Suddenly, what seems to attract the most attention in the US stock market is no longer AI, but a bunch of companies on the verge of delisting. In recent months, the US capital market has seen an unprecedented scale of reverse mergers occurring at increasingly larger amounts.

Listed companies have completely abandoned their original main businesses, turning cryptocurrencies into their fundamentals, with stock prices skyrocketing several times or even dozens of times in a short period. Now, the US stock market has become a playground for crypto circles to conduct financial experiments. This time, crypto VCs have really brought the story to Wall Street's ears.

In the US stock market, 'firestarter' is launching DAT fireworks.

Three months ago, when investing in Sharplink, Primitive Ventures did not expect this new crypto track in the US stock market would become so crowded in such a short time. 'At that time, not many were discussing these investment cases; the market's current heat is simply incomparable, but it really was just a matter of one or two months,' said Primitive partner Yetta.

In June of this year, Sharplink Gaming announced the completion of $425 million in financing, becoming the first Ethereum reserve company in the US stock market. Following the announcement, the company's stock price surged, at one point rising over 10 times. Primitive, as the only fund in the Chinese community participating in this investment case, garnered attention within the circle.

'Because we found that the liquidity in the crypto market is not good, but the purchasing power on the institutional side is extremely strong. Bitcoin ETF volume has always been good, and the open interest for Bitcoin options on CME even exceeds that of Binance.' Last April, Primitive held an internal meeting for a major review, and thereafter set a new investment direction of 'integration of CeFi (centralized finance) and DeFi (decentralized finance).' Now, they have become one of the busiest VCs in the crypto circle.

Today, Primitive receives daily emails from investment banks inviting the fund to participate in investments in crypto reserve companies. In this wave of investment, investment banks act as intermediaries, responsible for helping project parties find and coordinate all investors and assisting teams in roadshows for the funders.

In the past month, Primitive has discussed no less than 20 crypto reserve projects. However, currently, the only projects they have publicly invested in are Sharplink and another company doing Litecoin reserves, MEI Pharma. This cautious investment approach stems from concerns about an overheated market, and since May of this year, the team has begun closely monitoring various top signals.

'We do feel that the level of market bubble is significantly higher now than a few months ago,' Yetta told Beating. The team now prepares daily market reports and assesses appropriate exit strategies based on the situation. 'Crypto reserve companies are financial innovations; you can maintain a bullish outlook on their underlying assets in the long term, but there are also risks of severe deleveraging and bubble bursts when the market declines.'

Unlike Primitive, Pantera is gearing up for a major push. This 12-year-old veteran crypto VC even coined a new term for this field—DAT (Digital Asset Treasury). In early July, Pantera established a new fund named the DAT Fund.

In the fundraising memorandum, Pantera partner Cosmo Jiang wrote: 'As an investor, it is very rare to find oneself at the starting point of a new type of investment category. Recognizing this and responding quickly to seize early investment opportunities is crucial.'

The story Pantera tells investors is very simple: if a company holds an increasing amount of Bitcoin per share each year, then owning its stock will mean you are acquiring more and more Bitcoin.

The underlying logic of Bitcoin reserve companies led by MicroStrategy and other cryptocurrency reserve companies is to raise capital in the market through targeted issuance, convertible bonds, preferred shares, etc., when there is a premium on the value of crypto assets over their market capitalization, and to purchase more crypto assets. Because stocks exist at a premium, companies can hoard more assets at a lower cost.

Investors typically use the mNav indicator (Market Cap To Net Asset Value) to measure its premium multiple to assess a company's fundraising ability. 'The stock market is obviously volatile; sometimes the market overestimates certain assets. At this time, launching financial instruments for fundraising is essentially selling this volatility, so from this perspective, the premium can actually be maintained in the long term,' Cosmo told Beating.

In April of this year, Pantera invested in the reserve Solana public chain token SOL's Defi Development Corps (DFDV), which is the first company in the US stock market to use cryptocurrencies other than Bitcoin as reserve assets, with its stock price having risen over 20 times in the past six months.

However, for Pantera, this was definitely a contrarian investment, as no one was willing to invest in the project at the outset, and the company's $24 million financing came almost entirely from Pantera.

Most members of DFDV come from the senior management of Kraken, and the CFO has also operated Solana validation nodes. The team's deep understanding of Solana and their professionalism in traditional finance became key factors in impressing Pantera. 'Nevertheless, we still set some downside protection measures in the transaction structure, but DFDV's astonishing success was something we completely did not anticipate.'

