Author: Weimans Notes

Original link: https://mp.weixin.qq.com/s/QC0Ptu-aFv3eZ5wMZBzAyg

Statement: This article is a repost. Readers can obtain more information through the original link. If the author has any objections to the reposting format, please contact us, and we will make modifications according to the author's requirements. Reposting is only for information sharing and does not constitute any investment advice, nor does it represent the views and positions of Wu's opinion.

[Introduction] Recently, a platform called Mystonks, known for 'U.S. stock on-chain,' has sparked widespread controversy due to freezing user funds. It is understood that the platform withheld a large amount of assets on the grounds of 'non-compliance in user fund sources.' From a financial compliance perspective, this handling method is extremely unusual. A regulated financial institution, upon identifying suspicious funds, would typically refuse receipt and return the funds along the same path, while also reporting to regulatory authorities. The platform's direct 'withholding' of assets raises a significant question mark over its claimed 'compliance.' Mystonks has long promoted its possession of a U.S. MSB license and compliance in issuing STO as its core selling points. So, what is the truth behind these so-called 'compliance' qualifications? The author conducted an investigation.

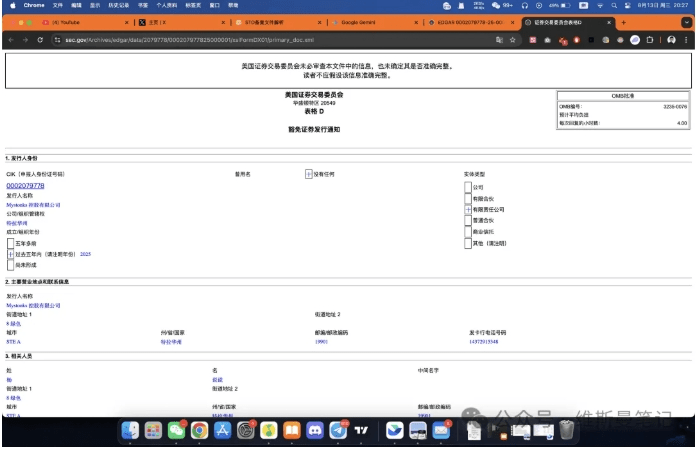

This document is precisely the crux of the issue and also the most misleading aspect of the platform's promotion. First, Form D is a notification filing, not an operating license. It only indicates that the company has informed the SEC of a private placement issuance, and the SEC does not provide any review or endorsement of the company's qualifications or the authenticity of the project. Secondly, and most importantly, this filing strictly limits the issuance targets. Regulation D is an exemption designed for private placements, aimed at a small number of qualified wealthy individuals or institutional investors (i.e., 'accredited investors'). However, Mystonks, as a publicly accessible trading platform, clearly has a majority of users who do not meet this standard. Therefore, Mystonks's actions can be understood as: taking a filing document limited to fundraising from a small number of wealthy individuals and publicly engaging in securities trading activities that require strict licensing. This approach essentially exploits ordinary investors' unfamiliarity with U.S. securities regulations to create conceptual confusion. To legally provide securities token trading services to the public, the platform needs **ATS (Alternative Trading System) or Broker-Dealer** licenses, which are fundamentally different from a simple Form D filing. After discussing the relatively complex STO, let's look at the more common promotional tool — the U.S. MSB license. Regarding the MSB license, investors need to recognize one core fact: its value and significance have been severely exaggerated by many projects in the market. The regulatory body for MSB (Money Services Business) is FinCEN, which is under the U.S. Department of the Treasury, and its core responsibility is anti-money laundering (AML). In other words, FinCEN only cares whether the platform reports suspicious transactions as required to combat financial crimes, but it is not responsible for ensuring the safety of user funds, reviewing the platform's business model, or technological capabilities. Moreover, the application threshold for MSB is extremely low; registration can be easily completed through intermediaries overseas, even without establishing a physical office in the U.S. This makes it a preferred tool for many projects to quickly and cheaply 'package' their compliance image. When a platform primarily serving non-U.S. users repeatedly emphasizes its MSB license, investors need to understand that this is more of a marketing strategy than proof of its strong financial capabilities.

After discussing the relatively complex STO, let's look at the more common promotional tool — the U.S. MSB license. Regarding the MSB license, investors need to recognize one core fact: its value and significance have been severely exaggerated by many projects in the market. The regulatory body for MSB (Money Services Business) is FinCEN, which is under the U.S. Department of the Treasury, and its core responsibility is anti-money laundering (AML). In other words, FinCEN only cares whether the platform reports suspicious transactions as required to combat financial crimes, but it is not responsible for ensuring the safety of user funds, reviewing the platform's business model, or technological capabilities. Moreover, the application threshold for MSB is extremely low; registration can be easily completed through intermediaries overseas, even without establishing a physical office in the U.S. This makes it a preferred tool for many projects to quickly and cheaply 'package' their compliance image. When a platform primarily serving non-U.S. users repeatedly emphasizes its MSB license, investors need to understand that this is more of a marketing strategy than proof of its strong financial capabilities.

Conclusion: Understanding a Type of Platform's 'Compliance' Tricks from Mystonks. The Mystonks case is not an isolated incident; it clearly reveals a type of platform's common 'compliance' packaging tactics in gray areas. Looking at the market, many exchanges and financial platforms are reusing similar scripts, and investors need to establish a clear understanding of this. The typical tricks of such platforms can be summarized as: 1. Step one: Use the MSB license as a marketing 'doorstone.' Utilizing its 'U.S. official' background and extremely low acquisition cost, quickly establish a basic, seemingly reliable image. 2. Step two: Interpret securities filings using 'concept switching.' Package a limited, strictly conditional filing document (such as a private placement filing) as a comprehensive operating license that can provide services to the public, and use information asymmetry for deep misguidance. 3. Step three: Use geographical and legal differences for 'targeted marketing.' They know that their business cannot land in the U.S., so they focus on overseas users who are unfamiliar with U.S. regulations, forming a situation where 'flowers bloom inside the wall while the fragrance wafts outside.' As investors, we should learn lessons from these tricks. When judging whether a platform is truly compliant, please remember two basic principles: ● True compliance is expensive and tangible. It means high licensing application fees, deposits, rent for physical offices, and expenses for local legal teams. Those easily obtained, invisible 'compliance' must be cheap in value. ● True compliance is transparent and specific. It dares to clearly publicize its license types, numbers, regulatory scope, and restriction clauses. Any vague, broad 'compliance' rhetoric often cannot stand up to scrutiny. In investment decisions, please restore the term 'compliance' from a marketing phrase to a legal fact that needs to be strictly examined. Upholding this bottom line is the best way to protect our asset safety.

Starting from Mystonks: Unveiling the 'U.S. Compliance' Promotional Trap of Crypto Platforms

--

Disclaimer: Includes third-party opinions. No financial advice. May include sponsored content. See T&Cs.

Explore the latest crypto news

⚡️ Be a part of the latests discussions in crypto

💬 Interact with your favorite creators

👍 Enjoy content that interests you

Email / Phone number

Relevant Creator

@Square-Creator-45ff24533