Written by: Shenchao TechFlow

The crypto market is gradually warming up, with BTC and ETH leading the way. However, the main coin prices of many L1 public chains have failed to achieve a synchronized rebound, making the current situation far from when the hundreds of chains competed to be Ethereum killers.

Currently, many L1s face the challenge of 'marginalization of the main coin': circulation unlocks, token dilution, and weak narratives make it difficult for these main coins to capture the value of ecosystem growth.

As an innovative EVM-compatible public chain, Berachain occupies a place in the public chain ecosystem with its unique Proof of Liquidity (PoL) mechanism, but the three-token model also limits its primary token BERA's value capture ability, with a current market cap of only $270 million.

$BERA's current situation stems not only from traditional token economics issues (like unlocking pressure) but also from a lack of narrative and product application layers.

If $BERA is just a tool for paying gas on the chain, its narrative scope would naturally be much smaller. However, a recent PoL V2 proposal in the Berachain official community may provide $BERA with an opportunity to reverse its narrative and functionality:

By reallocating 33% of PoL incentives, the goal is to transform $BERA from a marginalized gas token into a core income asset.

After the proposal was released on July 15, the price of $BERA surged by 23% to exceed $2.5 within 24 hours, and the market has interpreted this as positive and responded accordingly.

Beyond short-term effects, can PoL V2 bring long-term value to $BERA? Can it reshape the primary token's position through incentive mechanisms, attracting institutional and user participation?

The secret dilemma of BERA's value in the first-generation PoL.

To answer the above questions, one must first understand the current situation of the main coin $BERA under Berachain's PoL model.

