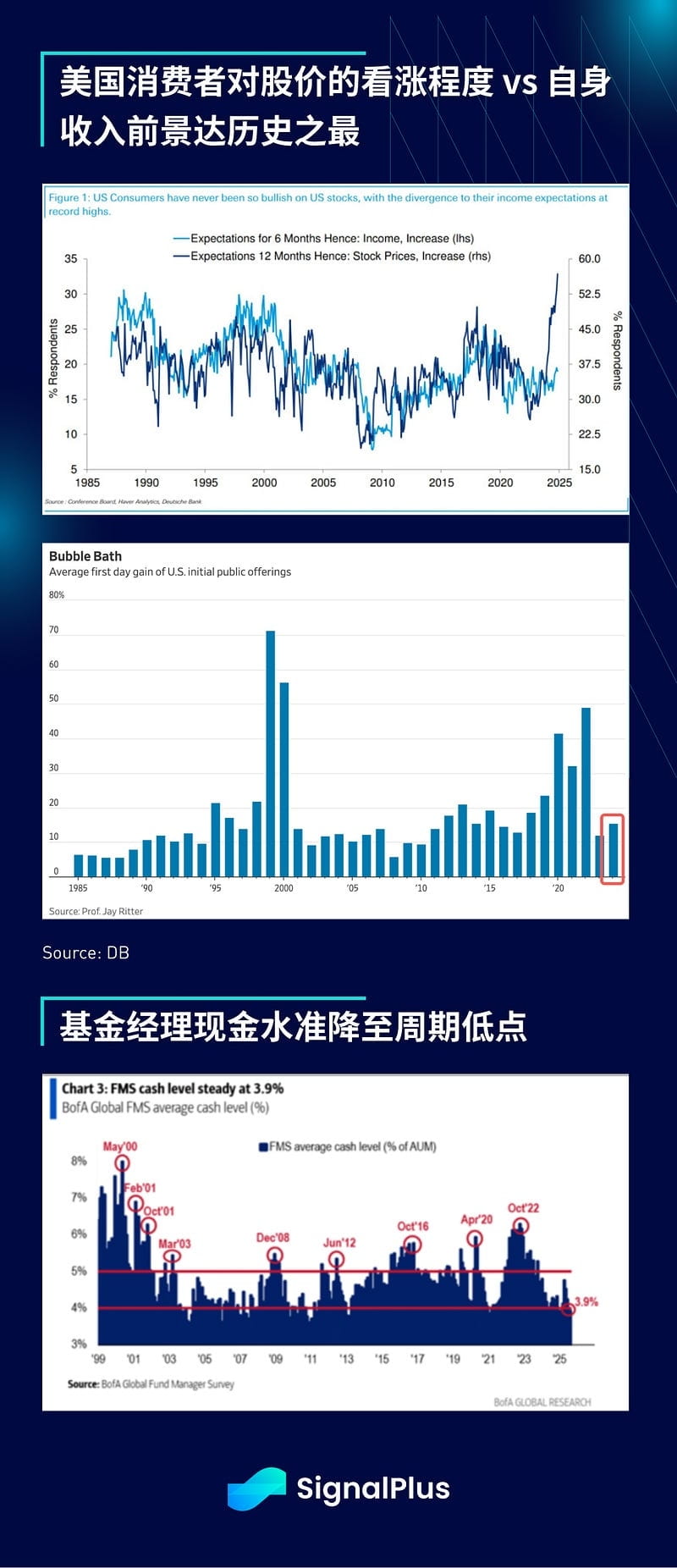

On the sentiment front, we must remind that the current level feels somewhat overly exuberant. The divergence between American consumers' optimism about stock prices and their own income prospects has reached an unprecedented historical level. Meanwhile, as we enter the historically volatile September and October months, fund managers' cash holdings have fallen to cyclical lows (indicating that investments are close to being fully deployed).

Good luck and happy trading!