Overview

Overview

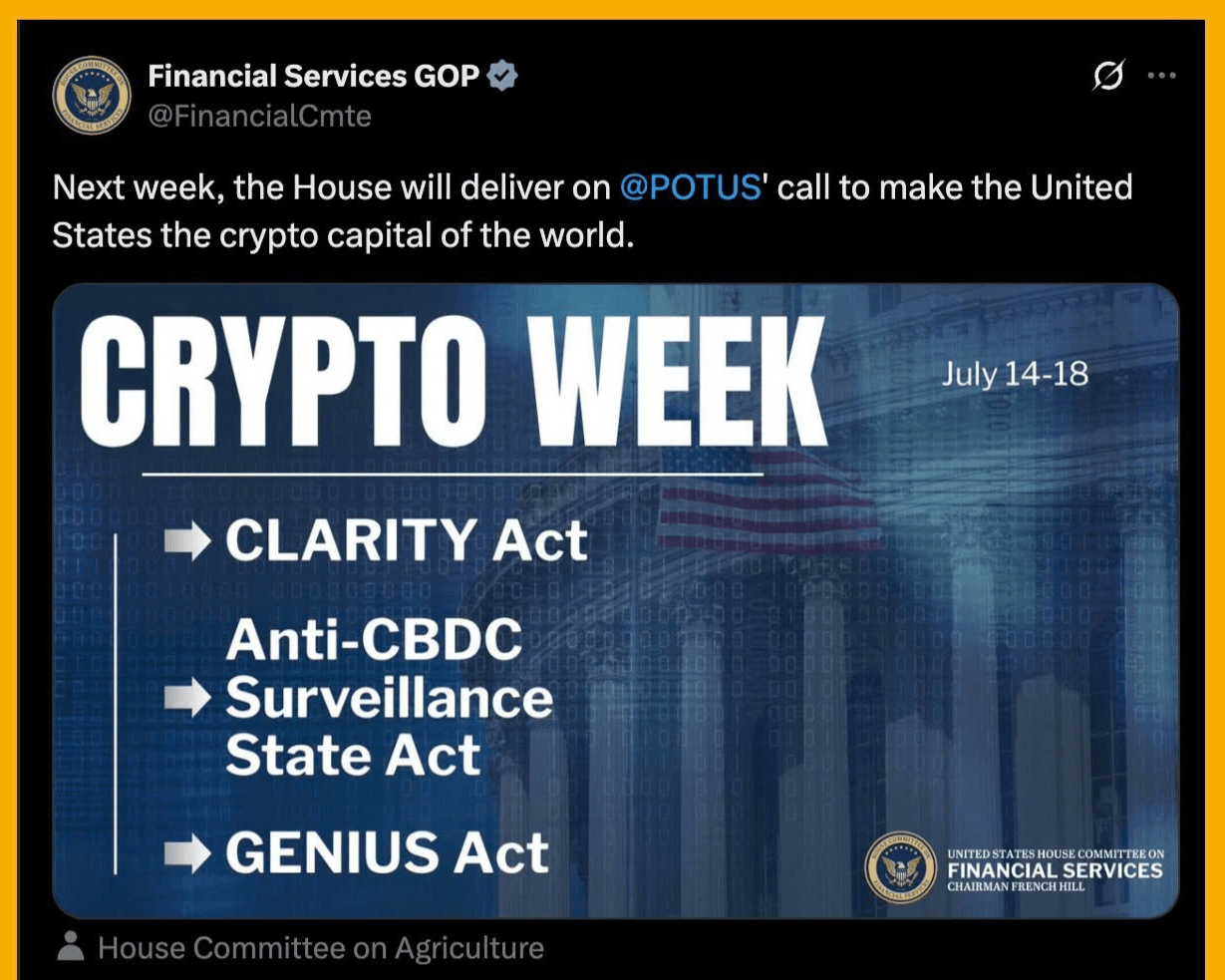

This analysis provides insights into "Crypto Week," scheduled to take place from July 14 to July 18, 2025, in the U.S. House of Representatives. This pivotal legislative phase aims to promote the U.S. strategic goal of becoming the world's leading cryptocurrency hub, in line with President Trump's declared vision. The House will consider three key bills: the Digital Asset Market Clarity Act (CLARITY Act), the Anti-CBDC Surveillance Act, and the GENIUS Act. Each bill addresses crucial aspects of digital asset regulation—market structure, central bank digital currency (CBDC) policy, and stablecoin oversight—together seeking to establish a comprehensive, clear, and innovation-friendly legal framework. This article details the key provisions, legislative status, and expected impacts of each bill, along with an examination of their broader implications for financial innovation, competitiveness, and the U.S.'s global leadership role in the digital economy.