'I believe the real catalyst was Coinbase being included in the S&P 500 index, which forced all fund managers worldwide to consider crypto,' said Nachi. Since Trump's election, the crypto industry has been booming in traditional capital markets, with Circle's IPO attracting global attention to stablecoins, and Robinhood's foray into RWA has pushed security tokenization to the forefront. Now, DAT is becoming the new concept of the relay.

Less than a month after investing in DFDV, Cantor Equity Partners also came calling. The success of DFDV accelerated SoftBank's and Tether's Bitcoin reserve company plans, ultimately raising about $300 million in external funding for CEP, with Pantera again becoming its largest external investor.

The funding for investing in DFDV and CEP came from Pantera's flagship venture capital fund (Venture Fund) and liquidity token fund (Liquid Token Fund). The team initially thought these would be the only two investments the fund would make in this field.

But the market's development quickly surpassed Pantera's expectations. Due to the limitations in the investment portfolio framework and concentration of the aforementioned two funds, Pantera soon made the decision to establish a new fund.

On July 1, the DAT Fund began fundraising with a target of $100 million. On July 7, it was officially announced that the fundraising was completed. Due to the high enthusiasm from LPs, Pantera subsequently launched a second fundraising for the DAT Fund. By the middle of the month, when interviewed by Beating, the funds from the first DAT Fund had already been fully deployed.

In publicly disclosed investment cases, Pantera often plays the role of 'Anchor,' being the largest investor. Due to the initial poor liquidity of the DAT company, it is prone to discounts. At this time, the team needs to bring in heavyweight investors off-market to build a foundational base, ensuring liquidity and narrowing price spreads.

On the other hand, the 'Anchor Investor' itself is also a strategy for Pantera to market; 'In the past two months, we have received nearly a hundred proposals from DAT companies. Pantera is usually the first call they make because we entered early enough to establish cognitive leadership in this field, and they also see that when we invest, we are real investors who can place heavy bets and dare to write big checks.'

Of course, Pantera does not invest in just anything. For DAT companies, the fund also values their ability to create 'cognitive leadership' in market marketing. Their investments in Sharplink and Bitmine are largely based on this consideration. Among them, Bitmine was the first investment of the DAT Fund, with Pantera also playing the role of 'Anchor' in the transaction.

On June 2, key figures in the Ethereum community, led by Joseph Lubin, completed the reverse acquisition of Sharplink, marking the birth of the first Ethereum reserve company. On June 12, Joseph and other Ethereum core members released a fundamental report on Ethereum through Etherealize, introducing its investment value to institutions.

On June 30, the second Ethereum reserve company, Bitmine, was born, with 'Wall Street cryptocurrency expert' Thomas Lee coming to the fore and frequently appearing in mainstream media to interpret investment opportunities in Ethereum. At the same time, Sharplink's stock price began to rise, and the 'Ethereum arms race' quickly became the hottest topic in the industry.

'To truly open up the channel for financial leverage, the market capitalization of the DAT company must reach at least $1 to $2 billion,' Cosmo told Beating. Only by reaching this scale can the company truly achieve valuation premium in the market and open another door to institutional capital through convertible bonds or preferred shares.

But before that, the DAT company needed to tell the story to ordinary investors, not just crypto-native investors, but a broader mainstream retail group in the stock market. 'We need to make them understand this story and be willing to participate. The market must first 'believe it will happen' for the whole model to work.'

Establishing continuous trust with the market is another key factor in the success of the DAT company. The traditional financial market requires 'transparency + discipline' guarantees; the team must be adequately 'Crypto Native' while also possessing the sensitivity of traditional finance, managing and disclosing information for listed companies, and clearly understanding the SEC's rules and processes to ensure the company can efficiently and professionally access the US capital market.

'We spend a lot of time conducting due diligence; what really matters is not the static figure of mNav. Is there a clear management structure? Can financing be done stably? Is there the ability to build a new business model? This is what truly defines an excellent 'DAT startup team.'

In addition to Bitcoin, Ethereum, and Solana reserves, Pantera has also recently invested in several other large-cap altcoin reserve companies. From Bitcoin to mainstream coins to altcoins, the narrative told to investors in the crypto space is also layered: compared to Bitcoin, DAT relies entirely on financial engineering for growth, while mainstream tokens can generate returns through staking and DeFi activities, and altcoin protocols have mature use cases and revenue in the crypto market, allowing stock market investors to gain exposure to their growth through DAT.

