Wallets are outdated products and PMF has been criticized a lot. For entrepreneurs, persistence itself is a meaning. You need to persist until Stripe discusses acquisition and MoonPay discusses cooperation. Before that, do everything you can to survive.

Hyperliquid and Phantom are two-way choices, showing the integration of wallets and DEX.

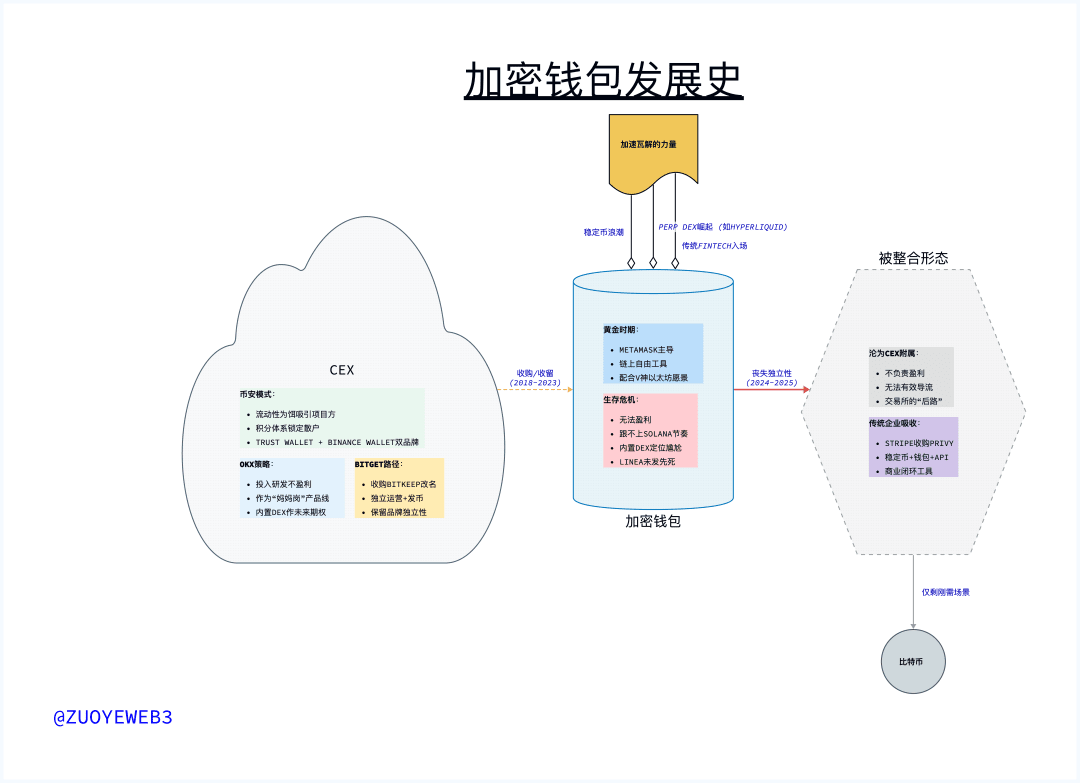

Prior to this, compliant CEXs such as Kraken actively followed Coinbase in deploying wallets, offshore exchanges OKX and Binance were engaged in a love-hate relationship in the wallet field, and Uniswap and 1inch had already launched independent wallet apps.

The trend has changed. As a product concept, crypto wallets have quickly slipped from fashionable concepts such as AA wallets/MPC wallets to a part of the essential product lines of "big companies", just like Feishu, DingTalk and WeChat for Enterprise, which insist on doing SaaS even if they don't make money.

Crypto wallets are the SaaS of Web3. To give just one example, the main chain abstraction Particle Network first provided wallet services to GameFi, with payment based on usage. It was unable to issue coins for a long time, but it seized the opportunity of Meme trading tools and urgently launched UniversalX to complete the coin issuance.

Stablecoin Wave

Pure wallet products, such as MetaMask, are not having an easy time. This is not to say that their revenue and DAU fluctuate greatly, but that people’s imagination and attention are not on them. Like OpenSea, they have gradually entered the end of their life cycle.

Under its influence, Linea has become an L2 that died before it was launched. Under the current narrative of Ethereum returning to L1, it has directly missed the entire L2 cycle. It should have been a twin star like Base, but has become lost in the crowd of L2s.

On the other hand, after Stripe acquired Privy, everyone's attention was not on cryptocurrencies, but on Stripe's layout of stablecoins. While other FinTechs wanted to become the Stripe Web3 version of USDT+API, Stripe's attention was on further integration of stablecoins.

Privy is another wallet SaaS product, which can be understood as helping companies make wallets or access wallet services. This is exactly the same as Stripe's acquisition of Bridge to make a stablecoin API. Privy's goal is to help Stripe complete the closed loop of business logic.

