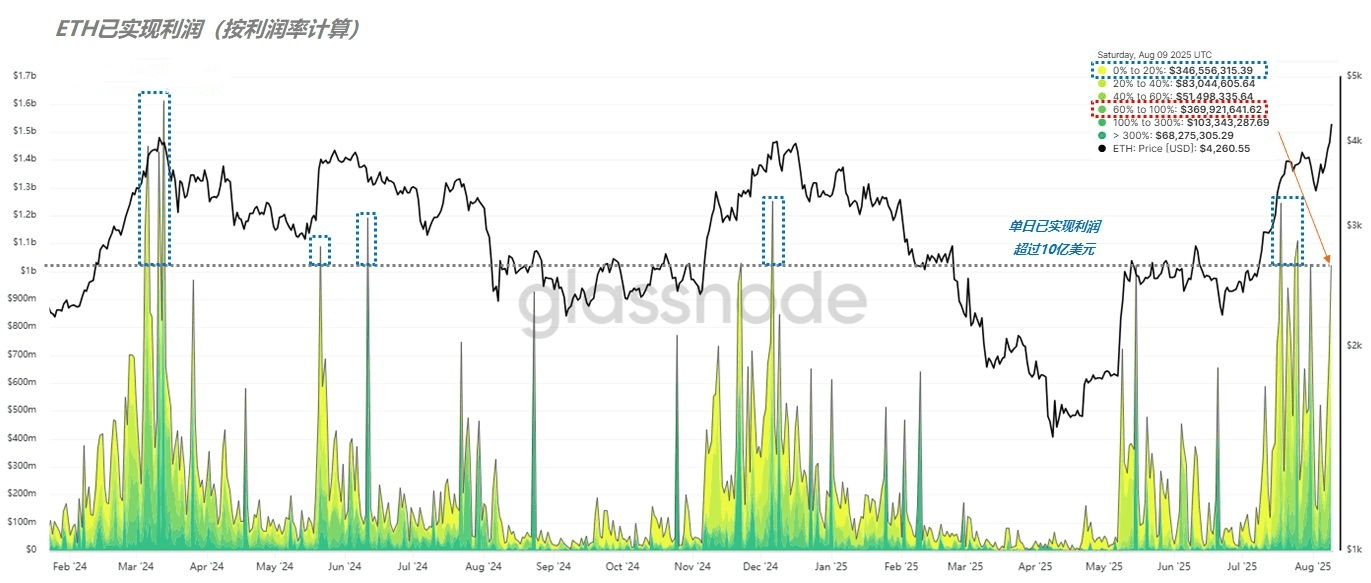

During yesterday's surge of Ethereum to $4,200, on-chain data recorded about $1 billion in realized profits. This scale has been extremely rare in the past six months; since February 2024, there have only been 8 trading days where realized profits exceeded this level.

This indicates two points:

First, the market has a strong absorption capacity for the current selling pressure of ETH; second, the battle between bulls and bears is becoming more short-term. If the absorption is insufficient, the price may correct; if demand is strong, there is hope for continued upward movement.

From the sources of realized profits, they can be mainly divided into two categories:

Profit margin below 20%: Mainly dominated by short-term speculative funds, usually appearing frequently during rapid price increases, with limited reference value.

Profit margin between 60%-100%: This is a key focus area, with an average profit of 80%, the cost of building positions is approximately between $2,300-$2,500.

(Figure 1)

These chips were likely accumulated during the sideways trading phase of ETH from May to July this year, with profits realized when the price broke through $4,000. It is worth noting that there are still about 2.6 million ETH in the $2,500 cost range and about 2.9 million ETH in the $2,700 range. The selling intentions of these holders and the market absorption capacity will directly affect the subsequent trend.

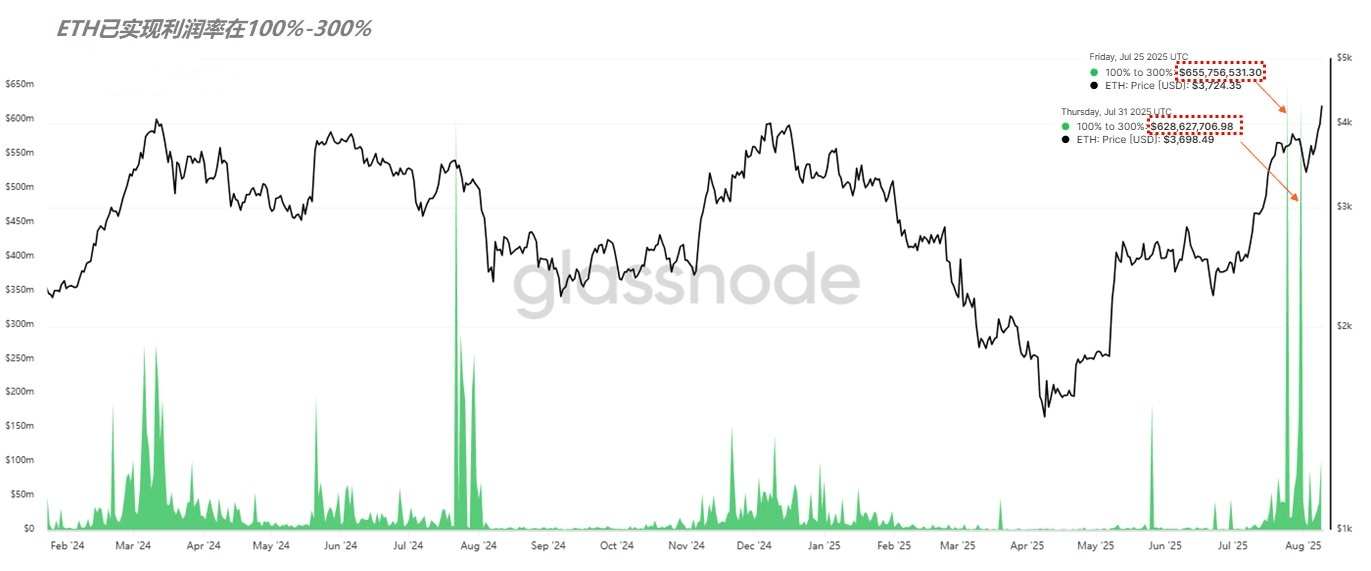

(Figure 2)

As for the earlier chips with higher profit margins, the selling volume yesterday was not significant. The reason is that this portion of funds had already realized profits on July 25 and July 31, with profit margins of 100%-300% resulting in profits of $620 million and $650 million, respectively. The transaction prices were mostly around $3,700, and the average cost was about $1,200, belonging to long-term holding funds.