Author: David Duong, Coinbase

Translation: Tim, PANews

Article Overview

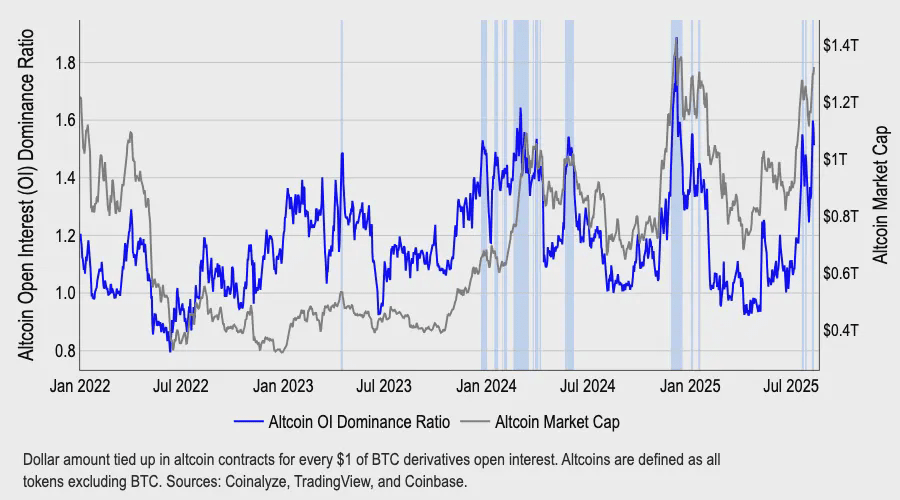

Coinbase maintains an optimistic outlook for Q3 2025, although its view on the altcoin season has changed. Based on current market conditions, it believes that as September approaches, the market may shift towards a full altcoin season. (A common definition of altcoin season is: at least 75% of the top 50 altcoins by market capitalization have outperformed Bitcoin over the past 90 days.)

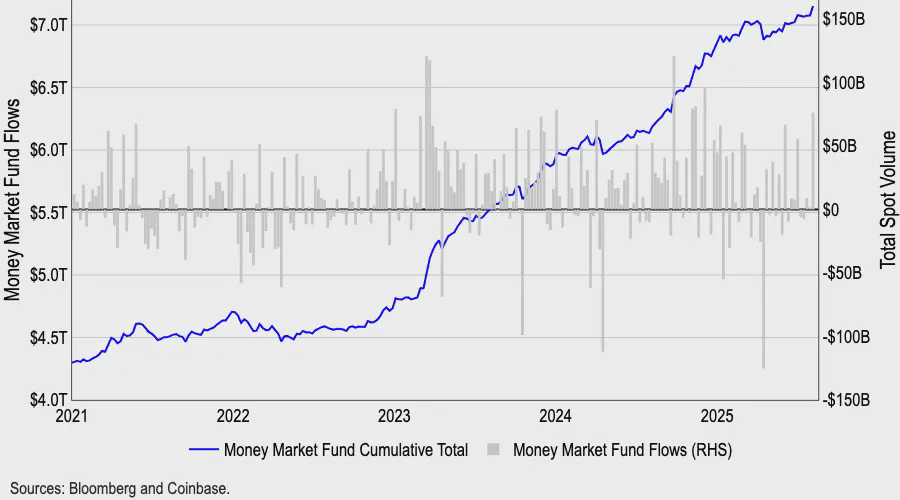

Many have been debating: if the Federal Reserve lowers interest rates in September, will it mark a cyclical peak for the cryptocurrency market? We disagree. Considering that nearly $7 trillion of retail funds are still on the sidelines, including money market funds and other areas, we believe that the Federal Reserve's policy easing may attract more retail investors into the market in the medium term.

Focus on ETH. The altcoin season index from CoinMarketCap has shown weak performance, in stark contrast to the 50% surge in total market capitalization of altcoins since early July, which reflects the growing investment enthusiasm from institutional funds for ETH. The increasing demand for digital asset treasury (DAT), coupled with the narrative of combining stablecoins with RWA, has supported this wave of market activity.

