By June 2025, the global scale of 'stablecoins' had surpassed 250 billion.

As early as six months ago (by the end of 2024), when the scale of 'stablecoins' was only 200 billion, a terrifying annual trading volume of 15.6 trillion had already been achieved, surpassing the total of VISA and Mastercard.

'Stablecoins' can be quite complex in principle, but to put it simply, they can also be very straightforward:

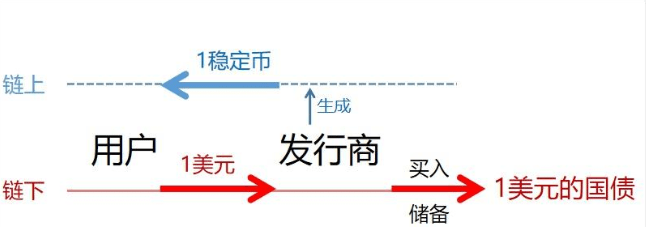

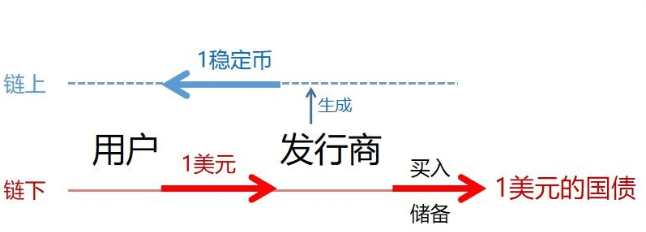

Every time a publisher receives 1 dollar from a user, they generate 1 stablecoin on the blockchain and record it in the user's account. At the same time, they purchase highly liquid assets primarily in short-term Treasury bonds with the received dollars to ensure the user's ability to redeem at any time and stabilize the currency value.

From the user's perspective, it is no different from depositing money into a bank card.

'Stablecoins' are also a type of cryptocurrency and are issued on the blockchain. Therefore, compared to traditional banking systems, 'stablecoins' have reduced the speed of cross-border transfers from 'days' to 'seconds', and transaction fees have dropped from the extortionate 'dollar level' to 'dollar-fraction level', or even lower.

With this natural advantage, 'stablecoins' have already torn open a crack in the high walls of traditional finance, becoming a 'cross-border remittance tool' in the eyes of ordinary users. This year, it has even been packaged by the Emperor as a 'genius tool to defend the dollar hegemony', secretly launching a 'digital colonial war'.

Understanding 'stablecoins' is not only about comprehending a new tool but also about perceiving a financial shadow war that is reconstructing the flow of global wealth.

This article first briefly explains how 'stablecoins' came into being. Then it analyzes several sharp points of contention.

1. Do 'stablecoins' represent a disguised monetary issuance?

2. Is the Emperor fully promoting 'stablecoins' to take over U.S. Treasury bonds?

3. Can 'stablecoins' serve as a reservoir for dollar issuance, thereby avoiding inflation?

4. Does the mission of Hong Kong's 'stablecoins' involve competing for an international currency status on the blockchain?

How did 'stablecoins' come about?

'Stablecoins', which suddenly exploded this year, have actually been around for over 10 years.

In 2014, the first generation of stablecoin USDT was issued by Tether, aimed at solving the biggest pain point of cryptocurrency trading — the extreme volatility of Bitcoin prices, while bank transfers are as slow as a snail.

Users first convert dollars to USDT at a 1:1 ratio, then use USDT to quickly buy Bitcoin, thereby avoiding the risk of the price of currency changing drastically by the time it arrives at the bank.

In 2019, due to the lack of regulation and exposed risks of cryptocurrencies, banking systems finally could not tolerate it any longer, globally refusing to provide services to cryptocurrency exchanges, forcing cryptocurrency trading to shift off-market.

However, for 'stablecoins', the banking action is rather a 'divine assist', as off-market transactions magnify the original pain point a hundredfold. At this point, 'stablecoins' became the only efficient settlement tool, ushering in the first leap — in the following five years, the scale of 'stablecoins' grew tenfold (from 20 billion in 2020 to 200 billion by the end of 2024).

Thus, 'stablecoins' are essentially just a technological tool. It wasn't until this year that the Emperor had a sudden insight and realized its perfect potential to become 'financial nuclear weapons'.

In 2025, even with the Emperor being 'trinitarian', the problems of blocked monetary expansion, blocked fiscal expansion, and sluggish U.S. Treasury bonds still keep him awake at night.

After trying the global tariff stick, attempting to pressure Powell to cut interest rates, and various geopolitical disruptions, the Emperor suddenly had a moment of insight:

'Stablecoins' are inherently designed to resolve the dilemma of sluggish Treasury bond sales; what is lacking is only official endorsement and regulatory standards. Once the shortcomings are addressed, it will break the original balance between risk and efficiency, not only solving the problem of sluggish Treasury bond sales but also breaking through the resistance to fiscal and monetary expansion.