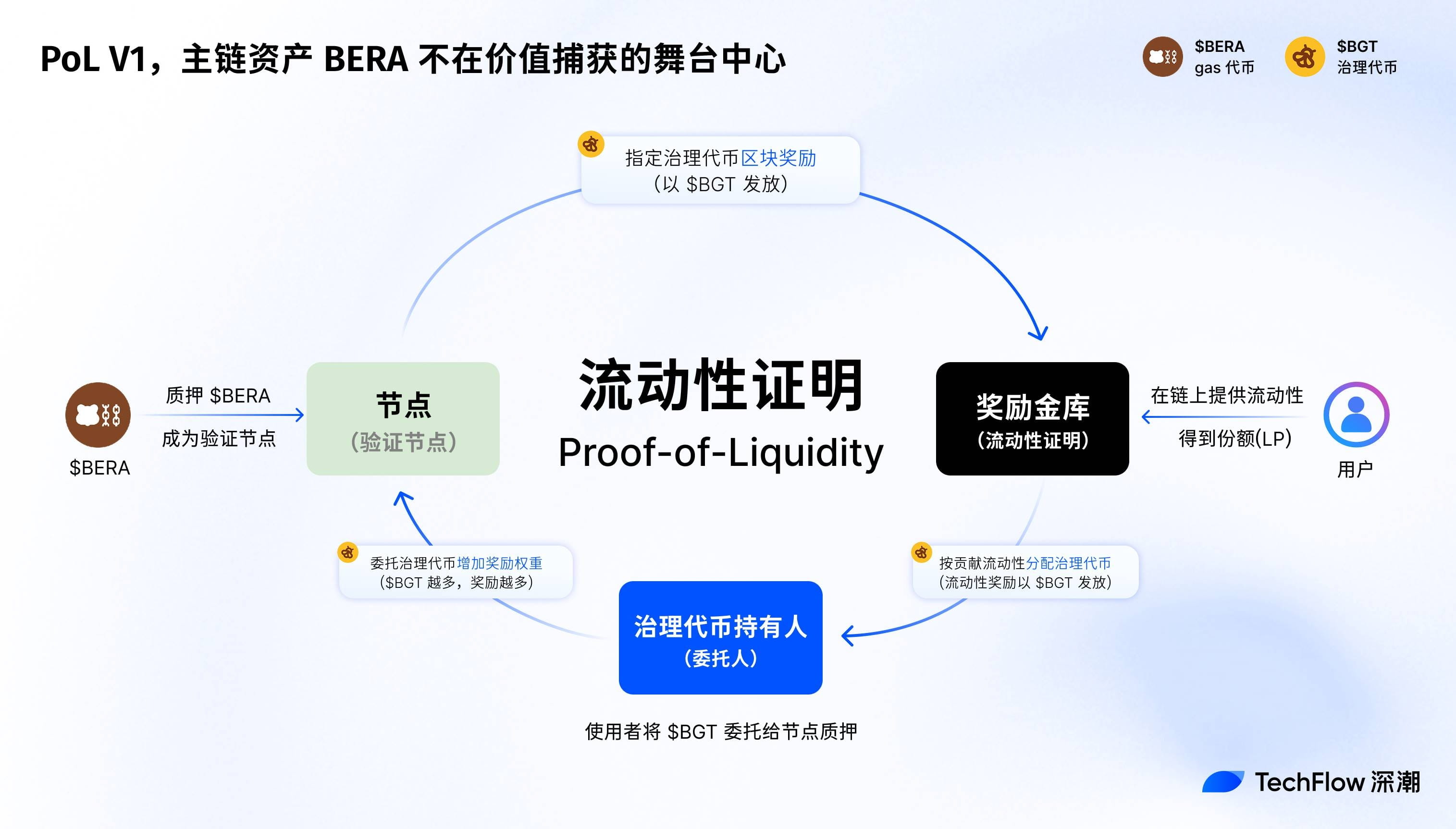

The first-generation Proof of Liquidity (PoL V1) mechanism of Berachain is essentially a consensus design at the economic level, enhancing network security and ecosystem prosperity by incentivizing liquidity providers (LPs) and dApp development.

Unlike traditional PoS, PoL utilizes a three-token model ($BERA, $BGT, $HONEY) to distribute block rewards to validators and ecosystem participants through bribery auctions.

Among them, $BERA serves as the gas token and the network's underlying asset, $BGT is responsible for governance and staking rewards, while $HONEY acts as a stablecoin to support liquidity.

Since the mainnet launched on February 6, 2025, PoL has once driven the growth of Berachain's TVL, which peaked at $3 billion at the end of March this year.

