Author: Liu Ye Jing Hong

Original link: https://mp.weixin.qq.com/s/y5WED5zyPPRB-WPS2QOKkg

Statement: This article is a reprint. Readers can obtain more information through the original link. If the author has any objections to the form of reprinting, please contact us, and we will make modifications according to the author's requirements. Reprinting is only for information sharing and does not constitute any investment advice, nor does it represent Wu Shuo's views and positions.

Introduction

Recently, I have been deeply involved in several real-world asset (RWA) tokenization projects and have conducted in-depth research on related businesses in practice. To facilitate readers' understanding, this article will share some of our core observations and thoughts in a Q&A (FAQ) format.

Q1: Why has RWA become popular recently?

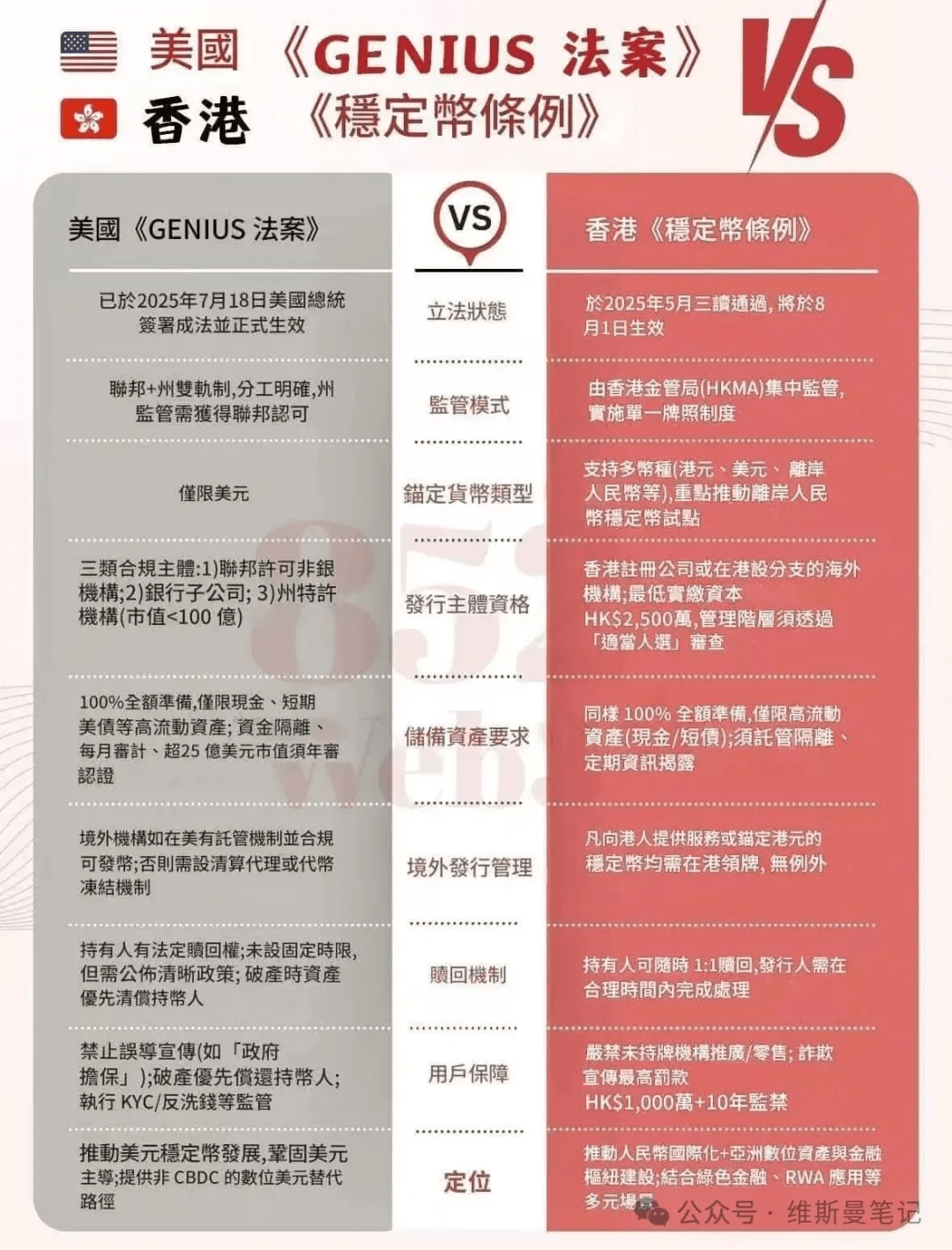

The fundamental reason for the popularity of RWA is the formal implementation of the Hong Kong Stablecoin Regulation on August 1, 2025. This marks the achievement of full compliance for stablecoins as anchor currencies for transaction settlement. Against the backdrop of the Hong Kong government's strong support for the compliant issuance of virtual assets, a market framework for virtual assets that is compliant and legally sound has taken shape.

From a market motivation perspective, many enterprises hope that Hong Kong RWA can open up a new compliant financing channel, and some listed companies also hope to boost market confidence and stock prices by laying out in this track. This expectation is somewhat similar to certain market sentiments during the early ICO boom.

Q2: What is the difference between Hong Kong RWA and Web3 RWA?

The difference is significant; the two have no direct business correlation.

The core of Hong Kong RWA is 'full-chain compliance.' The underlying assets must meet the legal requirements of both regions, that is, compliance with the laws of the asset's location (e.g., Mainland China) and compliance with local laws in Hong Kong. This compliance requirement cannot be satisfied simply by technical means such as 'consensus chain verification'; it must be based on documents with clear legal validity. For example, data assets need to complete compliance exit filings, while physical assets need to handle compliant exit transfer procedures.