What's even more astonishing is that during this process, 'stablecoins' will also be molded into the 'financial nuclear weapons' of the new era, allowing dollar hegemony to become great again.

Immediately, the 'Mar-a-Lago Agreement' was upgraded to the 'Pennsylvania Plan'.

In June, it was quickly passed in the Senate (GENIUS Act), paving the way for the standardized development of 'stablecoins' and acceptance of federal regulation.

From now on, 'stablecoins' are endowed with the aura of 'on-chain fiat currency', marking the official start of the second leap — the industry conservatively predicts that the scale of 'stablecoins' can still grow more than tenfold in the next five years (to 3.7 trillion by 2030).

After the boom of 'stablecoins', there has been a surge in efforts to popularize it online in the country. After all, it is a new phenomenon, and 'stablecoins' are inherently more complex than traditional financial tools, naturally leading to a series of controversial points.

For example, does the process of generating 1 stablecoin on-chain count as monetary issuance? — Off-chain, 1 dollar is exchanged for Treasury bonds, but on-chain, 1 stablecoin that can buy 1 dollar worth of goods appears out of thin air, from this angle, it seems like issuance. However, the on-chain 'stablecoin' can serve as collateral, while the off-chain Treasury bonds as reserve assets are prohibited from being used as collateral, making it seem like there is no issuance from this angle...

The aforementioned are the current four sharp points of contention.

Both sides of the controversy have presented a series of 'sophisticated' financial theories, but apart from appearing particularly advanced, in the end, neither side can completely convince the other.

The controversial blind spot: 'Do stablecoins count as currency?'

The emergence of this phenomenon usually occurs because an important premise becomes a blind spot.

In the issue of 'stablecoins', the controversial blind spot lies in: 'Do stablecoins count as currency?'

If the second leap of 'stablecoins' is just a flash in the pan, still only applied in limited areas and unable to achieve global proliferation, then users will eventually redeem for dollars, and corresponding 'stablecoins' will be canceled, and reserves of Treasury bonds will be sold again. — Under this assumption, 'stablecoins' do not count as currency, at best they are just a type of advanced gaming currency.

One side of the controversy implicitly accepts this assumption and has not even considered the possibility that 'stablecoins' could achieve global proliferation. Therefore, it naturally concludes:

1. 'Stablecoins' do not belong to the category of disguised monetary issuance.

2. Taking over U.S. Treasury bonds is out of the question.

3. The issuance of 'stablecoins' will not affect real inflation.

However, what if the second leap of 'stablecoins' can successfully achieve global proliferation?

International students use 'stablecoins' to remit money to overseas schools, tourists in Thailand swipe 'stablecoins' to buy mango sticky rice, factories in Argentina pay workers with 'stablecoins'...

Just like twenty years ago, countries not only wouldn't exchange dollars back for gold or oil, but they are also desperately increasing their dollar reserves.

In the global proliferation of 'stablecoins', users will not redeem them for dollars; 'stablecoins' will never need to be canceled; reserves of Treasury bonds will only increase, and reserve assets will no longer need to be 100% frozen. The ratio will continue to decrease, just like banks' reserve requirements.

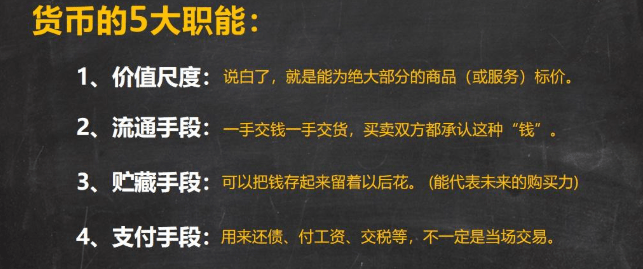

At that time, 'stablecoins' will fully possess the five major functions of currency. — Globally proliferated 'stablecoins' will indeed be currency.

Even if the current 'stablecoins' are still far from global proliferation, under the Emperor's full promotion, on the strong foundation of the dollar as a world currency, and with the high growth rate and high demand for 'stablecoins', global proliferation is highly probable, and it will happen in the next three to five years.

Since it has such strong potential, when considering related issues, 'stablecoins' should be regarded as future currency.

The other side of the controversy concludes naturally based on this consideration:

1. 'Stablecoins' are essentially newly minted currency. It might not be obvious now, but as they become more globally widespread, it will soon become apparent.

The Federal Reserve is now afraid to print money (QE) casually, fearing that dollar depreciation is secondary. The main concern is that more and more countries are no longer using dollars, which is what they fear the most.