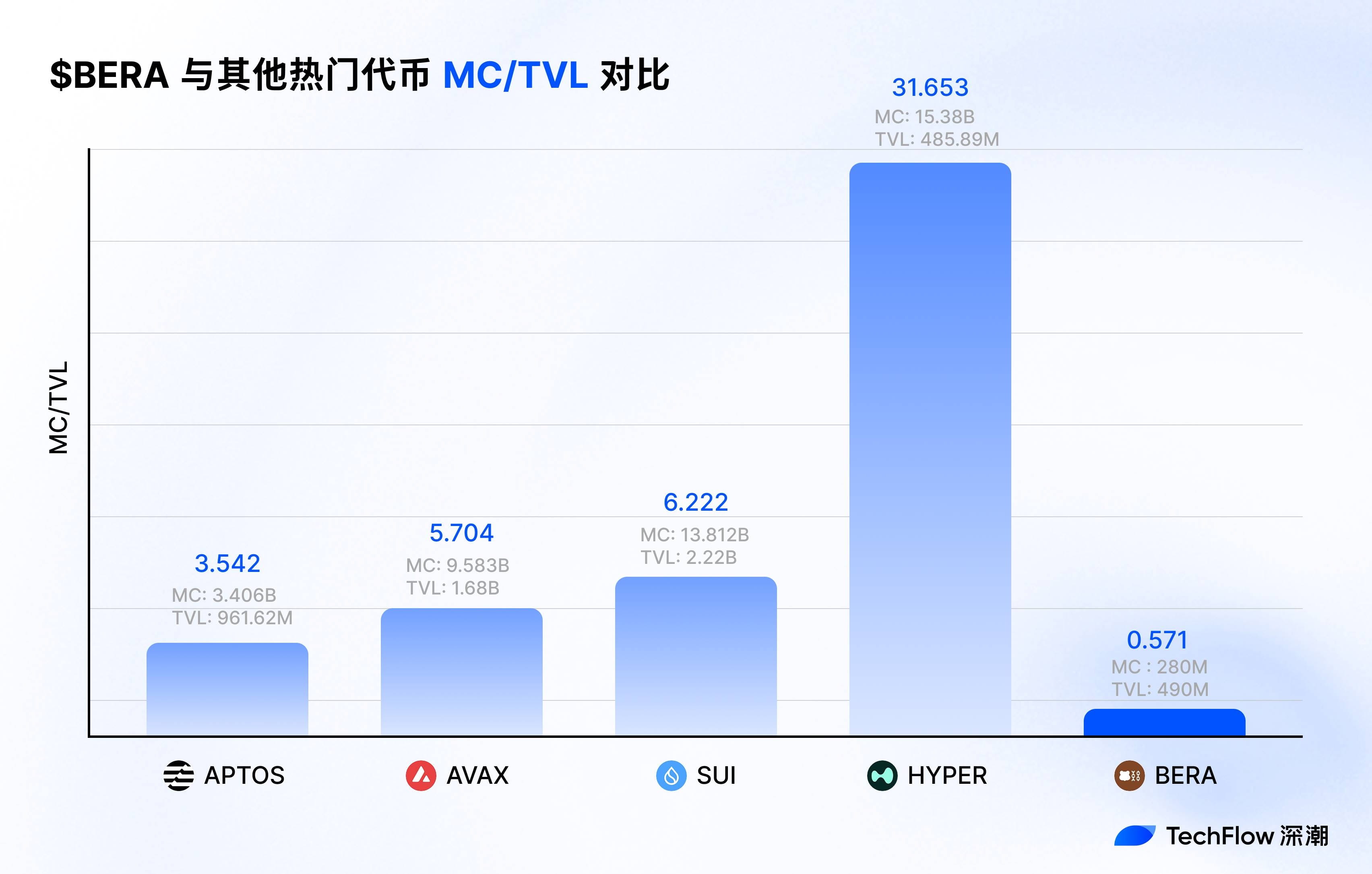

During the same period, the market cap of the main coin BERA was only $900 million, with an MC/TVL ratio of less than one-third; $BERA seems not to have gained better market performance from the attractiveness of the Berachain ecosystem.

Where is the issue?

Looking back at the initial design of PoL, I believe this was an arrangement that obeyed the overall interest, where incentive distribution and mechanism limitations led to the dilution of BERA's value.

The first-generation PoL was designed to strive for more ecosystem activity, structuring clever bribery and emission mechanisms that overall served Berachain's development, but $BERA, as the main chain asset, did not receive equal development opportunities, which is reflected in:

LPs capture the full staking rewards through the PoL bribery mechanism and distribute them using $BGT, while $BERA is only used for gas payments, lacking independent income sources.

Bribery incentives are prioritized for $BGT holders, neglecting the needs of $BERA stakers, which indirectly reduces the market demand for $BERA.

The reward treasury mechanism of PoL V1 concentrated liquidity incentives on dApps rather than the mainnet asset $BERA.

Overall, while Berachain can thrive, the ecosystem can thrive, and meme creations can thrive, $BERA has not thrived. 'Raising the main coin's profile' has become an urgent task for enhancing the public chain's influence in the next phase.

The V2 proposal makes $BERA the core asset of the ecosystem.

Understanding the initial PoL's limitations on BERA's value capture, let’s take a look at the changes brought by the PoL V2 proposal.

To summarize, PoL V2 focuses more on incentive redistribution and functional expansion, attempting to transform $BERA from a marginalized gas token into an ecosystem core asset.

Specifically, PoL V2 introduces the following key changes:

Incentive redistribution:

PoL V2 redistributes 33% of DApp bribery incentives from BGT (governance token) holders back to BERA stakers.