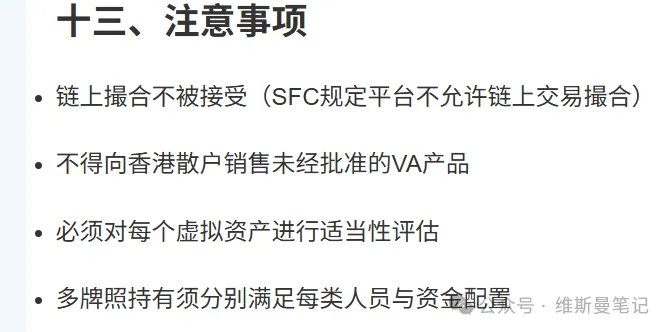

There is a common misconception in the market, such as the idea of issuing RWA in Hong Kong after verifying the ownership of Mainland real estate on-chain. However, under the current framework, this path is completely unfeasible. First, the Hong Kong Securities and Futures Commission (SFC) explicitly prohibits automated matching transactions on-chain; secondly, transferring the complete ownership of Mainland real estate to Hong Kong faces significant legal and practical obstacles.

Currently, the forms of RWA officially encouraged by the Hong Kong Monetary Authority (HKMA) mainly focus on stablecoins and tokenized bonds (such as government-issued green bonds). The operational model for a broader range of physical RWA is still unclear, but it is certain that regulatory authorities do not accept models based solely on blockchain verification for issuance; assets must be fully placed under Hong Kong's regulatory system.

Therefore, Hong Kong RWA emphasizes its nature as a 'regulated distributed ledger' in the application of blockchain technology, rather than the global free trade and circulation pursued by Web3 RWA.

Q3: How can we understand Hong Kong RWA in simple terms?

At the current stage, Hong Kong RWA can be understood as a 'futures market that allows for compliant private issuance.'

Just as crude oil futures require designated storage locations to hold and deliver physical crude oil, Hong Kong RWA also requires that its underlying assets must be in a state that can be effectively regulated by Hong Kong financial regulatory authorities. If the underlying physical assets of an RWA cannot be regulated, it is highly unlikely to be approved for issuance. For example, tokenizing rental income from real estate outside Hong Kong is unlikely to be approved since both the property itself and the leasing contract cannot be directly regulated by Hong Kong.

