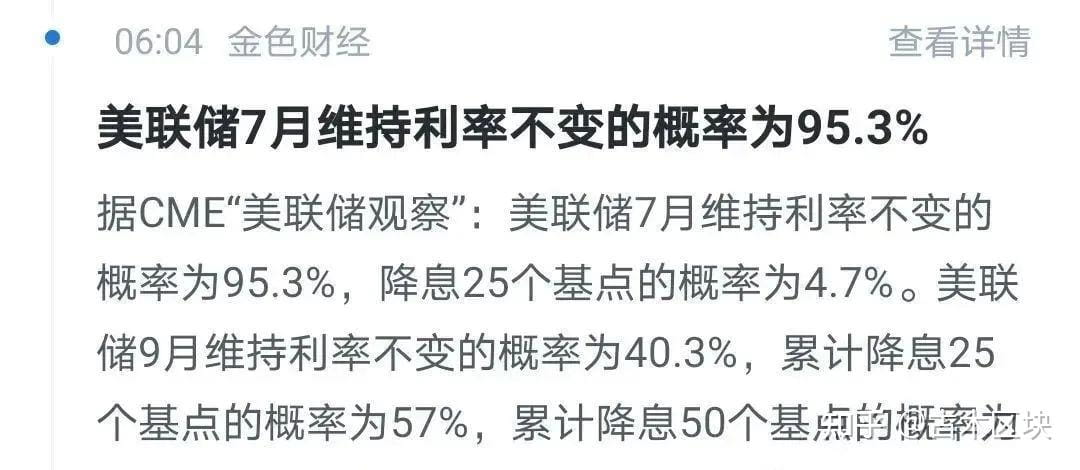

At the end of July, the Federal Reserve's interest rate meeting is widely expected to keep rates unchanged, with a very low probability of a rate cut. The next possible window for a rate cut won’t come until September at the earliest. How much impact will this have on the upcoming crypto bull market? Is it a positive or negative for the market? The answer may be different from what you think!

If the Federal Reserve does not cut rates, will the crypto market be unable to rise? Wrong!

Many people believe that the crypto bull market relies entirely on the Federal Reserve's liquidity. If interest rates do not fall, funds will not flow in, and the bull market will be delayed. However, the logic of the crypto market has never been solely about liquidity. Looking back at past bull markets, Bitcoin's explosion is often strongly correlated with halving cycles, market sentiment, institutional entry, and other factors, while the Federal Reserve's policies are merely an 'enhancement' rather than a 'necessity.'

For example, in March 2020, when the world was flooding with liquidity, Bitcoin indeed soared, but during the bull market in 2017, the Federal Reserve was still raising interest rates, and the crypto market also skyrocketed. This indicates that liquidity can boost a bull market, but it is not the only engine. In the current market, with continuous inflow of ETF funds, accelerated institutional layouts, and persistent global inflation expectations, even if the Federal Reserve delays interest rate cuts, the bull market will still come!

Rate cut in September vs. no rate cut, how will the crypto market react?

If there is no rate cut in July, the market may experience short-term fluctuations, but it will not change the overall trend. The key is whether a rate cut will actually begin in September:

If there is an interest rate cut in September: global liquidity expectations will strengthen, institutional funds will accelerate their entry, and Bitcoin may welcome a new round of explosion, with altcoins going crazy as well.

If there is still no rate cut in September: the market will continue to strategize, but the effects within the crypto market and institutional demand will still be present, and the bull market may proceed more steadily rather than abruptly stopping.

In other words, a rate cut is an 'accelerator,' not a 'switch.' The foundation of the bull market has already been laid, and a rate cut will only make the market more explosive; however, even if delayed, it will not extinguish the bull market completely.

The real risk is not the Federal Reserve, but...

Compared to the Federal Reserve's policies, crypto investors should pay more attention to two key points:

Can you hold on? Bull markets often experience sharp declines, and many people are shaken out due to short-term fluctuations, missing out on the main rising wave.

Can you escape the peak? History shows that 90% of those who make money in a bull market will lose it back in a bear market.

The Federal Reserve's policies will affect short-term fluctuations, but the fate of the bull market ultimately depends on market cycles and your operational strategy. If you can hold on and also formulate a profit-taking plan, then regardless of whether the Federal Reserve cuts rates in July or September, you can still benefit from this wave of dividends!

The bull market has arrived, don’t let short-term noise disturb you!

No rate cut in July? It doesn’t matter! The crypto bull market will never end due to a policy delay of one or two months. Once a trend is formed, it will not easily reverse. What you need to do now is not to get tangled up in the Federal Reserve's actions, but to ensure yourself:

Hold onto core assets;

Control your position; don’t go all-in;

Develop a clear exit strategy.

The ones making money are always the minority, and those who can traverse bull and bear markets never lose their footing due to short-term policy changes. The bull market is still here; are you ready?

Strong rebound, profits doubled! Prepare in advance to win at the starting line.

Keep an eye on: SPK, C