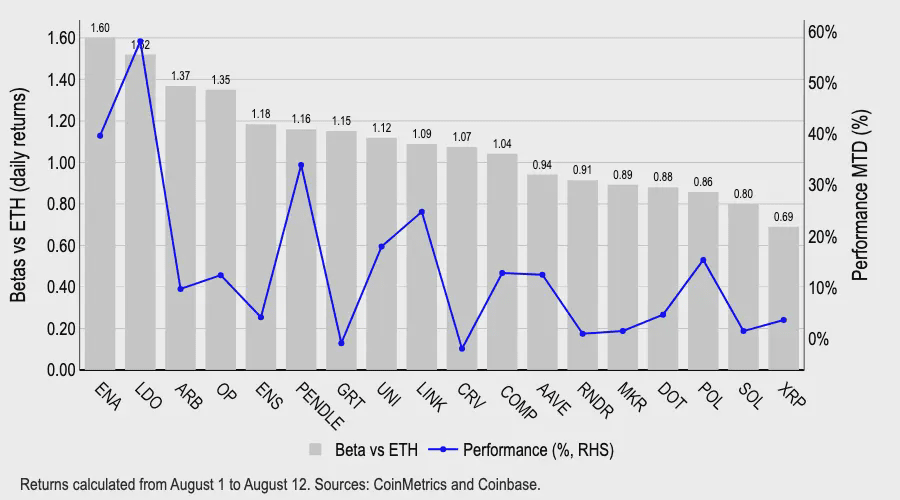

Tokens like ARB, ENA, LDO, and OP have consistently shown higher Beta returns compared to ETH, though only LDO leads with a 58% increase this month. Historically, Lido has provided a relatively direct avenue for ETH exposure through its liquidity staking features. Additionally, we believe the SEC's statement that 'under certain conditions, liquid staking tokens do not constitute securities' has supported LDO's appreciation.

Entering Altcoin Season

As of August 2025, Bitcoin's market share has declined from 65% in May to about 59%, indicating that funds are beginning to shift towards altcoins. Although the total market capitalization of altcoins has soared over 50% since early July, reaching $1.4 trillion as of August 12, the CoinMarketCap altcoin season index remains in the low 40s, far below the historical threshold of 75 that defines the start of an altcoin season. As we move into September, we believe current market conditions have shown signs that a full altcoin season is about to start.

Our optimistic outlook stems from a comprehensive observation of macro-level factors and expectations for significant regulatory progress. We have previously noted that our self-developed global M2 money supply index typically leads Bitcoin prices by 110 days, suggesting that a new wave of potential liquidity may arrive from late Q3 to early Q4 of 2025. This judgment is particularly crucial because, in the realm of institutional capital, the main investment line seems to revolve around large-cap coins. In our view, the primary force supporting the altcoin season comes from retail investors.

The current scale of U.S. money market funds has reached $7.2 trillion (the highest level on record), which is noteworthy. (See Figure 2) In April, cash reserves decreased by $150 billion, which we believe drove the strong performance of cryptocurrencies and risk assets in the following months. However, interestingly, since June, cash reserves have rebounded by over $200 billion, contrasting sharply with the upward trend in cryptocurrencies during the same period. Traditionally, the price rise of cryptocurrencies often shows an inverse relationship with the scale of cash reserves.

We believe that these unprecedented cash reserves reflect three major market concerns: (1) increased uncertainty in traditional markets (stemming from trade conflicts, among other issues); (2) overvaluation of the market; (3) ongoing concerns over economic growth. However, as the Fed approaches rate cuts in September and October, we believe the attractiveness of money market funds will begin to wane, and more capital is expected to flow into cryptocurrencies and other higher-risk asset classes.