In contrast, some intangible assets, such as entertainment copyrights, have a higher likelihood of approval. As long as these assets have clear ownership under Mainland law, are compliant, and can legally transfer their rights to a regulatory entity in Hong Kong, their future revenues might be used to issue RWA.

It is worth noting that the Hong Kong government currently does not require the underlying assets of RWA to be located within Hong Kong; the core requirement is that the assets can 'be regulated by the Hong Kong government.' Based on this, I predict that even if a quality asset is not in Hong Kong, it may still have the possibility of approval for issuance if it can provide a complete set of credible evidence meeting Hong Kong regulatory requirements (for example, a continuous audit report issued by one of the 'Big Four' accounting firms).

Q4: Can RWA be traded after issuance?

No. Issuing RWA and trading RWA are completely independent matters.

Issuing RWA is more akin to a fundraising activity. Once the issuance application is approved, the issuer can raise funds from 'qualified investors' (Professional Investors). However, this does not mean that the tokens can be publicly traded.

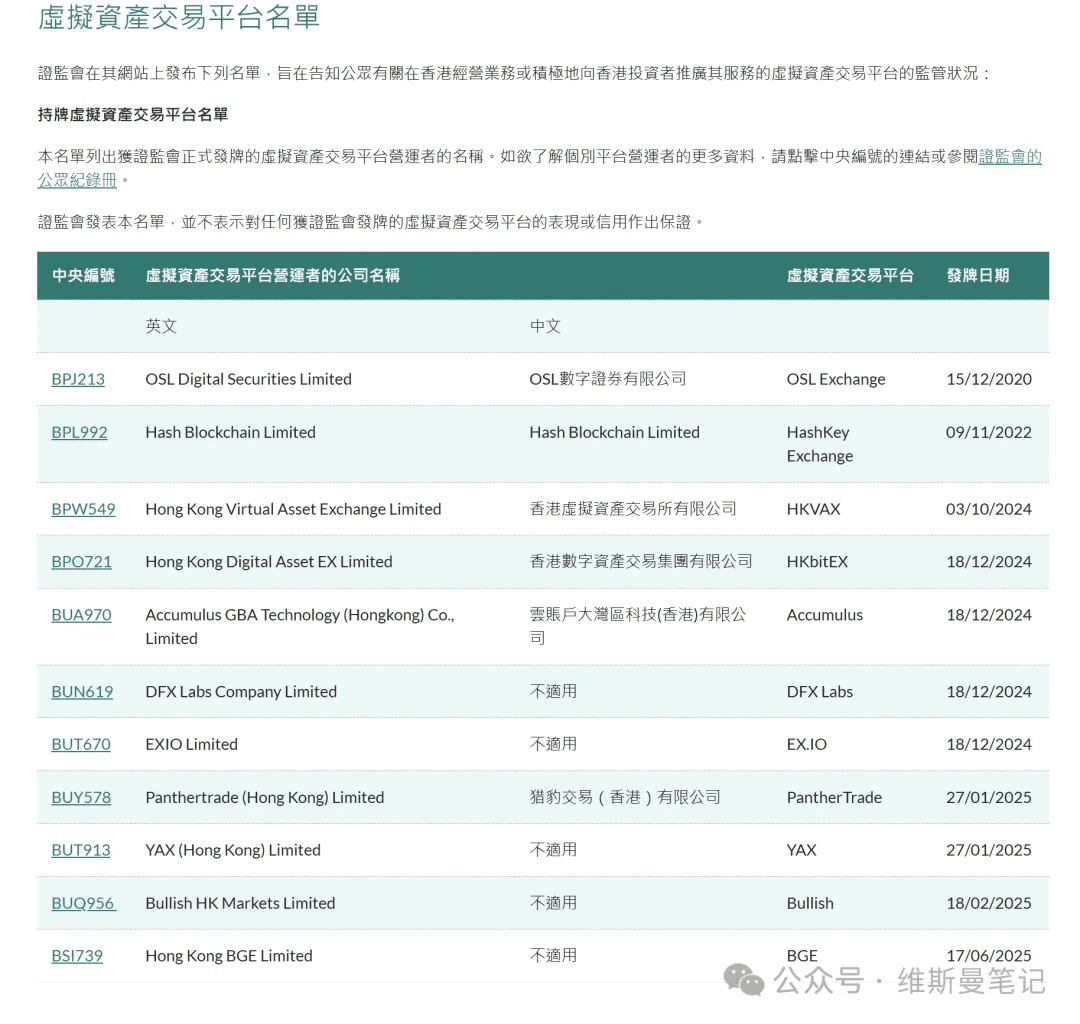

To achieve trading, according to the regulatory boundaries defined by the Hong Kong Securities and Futures Commission (SFC), RWA tokens are strictly prohibited from engaging in automated matching transactions on-chain. The only path is to apply for listing on a licensed virtual asset trading platform (VASP) in Hong Kong.

Moreover, these compliant virtual asset trading platforms are only open to qualified investors, which basically rules out the possibility of attracting a large number of retail investors through community marketing hype, differing significantly from the operational models of certain crypto assets (such as meme coins). Additionally, listing and trading on compliant platforms is expected to incur significant costs.

Q5: What about the issuance of compliant stablecoins in Hong Kong?

Among all RWA categories, the feasibility of issuing compliant stablecoins is the highest, especially stablecoins issued based on quality assets such as Hong Kong dollars, offshore renminbi, US dollars, or high-credit-grade bonds.

Of course, the threshold is also very high. Without discussing the complex compliance processes, just the capital cost poses a significant entry barrier for most startups. According to the Stablecoin Regulation, the issuing entity must actually pay at least 25 million Hong Kong dollars in paid-up capital and accept centralized supervision from the Monetary Authority. In addition, the issued stablecoins must have 100% quality liquid assets as reserve support.

Q6: Can alliance chain technology be used to issue Hong Kong RWA?

