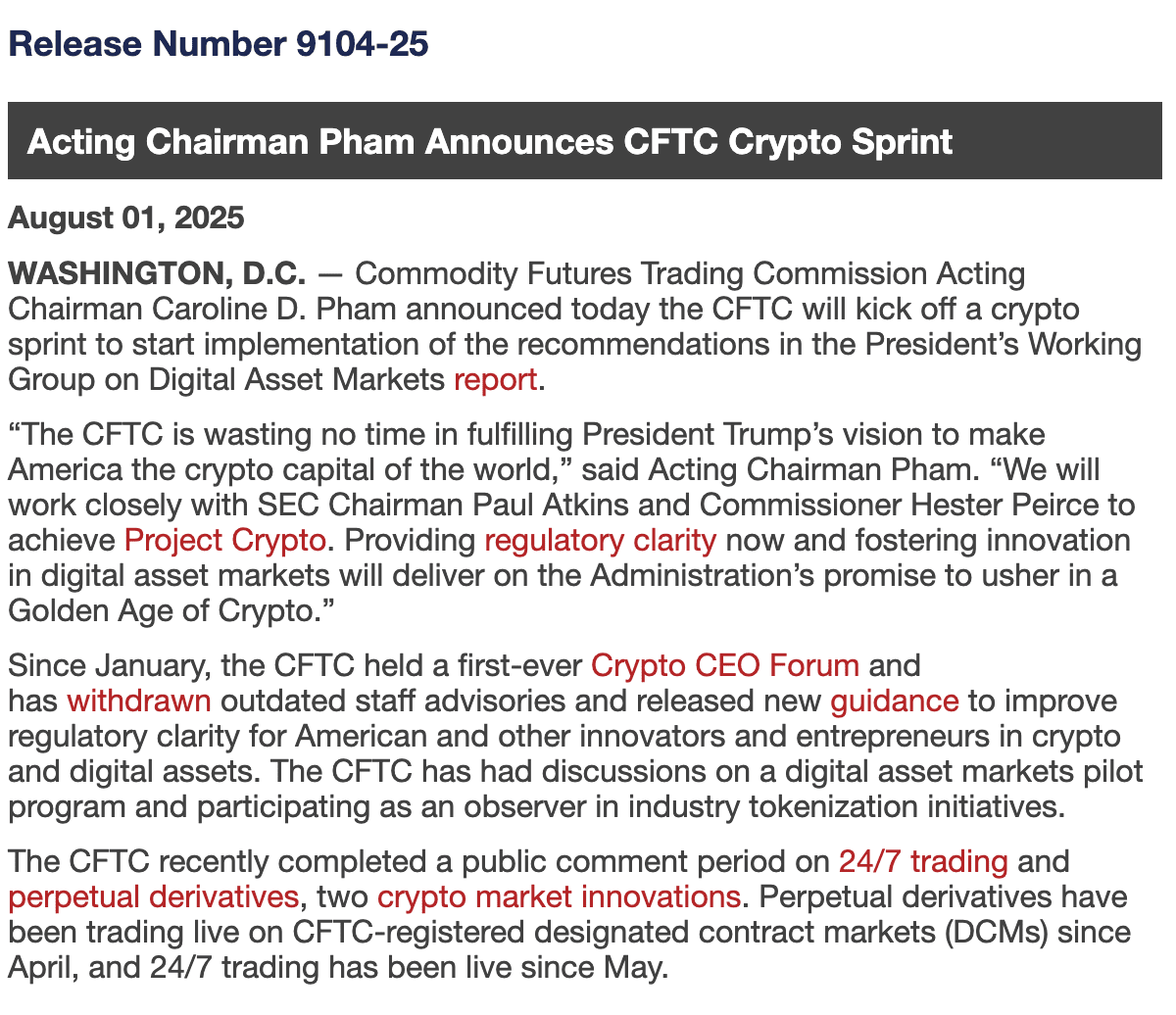

Under the strong push from the Trump administration, the United States is accelerating the integration of crypto assets into the mainstream financial system. On August 1, the U.S. Commodity Futures Trading Commission (CFTC) officially launched a regulatory program called 'Crypto Sprint,' and subsequently proposed on August 5 to include spot crypto assets for compliant trading on CFTC-registered futures exchanges (DCM). This move not only breaks the long-standing regulatory gray area of the spot market but also signifies that the Web3 industry will welcome a clear and feasible compliance path.