Unlike Bitcoin and mainstream coin DAT financing paths, many altcoin DAT's initial reserves come directly from the protocol foundation itself or its token investors.

The initial reserve of the Hyperliquid strategic reserve company Sonnet BioTherapeutics (SONN) was directly injected into the company by top crypto VC Paradigm, which purchased over 10 million HYPE at the end of last year. According to Beating's understanding, the establishment of the strategic reserve company StablecoinX by Ethena was also led by the Ethena Foundation, allowing PIPE round investors to directly use their ENA tokens or USDC for financing.

Due to poor liquidity, altcoin DAT often sees significant surges immediately after fundraising news is announced, providing insider trading opportunities for many participants aware of the situation. In the SONN case, the official announcement was made on July 14, but the stock price had already surged significantly since July 1, quadrupling by the night before the announcement.

Recently, BNB reserve company CEA, backed by YZi Labs, encountered similar issues. According to Beating, to prevent participants from knowing the company name in advance, the team purchased several US shell companies in advance and randomly selected one at the last moment. However, even so, there were still instances of early insider trading just hours before the official announcement on July 28.

On the other hand, many investors are also worried about the potential risk of altcoin DAT having a 'left hand paying the right hand' situation. Due to the poor liquidity in the crypto market, large-cap, high-priced tokens are difficult to exit without discounts. However, by injecting crypto assets into the DAT company, the false liquidity of the tokens themselves becomes real liquidity in the US stock market.

Therefore, whether to 'provide growth exposure' or 'seek exit liquidity' requires careful discernment by investors. 'Many DAT choose to operate in regulatory gaps, such as listing on low-threshold trading boards. But this type of short-term operation is difficult to establish stable information disclosure and compliance mechanisms; if you cannot obtain real capital premiums, it is just passing the buck.'

Regulation is also one of the risks faced by the DAT company. Once the SEC classifies altcoins and other on-chain assets as securities, the structure of DAT will need to be significantly adjusted. However, even so, Primitive and Pantera still believe this is a better battlefield, 'because US stock market liquidity is indeed better, and listed company investors have more protection. Therefore, for us, investing in DAT now is likely to have better odds and payouts compared to pure crypto investment,' Yetta said.

The world outside of the US stock market is still competing for the 'first MicroStrategy.'

The US stock market is the most efficient, inclusive, and liquid capital market, which is a consensus among investors. If one wants to replicate the next MicroStrategy, Nasdaq is still the best place. But this does not mean that other capital markets have no opportunities; outside the US stock market, everyone's goal is to become the next Metaplanet.

In the past year, Metaplanet's stock premium has risen sharply, bringing investors over 10 times the return. This 'Asian miracle' success story has led many to see opportunities for regional arbitrage.