This is a common major misconception recently. The application scenarios of domestic alliance chains (such as verification and traceability) are largely unrelated to the compliance requirements of Hong Kong RWA, yet some business leaders we have encountered often confuse the two.

The legal validity of Hong Kong RWA projects completely relies on the clarity of ownership and the authenticity of the underlying asset's value. According to analyses by Hong Kong legal experts, issuers must fulfill strict verification obligations, including:

Legal document verification: Confirming that the asset is free of any rights encumbrances through property registration documents, judicial declarations, etc.

Financial penetration audit: Commissioning licensed auditing institutions to verify the asset's cash flows, liabilities, etc., to prevent financial fraud.

Independent third-party valuation: For non-standard assets, independent evaluation institutions need to use multiple models for valuation endorsement.

In short, Hong Kong RWA projects only recognize documents with legal validity and the review results of licensed third-party institutions, completely rejecting the technical concept of 'on-chain verification' as a basis for legal validity.

Q7: What is the use of issuing RWA in Hong Kong?

In my opinion, for legitimate enterprises, its core functions are mainly twofold: first, to expand new compliant financing channels for quality assets; second, for listed companies, it can serve as a positive signal to boost market confidence.

However, it is crucial to be aware that there are numerous participants in the current market treating RWA as a speculative narrative. Their true purpose may not be to complete compliant issuances but to use this trending concept for private financing or market speculation. Such phenomena are not uncommon in the industry and warrant high vigilance from investors and practitioners.

Conclusion

In summary, Hong Kong RWA is a very new field, with successful cases being few and far between. Therefore, the viewpoints in this article may still have limitations, and I will continue to update my understanding as I deepen my knowledge of the business. This article serves merely as a personal record of insights at this current juncture, hoping to provide some valuable references for colleagues interested in this field.

In-depth Analysis of Hong Kong RWA: FAQ from the Frontline

--

Disclaimer: Includes third-party opinions. No financial advice. May include sponsored content. See T&Cs.

Explore the latest crypto news

⚡️ Be a part of the latests discussions in crypto

💬 Interact with your favorite creators

👍 Enjoy content that interests you

Email / Phone number

Relevant Creator

@Square-Creator-45ff24533

Explore More From Creator

--