• Stripe 1.0 = API

• Stripe 2.0 = Stablecoin + API

• Stripe 3.0 = Stablecoin + Wallet + API

At present, Stripe's similar competitors are still in the 2.0 stage. Simple external cooperation is not enough. If you want enough companies to accept stablecoin payments, you cannot just use the stablecoin interface to convert it into fiat currency to connect with companies. It is best to let companies manage and use stablecoins natively.

The more persistence, the more offers.

Before the wave of stablecoins, crypto wallets were more free-flowing on-chain Doge tools. The first Doge meme wave triggered by Musk was a direct factor in the rise of Bitkeep and others, while Metamask is more in line with Ethereum’s long-standing on-chain ideal.

In the era when Vitalik was still V God, every EIP/ERC change would point to Gas, wallets and transactions. The goal was to make the on-chain experience usable, easy to use and good to use. The AA and MPC narratives in the wallet, and the ZK and OP in L2 were the strongest beneficiaries of this era, gaining both fame and fortune.

Doge Meme has finally come to an end, and as PumpFun Meme is revived again, the narrative focus has shifted to Solana. Metamask is obviously unable to keep up with the pace. On-chain trading tools rather than traditional DEX have become the mainstream of the era, and wallets with built-in DEX are a bit awkward.

By the way, under the technical narrative, wallets are also moving towards asset management, and in the end it was Fireblock that screwed Bybit over.

Wallets and the development software around them seem a bit helpless at this time, and committing to CEX is one of the few options at this time.

CEX Fusion Device

Reluctantly, CEX has to admit that wallets are the future.

The unspeakable secret is that wallets cannot tell a good story about profitability.

After acquiring BitKeep, Bitget struggled for a while before finally changing its name to Bitget Wallet, while maintaining independent operation and issuing BGB products, which is different from Binance's dual-brand model of Trust Wallet and Binance Wallet, and also earlier than the product independence after OKX Wallet was regulated.

The product models of Bitget Wallet and OKX Wallet both follow the idea of "mother post". They have to have this product line, are not responsible for profits, and cannot even divert traffic to the main site. However, the built-in DEX and other on-chain financial service products are an option they give themselves in the future.

In 2024, OKX invested huge energy and manpower in the research and development of wallet products. I don’t think OKX will necessarily adhere to the concept of decentralization, but the wallet product line will be more flexible than compliance and listing.

However, in 2025, Binance discovered an effective way for the wallet and the main site to interact. It used liquidity as bait to attract project parties to Alpha; used points as a cage to attract retail investors in the era of low returns; and completed the distribution of main site liquidity with the expectation of retail investors taking over.

In an era when the trading volume of the entire CEX is declining, I am really curious about who can design this logic. It seems simple (complexity will reduce the desire of retail investors to participate), but it is already the best solution in the era of low liquidity.

OKX may have the best R&D team in the Crypto industry, but Binance must have the best growth operations manager in the cryptocurrency industry.

The boundary between wallets and trading tools is becoming increasingly blurred. CEX is willing to accept wallets not for the future, but to keep a way out. At least they can comfort themselves that they have a trump card leading to the future. However, just like the exchange public chain and L2, most business lines will eventually be cut.

Competition is everywhere, but the times are changing quietly. The tastes of CEX are changing, but the stablecoin wave has also attracted more traditional FinTechs to focus on this business line, just like Stripe mentioned above, which will not be elaborated here.

Next, let’s talk about the impact and changes that CEX’s Perp DEX has on wallet forms.

Wallet or Perp DEX, the focus of CEX planning has quietly changed.

Aster, invested by YZi Labs, and Byreal, developed by ByBit based on Solana, both show that the focus of CEX is on competing for the future of Perp DEX. The reason is simple. Let’s continue to cue Hyperliquid. HL is the source of all current CEX anxiety.

• More asset types, cryptocurrency stocks introduce high-quality U.S. stock assets

• More market-oriented DEX, CEX is rapidly becoming “institutionalized”, and developing new products is more reliable than improving them

• New user groups: Under the wave of stablecoins, most users who first go online are still exchanges

We will find that the wallet business seems to be more suitable for traditional companies such as Stripe to penetrate the cryptocurrency circle. It will not have much prospects as an independent product or as a CEX business line.

Crypto wallets, as a form of business, may have found their own PMF, but the best outcome is to be acquired. At the moment, even Linea’s airdrop is not expected by anyone. Is there anyone who would still look forward to Metamsk?

Conclusion

As Crypro's earliest product, the wallet started together with the Bitcoin mining hardware, forming people's most complete imagination of cryptocurrency. Except for "temporary" transaction intermediaries such as Mt.Gox, people at that time did practice decentralization without emphasizing that decentralization is the future.

Unexpectedly, Mt.Gox did exist temporarily, but CEX was like the Eye of Sauron, swallowing up all idealists and becoming the infrastructure of the entire industry. It was not until the emergence of Hyperlqiuid that it became possible to truly go on-chain.

Then, wallets were sacrificed and have reached the point where they can no longer exist independently. Except for Bitcoin holders who have an urgent need for wallets, hardware wallets, wallet apps, and wallet service providers are no longer the focus of industry development.

An era ended so quietly.