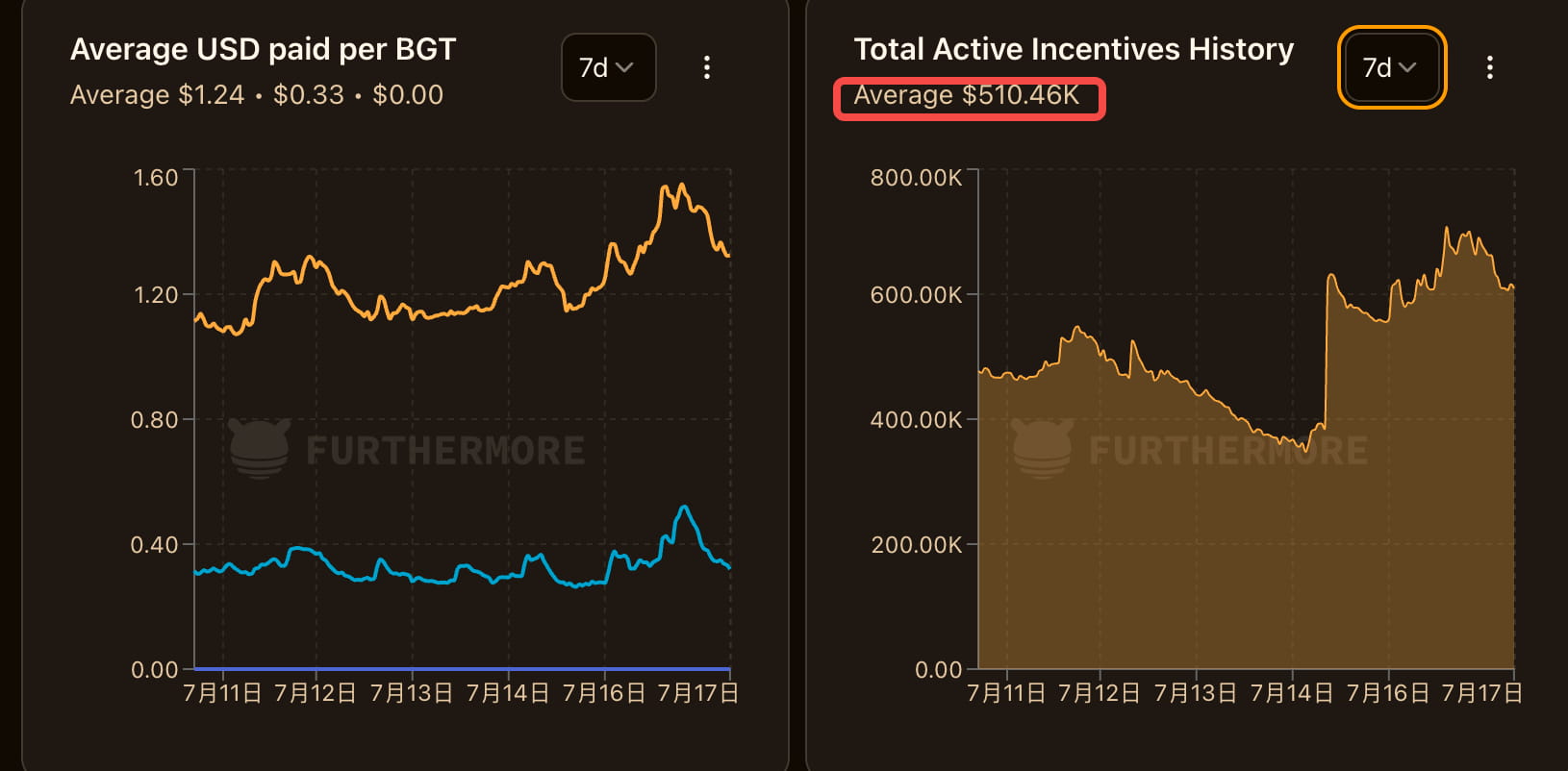

According to furthermore data, Berachain has had approximately $500,000 in total incentives daily over the last 7 days, meaning that one-third (i.e., $150,000) will be directly injected into the BERA staking pool, creating continuous buying pressure on BERA to some extent.

The remaining 67% of incentives continue to be allocated to BGT holders, maintaining their liquidity incentive leverage effect and ensuring that the rights of existing stakeholders are not compromised.

Note that this effectively provides additional income to BERA holders, and the method provided is not through simple issuance of more BERA, but through structural adjustments to redistribute cash flow within the protocol, avoiding the risk of BERA inflation.

Functional module expansion:

PoL V2 supports liquid staking tokens (LST), allowing BERA stakers to earn validator rewards while taking out the staked tokens to further earn PoL incentive income. This significantly improves BERA's capital efficiency.

BERA stakers do not need to engage in complex DeFi strategies or hold BGT to directly profit from on-chain protocols (such as BEX, etc.), lowering the participation threshold.