In the year 2000, the global foreign exchange share of the dollar was as high as 71%.

In the past decade, this proportion has dropped from 66% to 57.4%, with no signs of rebound during this period, and has even shown a trend of accelerated decline in recent years. If this trend continues, it will fall below 55% within two years, putting dollar hegemony in jeopardy.

On the other hand, dollars account for nearly 100% of 'stablecoins'. As a result, when we talk about 'stablecoins', we are essentially referring to 'dollar stablecoins' without needing to specify the full name.

This is also why they urgently need to 'make dollar hegemony great again'; why the (GENIUS Act) was able to pass swiftly.

After global proliferation, 'stablecoins' will become a new type of global foreign exchange reserve, one that countries cannot shake off. At that time, if the Federal Reserve prints money (QE) to buy its own 'stablecoins', countries can only watch their wealth being plundered.

Don't think this is unbelievable. — Twenty years ago, it was also inconceivable for the Federal Reserve to print money to buy its own Treasury bonds. And today, it's already quite common.

2. One of the motivations for the Emperor to promote 'stablecoins' is to solve the dilemma of the sluggish sale of U.S. Treasury bonds.

There are claims that the scale of 250 billion 'stablecoins' is a drop in the bucket compared to the total 36 trillion U.S. Treasury bonds. Therefore, it is impossible for the Emperor to promote 'stablecoins' just to take over U.S. Treasury bonds.

Those who express such views are basically diagnosed as financial novices.

At least 20 years ago, when the Federal Reserve Chairman was Greenspan, they had already figured out how to play the game of U.S. Treasury bonds — dollar hegemony allows U.S. Treasury bonds to keep 'rolling over', so the principal never needs to be repaid.

The scale of U.S. Treasury bonds, which has inflated without looking back for the past 20 years, is the best evidence. As long as new debt can be sold, no matter how many trillions of U.S. Treasury bonds mature, they are just clouds.

What we see in the news is the intense tug-of-war in Congress every year, ultimately struggling to break through the debt ceiling. It always seems very difficult, and sometimes even leads to temporary government shutdowns, but in the end, they always manage to break the ceiling successfully. — On the surface, this is a show for the world, demonstrating that the U.S. is a creditworthy country and that Treasury bonds are not casually issued; in reality, it is a form of welfare for the opposition party, providing an opportunity to extort the ruling party once or twice a year.

According to complete statistics, since 1960, the U.S. debt ceiling has been raised on average every eight months, and it has been raised 103 times so far.

There are often comments on America's debt pressure saying, 'Just the interest payment exceeds 1 trillion each year...'. Little do they know, their 'debt pressure' is just interest.

For the 36 trillion in U.S. debt, simply and brutally calculating at 4.2%, the annual interest is just over 1.5 trillion.

250 billion is indeed a drop in the bucket compared to 36 trillion, but it could be crucial compared to 1.5 trillion.

Currently, the problem they face is merely the sluggish sales of Treasury bonds; it is not that 1 dollar of bonds cannot be sold. Solving the 'sluggish sales' issue has never meant taking over everything, but rather just filling the gap in demand; sometimes, it even only requires raising expectations for demand, and the 'sluggish sales' issue will be resolved.

Moreover, with a conservative estimate of more than tenfold growth in the next five years, calculating from 250 billion is too much 'to see things in a stationary perspective'.

3. The issuance of 'stablecoins' will not temporarily affect real inflation but will only be delayed, not absent.

Moreover, as the global proliferation progresses, the portions that should have been inflationary will gradually 'catch up' with inflation. However, this 'catch-up' may not necessarily occur within the U.S.; wherever 'stablecoins' are spent, the inflation 'catch-up' will occur there.

In short, it is still that familiar taste, that familiar formula — the world pays for America's inflation.

'Stablecoin' issuers are mainly private enterprises, which is actually a very clever move. This way, the action of 'expanding the balance sheet' can be cleverly shifted from the Federal Reserve to private enterprises, leaving the economically illiterate economists confused for a while. They still adhere to the Western economic doctrines from a hundred or two hundred years ago and can only understand the so-called iron law of 'Federal Reserve balance sheet expansion - dollar depreciation - inflation'.

A carefully designed 'monetary metamorphosis'.

In fact, stepping out of the financial perspective and purely analyzing the Emperor's motives, the controversial issues may become simpler.

Promoting 'stablecoins' is about altering the 'Mar-a-Lago Agreement', which is at the level of core strategy. If the goal were not to promote the global adoption of 'stablecoins', but merely to provide temporary support for Treasury bonds and alleviate short-term sluggish pressures, would such a large-scale operation be necessary?