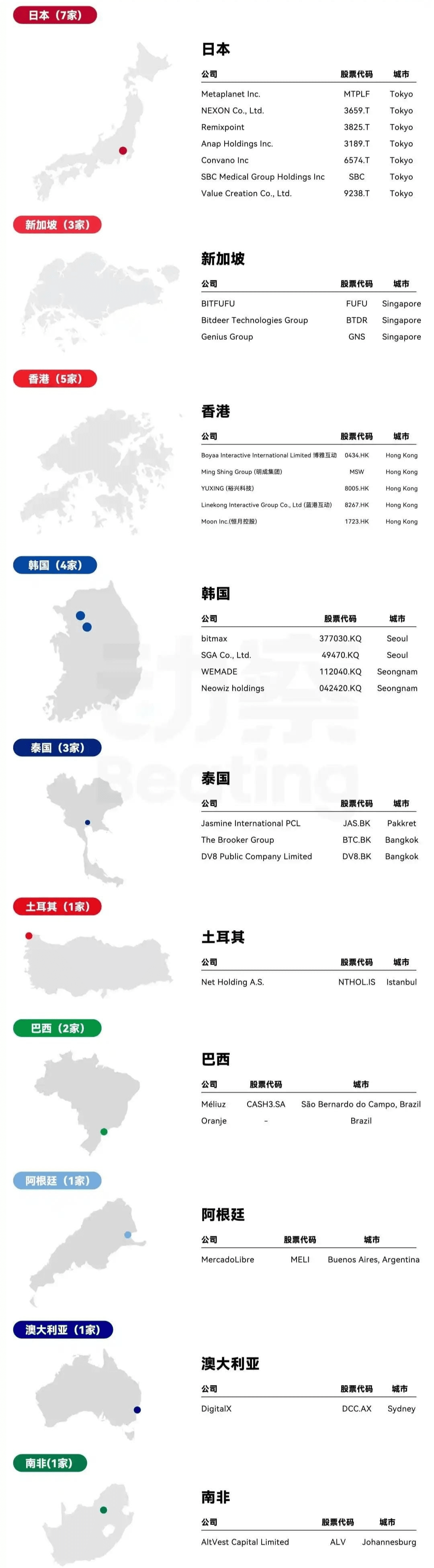

The Asian market is a pioneer in Bitcoin reserves. In mid-2023, Waterdrop Capital partnered with China Pacific Insurance (Hong Kong) Company Limited to establish the Pacific Waterdrop Fund, subsequently investing in the Hong Kong-listed company Boya Interactive, which had just launched its Bitcoin purchasing plan. In 2024, as MicroStrategy's stock surged, Waterdrop further confirmed this industry trend. Currently, Waterdrop has invested in five Hong Kong-listed companies and plans to invest in at least ten by the end of the year.

'It is clear that the current US market for Bitcoin and mainstream coin reserve companies is already very crowded, and the next incremental growth is more likely to come from capital markets outside the US,' said Nachi, a crypto trader who has now joined the wave of investment in reserve companies. This year, he participated in the investment of Bitcoin reserve company Nakamoto Holdings, quickly reaping a 10-fold return.

At the beginning of the year, Nachi invested in Mythos Venture as a personal LP, which specializes in 'Asian Bitcoin reserves.' The recent investment was in the Thai listed company DV8, which recently announced the completion of a 241 million Thai baht financing, becoming the first Bitcoin reserve company in Southeast Asia.

In addition, he also personally participated in several other regional Bitcoin reserve project investments, mostly in seven-figure US dollars. For example, in April of this year, he completed the acquisition of the first Bitcoin reserve company in Latin America, Oranje, which received support from Brazil's largest commercial bank Itaú BBA and raised nearly $400 million in its first round of financing.

'We believe there is still space in markets like Japan, Korea, India, and Australia to do this (Bitcoin reserve company).' After joining Mythos, Nachi's role gradually shifted from LP to 'quasi-GP,' looking for investment opportunities with other members. His task is to find listed companies interested in acquisitions, and 'shell owners' in the Asian region have become Nachi's frequent meeting targets.

'Striving to be first' is key to winning in capital markets outside the US stock market. This not only allows teams to accumulate first-mover advantages but also helps companies capture more market attention. But this also means that the narrative of Bitcoin reserve companies and the regional arbitrage is a race against time.

In the acquisition phase, there are significant differences between shell companies; some can be bought for $5 million, while in the case of Thailand's DV8, several participants spent around $20 million.

From buying a shell to listing and trading, the entire process generally takes 1 to 3 months, with regulatory approval efficiency being the main variable. However, from discovering the opportunity to getting it done, it takes at least 6 months or even longer.

The acquisition of DV8 took nearly a year from start to finish, officially completing in July of this year. The leading investors in this acquisition are UTXO Management and Sora Venture, who are also the main designers behind Metaplanet.

Recently, Sora also completed the acquisition of the South Korean listed software service company SGA. 'The Asian market, especially Southeast Asia, is relatively closed, but the volume here is actually quite large; many foreign investors are unaware of the activity level in these markets,' said Luke from Sora Ventures to Beating.

'Now everyone is racing against time, but in the Asian market, I believe few can compete with Sora.' According to Luke, local regulations pose a significant barrier for many overseas capital sources, as most VCs lack complete experience in acquisitions and communication with regulators, and do not have a good understanding of the Asian market.

Sora Ventures' strategy is to bring in many local partners to help connect with stock exchanges and regulatory agencies to accelerate the progress of project implementation. In the South Korean SGA case, the team took less than a month from start to finish, setting a record for the fastest acquisition in the history of the South Korean stock exchange.

The pace of company financing and market strategy is another barrier. 'mNav is a later-stage valuation model that only holds once Bitcoin accumulates to a certain amount. Early-stage companies operate quite differently from MicroStrategy in terms of strategy and premium logic.' Thanks to equity structures like super voting rights, US DAT companies can ensure team control while continuously diluting equity.