CFTC acting chair Caroline Pham publicly stated: 'Under President Trump's strong leadership, the CFTC is fully promoting federal-level digital asset spot trading and coordinating with the SEC's Project Crypto.' This statement sends a strong signal: U.S. regulation is shifting from 'defensive suppression' to 'institutional acceptance,' providing unprecedented compliance opportunities for DeFi, stablecoins, on-chain derivatives, and other Web3 infrastructure.

Legalization of spot contracts: The starting point for the institutionalization of the crypto market

For a long time, the U.S. regulatory system has lacked unified management of crypto spot trading. Transactions of crypto assets such as BTC and ETH are mostly concentrated on overseas platforms or unlicensed domestic exchanges, and the lack of regulation not only makes it difficult to protect investors' rights but also keeps a large amount of institutional capital in a wait-and-see state.

The 'Crypto Sprint' launched by the CFTC addresses this pain point. One of its core contents is to promote the legal listing of non-securities crypto asset spot contracts on CFTC-registered futures exchanges (DCM). By approving these platforms to host spot crypto trading, the CFTC provides the market with a compliant alternative path, replacing the long-reliance on unlicensed or offshore trading platforms—these platforms have gradually lost institutional trust in light of the FTX collapse (2021) and the ongoing regulatory issues surrounding Binance. Therefore, this policy means a more legitimate, transparent, and fair entry path for institutional investors into crypto assets, clearing obstacles for large-scale allocation of digital assets.

According to the CFTC, Section 2(c)(2)(D) of the Commodity Exchange Act explicitly requires that any commodity trading involving leverage, margin, or financing must be conducted on a registered DCM. This provision provides a solid legal basis for the legitimate listing of crypto spot contracts and brings much-needed regulatory certainty to the market. Under this framework, we may see centralized trading platforms akin to Coinbase or on-chain derivatives protocols such as dYdX obtaining compliance operating licenses through registered DCMs.

At the same time, this policy also opens a compliant channel to crypto assets for traditional financial institutions. The Chicago Mercantile Exchange (CME), representing DCM, has long possessed a complete infrastructure for BTC and ETH futures markets. Once spot contracts are approved for listing, it will provide institutional investors with a one-stop crypto asset trading entry from futures to spot, accelerating the pace of traditional capital entering the market.

SEC and CFTC join forces: Regulatory coordination brings certainty

One of the biggest regulatory challenges in the U.S. crypto market in recent years has been the overlapping responsibilities and ambiguous definitions between the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC). Project teams often have to cope with compliance pressures from the SEC while also adhering to the CFTC's commodity trading rules, falling into the dilemma of 'regulatory squeeze' or 'double enforcement,' consuming resources and increasing uncertainty.

The 'Crypto Sprint' clearly sends a signal for the first time: the CFTC will establish a close cooperation mechanism with the SEC to collaboratively clarify the legal attributes of crypto assets (securities or commodities), custody standards, and trading compliance requirements, thus providing market participants with a unified and predictable compliance path.