On the contrary, aiming for the global proliferation of 'stablecoins' not only solves the problem of sluggish U.S. Treasury bonds but also realizes the goal of 'making American hegemony great again', making the world pay for America's inflation; thus breaking the dilemma of fiscal and monetary expansion being blocked. This is the kind of business that merchants would engage in.

To put it more vividly, the 'Pennsylvania Plan' is a carefully designed 'monetary metamorphosis'.

The mission of Hong Kong's 'stablecoins'.

Domestic mobile payments in our country are unique on a global scale, and 'dollar stablecoins' trying to leverage the advantage of transaction convenience to gain a foothold here basically have no chance.

However, for most developing countries, 'dollar stablecoins' come with an advanced mobile payment system, are convenient for various imports and travel, and can combat inflation internally, making them highly attractive.

This kind of attraction is equally significant even for many developed countries.

This allows the dollar to regain its global foreign exchange reserve penetration under the disguise of 'stablecoins'.

Since blockchain can bypass banking systems, 'stablecoins' can easily infiltrate capital-controlled countries, reaching new heights that dollars have never reached. — This is how to 'make dollar hegemony great again'.

This is a carefully designed 'monetary metamorphosis' and has secretly launched a 'digital colonial war'.

'Using magic to win against magic' usually only exists in ideal plots. When the opponent is too powerful, the best option is to 'counter magic with magic'.

The EU is urgently legislating, restricting the circulation of 'dollar stablecoins' while accelerating the research and development of 'euro stablecoins'. Japan is also easing regulation while intensifying the exploration of 'yen stablecoins'. This is a clear indication that they prefer to create a small pond rather than jumping into the ocean of dollar hegemony, becoming a 'colony of digital dollars'.

However, magic doesn't necessarily counter magic; sometimes mastering someone else's magic makes it easier to become someone else's nourishment.

For example, South Korea is currently in a dilemma regarding the advancement of 'Korean stablecoins'. On one hand, South Korea hopes to counter the on-chain expansion of 'dollar stablecoins' with 'Korean stablecoins'; on the other hand, South Korea implements partial capital controls, and 'Korean stablecoins' would open the door for exchanging 'dollar stablecoins', accelerating capital outflow.

For our country, 'offshore RMB stablecoins' represent a feasible path. Conservatively, it is a form of defense; optimistically, it could be the key to countering the global financial colonization by 'dollar stablecoins'. It can bypass the SWIFT system of the dollar and further attract countries along the 'Belt and Road' to use 'offshore RMB stablecoins' for payments, continuing to promote the internationalization of the RMB.

Based on the free flow of capital, promoting the 'Hong Kong dollar stablecoin' is a very good 'experimental field'.

Thus, the mission of Hong Kong's 'stablecoins' is mainly defensive and balancing, rather than actively competing for international currency status on the blockchain.

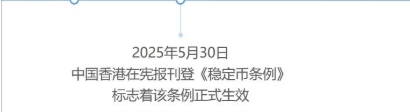

If they were actively competing, they wouldn't have waited until the (GENIUS Act) had completed its process in the U.S. Senate before issuing the first virtual asset trading license with a Chinese background. It should be noted that the Hong Kong (stablecoin regulations) were officially passed in May, and the promotion process is much faster than in the U.S.

If they were actively competing, they wouldn't have waited until after the thorough process of the (GENIUS Act) in the U.S. Senate to issue the first virtual asset trading license with a state-owned background. This is meant to state that our promotion of 'stablecoins' is not like the U.S., playing tricks of 'balance sheet transfer'.

Speaking of licenses, let me also share a few knowledge points:

1. Recently, the stock price of Guotai Junan International has surged, and it has obtained a virtual asset trading license, but not an official stablecoin issuance license. This is the 11th virtual asset trading license in Hong Kong, with the first ten being foreign or Hong Kong-based. The formal stablecoin issuance licenses will be issued after August 1 (stablecoin regulations) come into effect, with only 3 to 5 in the first batch, making them scarcer than virtual asset trading licenses.

2. The surging logic of Guotai Junan International mainly lies in valuation, including the value as a future massive flow entry point, higher transaction fee profits, and the value of scarce licenses (with state-owned background entering the market, they are likely to obtain formal stablecoin issuance licenses). Relatively speaking, the emotional aspect is secondary.

3. For mainland cross-border e-commerce giants, stablecoin licenses represent a huge opportunity to expand into overseas markets. Therefore, we can see that JD's JD-HKD stablecoin has also squeezed into the ranks of five institutions, entering the Monetary Authority's stablecoin sandbox test. However, it should be noted that entering the sandbox does not equate to obtaining a license.

An experiment disguised as 'efficient payment' is quietly rewriting the rules of the currency war.

#上市公司加密储备战略 #山寨季何时到来? #GENIUS稳定币法案

$BTC$ETH