1. Introduction: "Crypto Week" – A Pivotal Moment for the U.S. Digital Asset Leadership

"Crypto Week," scheduled for July 14-18, 2025, marks an important legislative initiative of the U.S. House of Representatives, signaling a coordinated effort to establish a strong and clear legal framework for digital assets. This intensive debate and voting phase highlights a strategic move to position the U.S. as a global leader in innovation and adoption of digital assets.

Overview of "Crypto Week" (July 14-18, 2025) and its significance

The House Financial Services Committee, along with House Agriculture Committee Chairman GT Thompson (PA-15) and House Leadership, has officially designated the week of July 14 as "Crypto Week." This designation highlights an unprecedented focus on digital asset legislation. This initiative is described as a historic step to ensure that the U.S. remains the world leader in innovation, following many years of intensive Congressional efforts on digital assets. This phase is expected to be a pivotal moment for U.S. financial policy, potentially shaping the future of digital assets worldwide.

Context: President Trump's vision for the U.S. as the Global Crypto Capital

This legislative agenda aligns directly with President Trump's promise to make the U.S. the 'crypto capital of the world.' Shortly after returning to the White House, President Trump signed an executive order on January 23, 2025, aimed at supporting the growth and responsible use of digital assets and blockchain technology. This executive order signals a 'lighter' approach to regulation, prioritizing innovation. The executive order also establishes the Presidential Task Force on Digital Asset Markets to propose a comprehensive federal regulatory framework and assess the national 'reserve' of digital assets, including Bitcoin. Majority Leader Steve Scalise (LA-01) emphasizes that these legislative bills advance the President's 'growth-supporting and business-friendly agenda' and provide a clear regulatory framework. The convergence of 'Crypto Week' with the President's 'crypto capital' agenda reflects a strong political mission and heightened sense of urgency accelerated to pass these bills. This is not merely routine legislative work; it is seen as fulfilling a direct presidential promise, which may bolster significant Republican support and momentum for the legislative process. This political alignment elevates 'Crypto Week' to a significantly meaningful event, underscoring its importance beyond the ordinary procedural functions of Congress.

Overview of the three key bills

During "Crypto Week," the House aims to consider three key bills: the CLARITY Act, the Anti-CBDC Surveillance Act, and the GENIUS Act. These bills together aim to establish a clear regulatory framework to protect consumers and investors, provide rules for the issuance and operation of dollar-backed payment stablecoins, and permanently prevent the creation of central bank digital currency. The deliberate decision to consider these three specific bills together during "Crypto Week" reflects a comprehensive and strategic approach to address the most fundamental and urgent aspects of digital asset regulation. This bundling shows a collective effort to build a cohesive 'crypto capital' ecosystem by simultaneously addressing market structure, central bank digital currency policy, and stablecoin oversight, instead of pursuing disjointed legislation. The recurring theme of making the U.S. the 'world leader' and 'crypto capital' emphasizes an important geopolitical and economic dimension to this legislative move. These efforts are not only related to domestic regulation but also aim strategically to ensure a competitive advantage over global rivals (e.g., the EU's MiCA framework mentioned in , and China's CBDC initiatives in ) in the rapidly evolving digital economy. This indicates that U.S. policymakers view leadership in digital assets as crucial to maintaining the financial dominance and long-term technological advantage of the nation.

The three key bills under consideration during "Crypto Week" include:

The CLARITY Act: Primarily focuses on market structure and classification of digital assets (jurisdiction of the SEC vs. CFTC). This bill is primarily sponsored by Chairman French Hill (R-AR), Representative Warren Davidson (R-OH), Representative Angie Craig (D-MN), Representative Ritchie Torres (D-NY), and Representative Don Davis (D-NC). It has currently been favorably reported by the House Financial Services and Agriculture Committees and is awaiting a vote in the House.