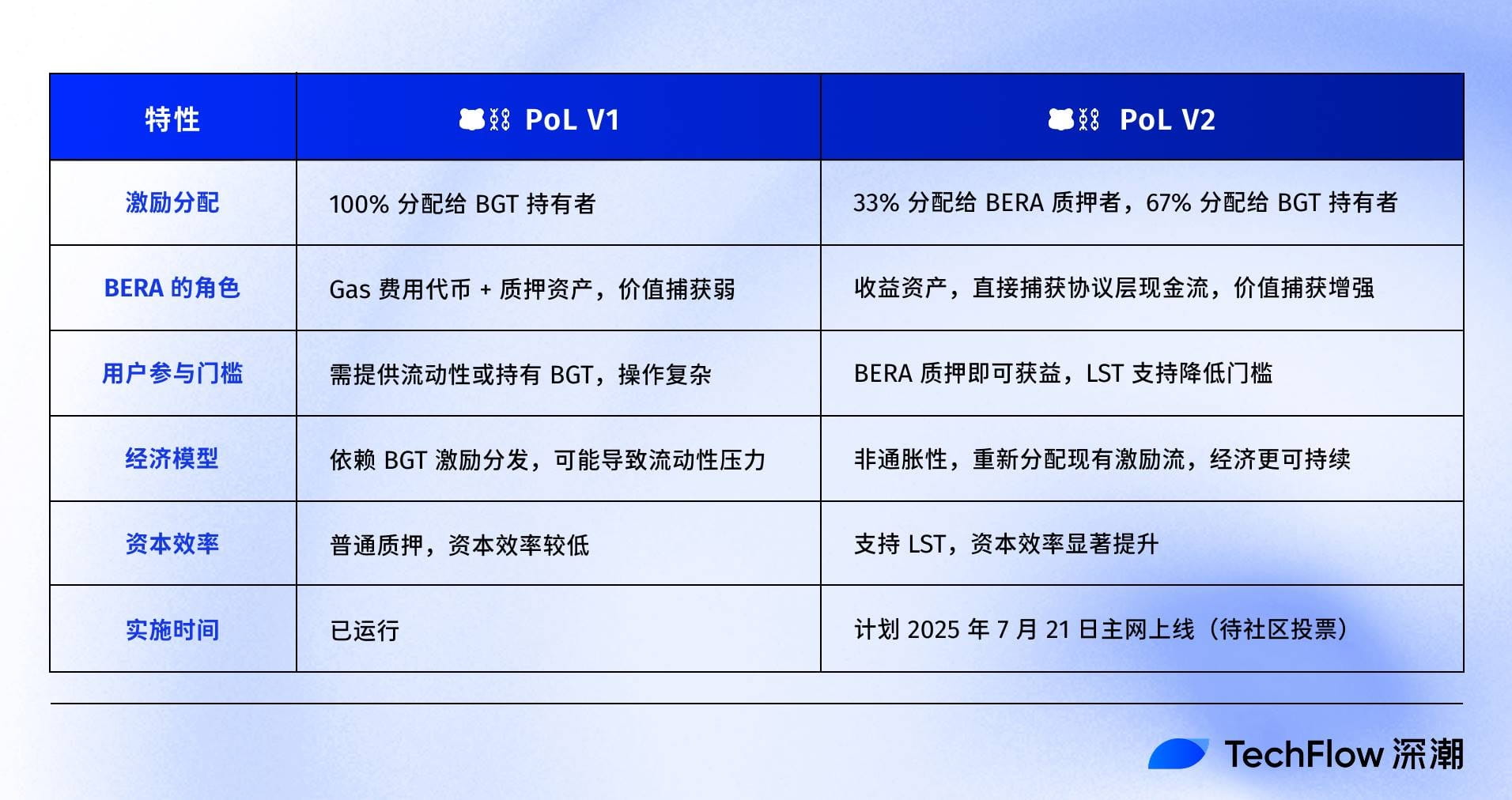

We can also use a table to clearly compare the differences between the V2 and V1 versions of PoL:

In contrast, PoL V1 was more like a tailor-made stage for $BGT, with most rewards flowing to it, while $BERA could only silently pay gas fees, relying solely on ecosystem-driven value growth.

V2 places $BERA at the center stage, simplifying the reward acquisition process through new reward distribution and bond tools.

Value capture, or value capture

Value capture is a high-frequency term in the crypto industry, but for BERA, where exactly is its anchor?

When BERA transitions from a single gas token to a core income asset of the ecosystem, the anchoring of its value will subtly change. This change lies in mental positioning and the ecosystem.

The core upgrade of PoL V2 is to grant BERA the ability to directly capture cash flows at the protocol layer, similar to BERA having the right to protocol dividends, thus reshaping its price logic.

We can calculate a theoretical account.

Assuming the V2 proposal passes, distributing 33% of DApp bribery incentives to BERA stakers, the previous data mentions a total incentive of about $500,000 per day, meaning that one-third (i.e., $150,000 daily, approximately $1.1 million weekly) will become income from staking BERA.