However, Asian listed companies generally lack such mechanisms, so the team's dilution space is relatively constrained. This means the team needs to accurately grasp the pace of financing while using cash flow from main business operations to repurchase stocks for reverse dilution. It is understood that the Thai company DV8 has obtained relevant local licenses and will soon start operations for a cryptocurrency trading platform.

Now, Sora is accelerating the finalization of an acquisition deal in the Taiwanese market while advancing the establishment of a second Bitcoin reserve company in Japan. In May of this year, the team took a 90% stake in Hong Kong luxury distribution company Top Win, which will soon be renamed Asia Strategy. 'Our goal is to create 9 to 10 'Metaplanets' in Asia and then integrate them into a parent company listed in the US stock market, allowing US investors to indirectly gain exposure to the premium of Asian companies through us.'

Top Win has participated in the acquisitions of several companies, including Metaplanet, Hengyue Holdings, DV8, and SGA. The company is also about to complete its initial round of financing, with Sora Ventures continuing to adopt a 'multi-player + small funding' model, raising less than $10 million in total and with a 6-month lock-up period.

Luke hopes that Top Win will present a capital layout of 30% holding in Asian companies and 60% reserves in Bitcoin in the future, to tell investors a relatively different narrative. Of course, all of this is just the team's ideas and stories; whether the premium in the Asian market is sustainable and whether US investors can buy into the Asian narrative remains to be verified by the market and time.

'It must be acknowledged that the Asian market has a high floor and a low ceiling; if you really want to achieve a certain scale, you can only do it in the US stock market, which attracts investors and players from all over the world.' Although investors are trying to chase the Alpha of the Bitcoin reserve narrative in various countries, all investors share a consensus that the Beta that sustains everything still comes from the favorable driving of US regulation.

'If bills like Bitcoin national reserves are truly implemented, the US government's purchasing behavior will drive other regional governments and sovereign funds to align, and Bitcoin could keep rising,' said Nachi.

Saved by 'Coin Stock'

Compared to the dismal crypto market, the current DAT space appears particularly lively. This new wave not only grabs attention but also seems to provide a 'lifeline' for capital trapped in the crypto space. 'Now, all the top 100 crypto projects are considering doing DAT,' one investor told Beating.

By the end of 2024 to early 2025, many crypto VC funds will reach maturity, marking a key point for starting a new round of fundraising. However, poor DPI data has deterred many LPs. Since the beginning of the year, many crypto funds have gradually shut down.

Since 2022, the valuations in the crypto primary market have continued to inflate, with many projects able to raise tens of millions of dollars in the seed round, but few have actual innovation and practical application scenarios. With the development of cryptocurrency ETFs and the FinTech + Crypto space, VCs have become the last choice for LPs to allocate crypto assets.

On the other hand, the continuously shrinking market liquidity is also increasing the difficulty of exit for projects. Retail investors are no longer willing to pay for 'VC coins,' while projects also need to pay high costs for 'listing.' 'Now to get on top trading platforms, you generally have to give up at least 5% of the token allocation, which for a $100 million market cap would cost $5 million. Acquiring a shell company in the US is about the same price.'

But the openness of the US regulatory environment has given everyone new hope. Crypto reserve companies not only found the best exit routes for tokens, but also provided new storylines to attract institutional funds into the crypto space.

In addition to crypto VCs, midstream investment banks have also benefited from this wave. According to Bloomberg, DAT transactions occupy about 80% of many midstream investment bank brokers' working time, and this area is expected to grow by 300% before the end of the year.

Now, the industry is eager to move the $2 trillion crypto market into the US stock market. In less than two months, dozens of DAT companies have emerged in the market.

According to Pantera's vision, significant consolidation will occur in the DAT space within three to five years. When the downward trend arrives, small DAT companies that cannot form economies of scale will fall into negative premium dilemmas and be swallowed by larger competitors at extremely low prices. 'DAT is a 'new type of financial asset model experimental field,' not the center of technological innovation. Ultimately, only two to three companies will survive.'

However, it seems that the music has just begun. Cosmo believes it will take at least another six months for the track to reach a boiling point. 'Ultimately, who will win is completely unknown. All we can do is support those teams that we believe have the potential to become one of the 'two or three' in the future.'