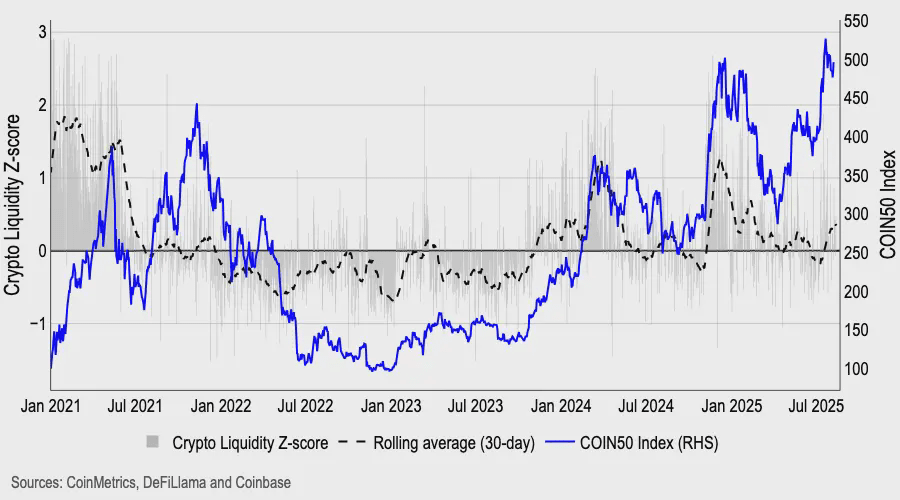

A liquidity-weighted z-score measurement model built on indicators including net issuance of stablecoins, spot and perpetual contract trading volumes, order book depth, and circulation shows that liquidity has begun to return in recent weeks, ending a six-month downward trend (see Figure 3). The growth of the stablecoin market is partly due to the increasing clarity of the regulatory framework.

Ethereum Beta Benchmark

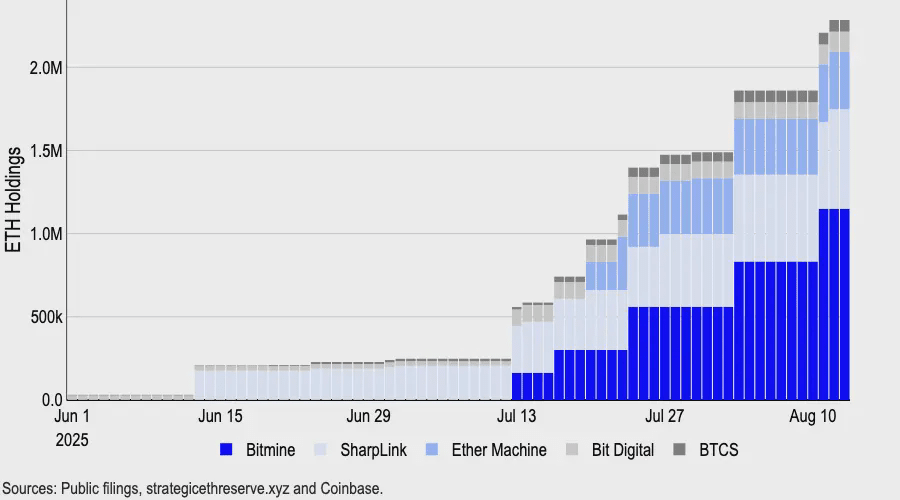

Meanwhile, the divergence between the altcoin season index and the total market capitalization of altcoins mainly reflects Ethereum's increasing institutional appeal, driven by demand from digital asset treasuries and the rise of stablecoin and RWA narratives. Just Bitmine alone has increased its holdings by 1.15 million ETH through newly raised funds totaling $20 billion, bringing its total purchasing power to $24.5 billion (whereas Sharplink Gaming, which used to hold the largest ETH position, currently holds about 598,800 ETH).

Latest data shows that as of August 13, companies holding the largest reserves of ETH collectively control about 2.95 million ETH, accounting for over 2% of Ethereum's total supply (12.07 million ETH). (See Figure 4)

In terms of higher Beta returns relative to Ethereum, tokens like ARB, ENA, LDO, and OP are at the forefront, but recently it seems only LDO has stood out in the Ethereum rally, with a monthly increase of 58%. Historically, Lido has provided investors with relatively direct exposure to Ethereum thanks to its liquidity staking features. Currently, LDO's Beta coefficient relative to ETH is 1.5 (a Beta value greater than 1.0 means the asset theoretically fluctuates more than the benchmark asset, potentially amplifying both gains and losses).

Additionally, we believe the SEC's statement regarding liquidity staking issued on August 5 supports the price increase of LDO tokens. Staff from the SEC's Division of Corporate Finance clearly stated that when the services provided by a liquid staking entity are primarily 'transaction execution' and staking rewards are directly proportioned to users through the agreement, their activities do not constitute the issuance or sale of securities. However, it's important to note that if there are guarantees of returns, self-determined re-staking, or additional return mechanisms involved, it may still trigger the classification as securities. The current guidance is merely departmental opinion; future changes in the commission's stance or judicial rulings may alter this interpretation.

Summary

Our Q3 market outlook remains positive, but our assessment of the altcoin market has changed. The recent decline in Bitcoin's dominance indicates that funds are beginning to rotate into the altcoin space, rather than fully entering an altcoin season. However, as the total market capitalization of altcoins rises, the altcoin season index is releasing early positive signals, and we believe market conditions are preparing for a rotation of capital, or a more mature altcoin market may emerge in September, with macro conditions and regulatory progress expected to provide dual support.