PoL V2 grants BERA a cash flow capture ability similar to 'protocol dividends', which means holding BERA equates to sharing the real income generated within the entire ecosystem, forming buying pressure under the positioning of an income-generating asset; obviously, BERA's price is also affected by token unlocks, and the actual multiples may vary due to TVL growth, adoption rates, or market cycles. However, if the native token is not limited to gas payments and has more productive functionalities, there is clearly greater growth potential based on the current performance of BERA tokens.

For comparison, if we place other public chains together, BERA's current MC/TVL ratio appears to have more potential.

Moreover, positioning BERA as an income-generating asset may trigger broader market imagination.

From an external perspective, companies like MicroStrategy have shown strategic interest in holding cryptocurrencies by reserving Bitcoin. Companies like SharpLink have also started to reserve Ethereum, primarily because ETH is a 'productive asset'.

If PoL V2 grants BERA a stable income stream and non-inflationary design, making it an income-generating asset, it also provides a suitable environment for the current 'coin-stock play'.

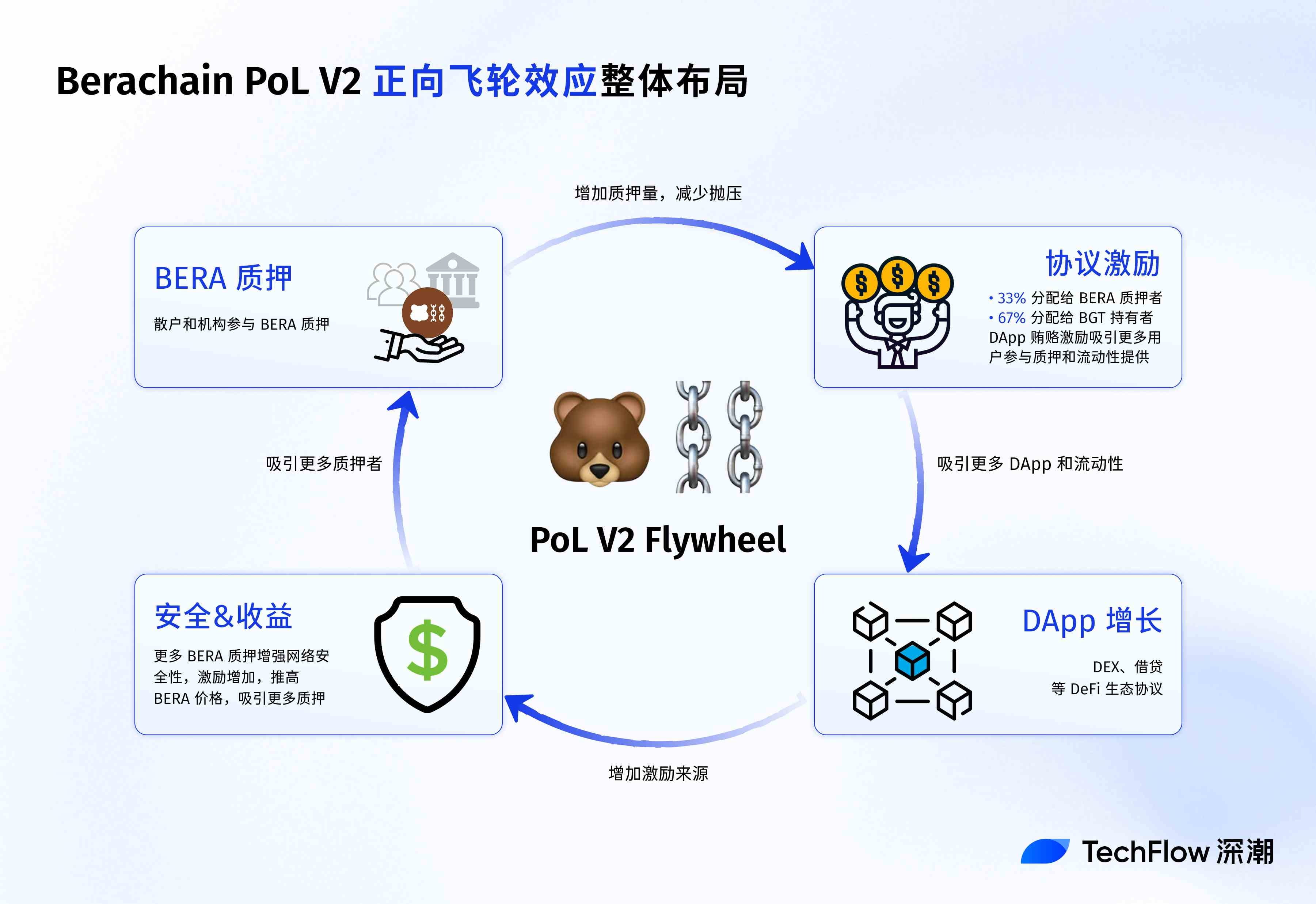

From within the Berachain ecosystem, PoL V2 has spawned a positive flywheel mechanism.