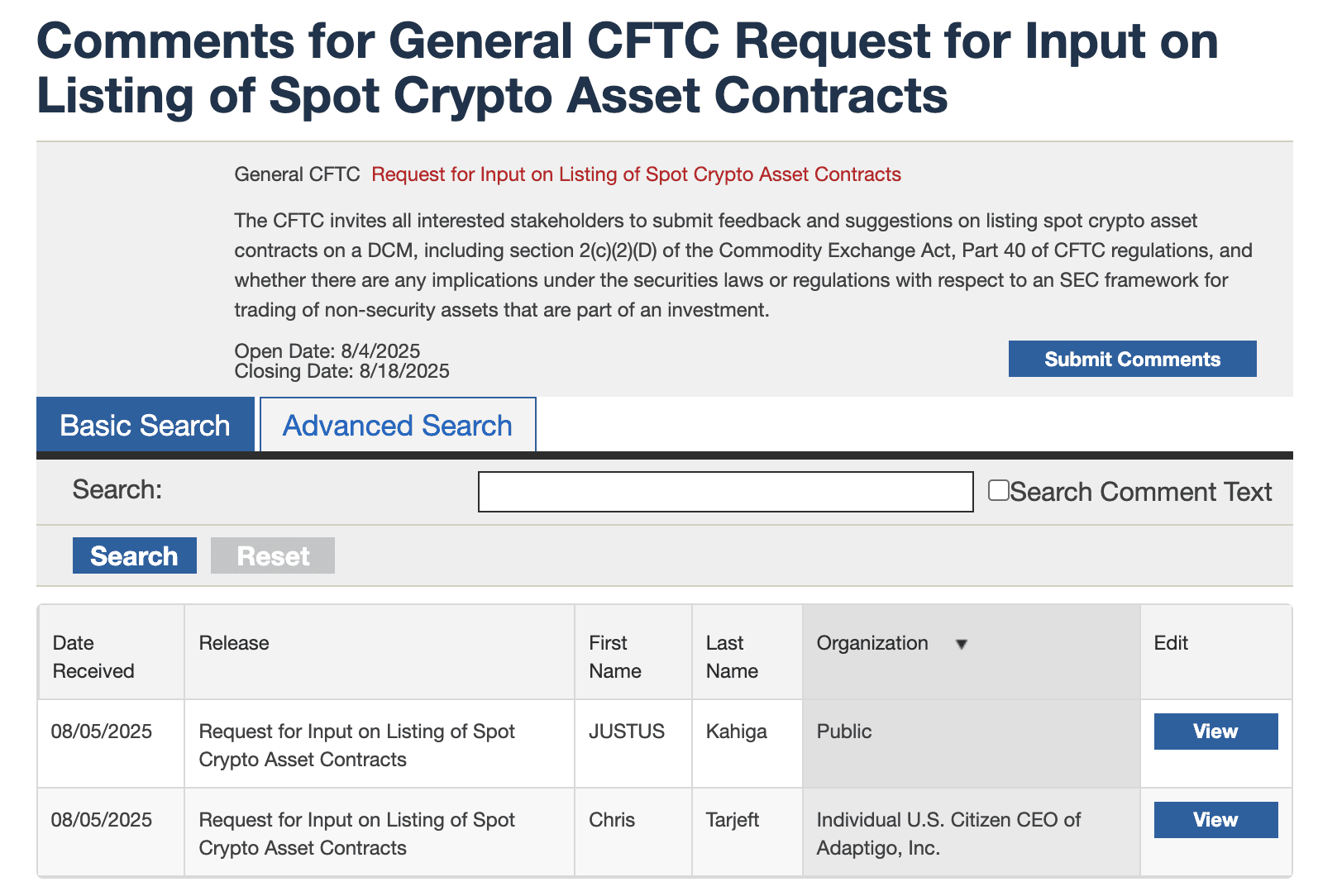

'Sprint' not only symbolizes an acceleration of regulatory pace but also marks a shift in regulatory thinking—from passive defense to active collaboration. For Web3 project teams, this is no longer merely a 'regulatory observation period' but an unprecedented window for institutional co-construction. The CFTC has publicly solicited market feedback on the 'listing of spot crypto asset contracts on registered exchanges (DCM)' plan, with a deadline of August 18. If participants can submit their opinions in a timely manner, they may not only avoid future regulatory blind spots but also potentially influence the specific direction of the rules.

Meanwhile, the SEC's 'Project Crypto' is highly coordinated with the 'Crypto Sprint,' attempting to create a unified federal regulatory framework that clarifies the boundaries between securities-type and commodity-type crypto assets, and promotes the construction of a 'super app' structure that can trade multiple asset types simultaneously. If this idea is realized, future trading platforms will be able to legally offer 'one-stop' crypto financial services such as stocks, Bitcoin, stablecoins, and staking services under a single license.

Related reading: (What Trump wants to stir up from SEC's Project Crypto)

SEC Chair Paul Atkins and Commissioner Hester Peirce have also publicly expressed their support, calling it a 'historic turning point for promoting on-chain integration of the financial system' and stating that they will accelerate the formulation of specific rules in key areas such as stablecoin regulation, crypto asset custody, and compliant token issuance.

This dual-track regulatory approach is expected to end the long-standing confusion in the U.S. regarding whether crypto assets are 'securities or commodities,' setting a clear and replicable compliance model for the world.

More importantly, this means that Web3 projects can finally stop 'stepping on landmines' and instead truly integrate into the mainstream financial system through a clear registration process, compliant custody, and auditing systems, achieving a connection between on-chain assets and real-world finance.

Summary

In the past week, the U.S. government has released unprecedented strong signals in the field of crypto assets: the White House officially issued the Digital Asset Strategic Report, the SEC launched Project Crypto, the CFTC initiated 'Crypto Sprint', and publicly solicited opinions to promote the compliant listing of spot contracts; at the same time, the White House made a rare statement banning banks from discriminating against crypto companies—this is not just a 'softening' but a complete policy shift.

Once upon a time, the SEC was the biggest regulatory shadow over crypto projects, but now we see it teaming up with the CFTC to establish a unified regulatory framework for Web3. The visible change is a historic structural shift: from ambiguity to clarity, from repression to support, from gray areas to federal legislation.

This time, the sprint is not just for regulatory agencies—but for every Crypto Builder.