First, the earnings of BERA stakers attract more long-term holders, increasing the token lock-up volume and reducing market selling pressure;

Secondly, the stable BERA price and higher network security attract more developers to deploy DApps, further increasing the sources of bribery incentives. In return, more incentives flow to BERA and BGT holders, creating a closed loop of 'staking-incentive-DApp growth'.

For example, the trading volume of BEX (Berachain's core DEX) may increase due to incentive optimization, thus boosting the usage of HONEY (the native stablecoin) and strengthening the overall ecosystem's stickiness.

Compared to other Layer 1s that rely on issuing tokens to incentivize users, Berachain's model is closer to 'protocol dividends', providing long-term stability for the ecosystem.

Finally, from the user's perspective, the value capture of PoL V2 affects different groups with varying emphasis.

For retail investors, BERA staking provides a low-risk yield path similar to 'crypto savings', attracting more long-term holders. For DeFi players, the introduction of LST means higher capital efficiency and strategic flexibility, such as using LST to provide liquidity in BEX while stacking PoL incentives.

For institutional users, BERA’s income-generating attributes and non-inflationary design make it a potential strategic reserve asset, similar to stablecoins or high-yield bonds.

The current PoL V2 proposal was released on July 15, 2025, in the Berachain public forum and is currently in the community feedback phase, with a deadline of July 20, 2025.

If a majority vote is passed, the mainnet will launch this proposal on July 21, 2025, at which point the changes in BERA's value capture will be reflected.

However, it should be noted that the development of any public chain and the appreciation of its tokens cannot rely solely on a single proposal; the crypto market has come this far, and pure concept speculation has been debunked. Only projects with practical applications, revenue, and solid fundamentals can stand out in the second half of the competition.

As a supplement to the PoL V2 mechanism, when the ecosystem becomes more active, the earnings around BERA will rise. Because more protocols bidding for BGT means higher bribery funds, which also means better BERA staking rewards.

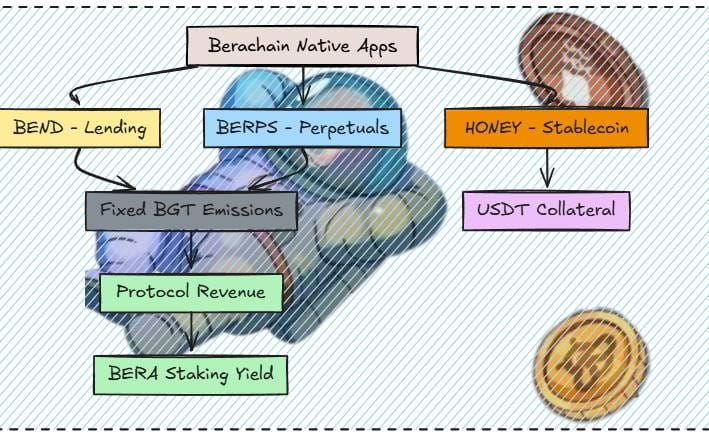

Next, we will see more native DeFi protocols from Bera launching successively, such as the native lending protocol Bend, which will start in 4 weeks; Berp, as a contract DEX, has confirmed its launch and is currently under development; Honey will expand to include more stablecoins as collateral, also set to launch within 3 weeks, enhancing its role as a stablecoin significantly.

(Image source: @0xRavenium)

Additionally, the new Berahub page has recently gone live, upgrading the UI design, introducing a new asset combination page, and one-click Vault operations. It facilitates users to explore the Berachain ecosystem's explore page and participate in various PoL income opportunities, no longer limited to providing liquidity.

Perhaps the projects themselves are gradually realizing that public chains need to make themselves valuable before making the ecosystem valuable.

By using 'income-driven main coins', Berachain's new proposal has made a good start.