The Anti-CBDC Surveillance Act: Focuses on prohibiting the issuance of U.S. central bank digital currency (CBDC). This bill is primarily sponsored by Representative Tom Emmer (R-MN-6) in the House and Senator Ted Cruz (R-TX) in the Senate. The House version (H.R. 5403, 118th Congress) has passed the House; the new version (H.R. 1919, 119th Congress) has been reported by the Financial Services Committee; the Senate version (S.1124) has been introduced.

The GENIUS Act: Focuses on comprehensive regulation of payment stablecoins. This bill is primarily sponsored by Senator Bill Hagerty (R-TN), Chairman Tim Scott (R-SC), Senator Kirsten Gillibrand (D-NY), Senator Cynthia Lummis (R-WY), and Senator Angela Alsobrooks (D-Md.). The bill has passed the Senate and is awaiting a vote in the House.

2. The CLARITY Act: Establishing a Foundational Regulatory Framework for Digital Assets

The Digital Asset Market Clarity Act (CLARITY Act) is an important bill aimed at addressing the regulatory ambiguity that has hindered the development of the digital asset market in the U.S. Its primary goal is to create a clear legal environment, promoting innovation while protecting consumers and investors.

Purpose and Objectives

The CLARITY Act establishes clear, functional requirements for participants in the digital asset market, prioritizing consumer protection while promoting innovation. This bill aims to provide overdue strong protections and regulatory certainty. It promotes American innovation and reinforces the U.S. leadership role in the global financial system. The bill addresses challenges by establishing a clear framework for the digital asset market and filling existing regulatory gaps. Ultimately, it is seen as essential to restoring trust, encouraging innovation, and keeping businesses in the U.S.

Key provisions

Defining Digital Commodities vs. Securities (SEC vs. CFTC Jurisdiction)

The CLARITY Act plays a central role in delineating the boundaries between the primary financial regulatory agencies in the U.S. It grants the Commodity Futures Trading Commission (CFTC) a central role in regulating digital commodities and related intermediaries. At the same time, it preserves certain jurisdictional aspects of the Securities and Exchange Commission (SEC) over cryptocurrency transactions in the primary market, subject to a new limited exemption. The goal is to clarify jurisdiction between the SEC and the CFTC, a point of significant contention in the industry.

The bill defines 'digital commodities' as a digital asset with value 'intrinsically linked' to the use of blockchain and 'primarily deriving from the use and function of blockchain.' Importantly, the term digital commodities explicitly excludes securities, derivatives, and stablecoins. The bill also clarifies that 'investment contracts' do not include 'investment contract assets,' implying that the instrument itself is not a security if issued through an investment contract. Secondary market transactions of digital commodities are classified as unrelated to investment contracts.

Under the CLARITY Act, regulatory authority is divided as follows:

Digital commodities: The primary proposed regulatory agency is the CFTC, with exclusive jurisdiction. The primary distinguishing criteria are value 'intrinsically linked' and 'primarily deriving from the use and function of blockchain'; not securities, derivatives, or stablecoins. Currently, this jurisdiction is ambiguous and may lie with the SEC (via the Howey Test) or CFTC (for derivatives).

Securities (Investment Contracts): The primary regulatory agency is the SEC, with a proposed new limited exemption. The primary distinguishing criterion pertains to the offering and sale of digital assets under investment contracts; not including 'investment contract assets.'

Stablecoin: Under the CLARITY Act, stablecoins are defined separately, not as commodities or securities. The CFTC and SEC will share oversight of 'authorized payment stablecoins.' Currently, this jurisdiction is ambiguous, potentially lying with the SEC, CFTC, Treasury, or banking agencies.

Non-native tokens: May be securities if not 'intrinsically linked' to blockchain. Currently, this authority is ambiguous and may be viewed as securities.

The concept of 'mature blockchain' and its implications

A key concept in the CLARITY Act is "mature blockchain." The bill requires that the value of a digital asset related to a mature blockchain must "primarily derive from the use and function of the blockchain," not restrict or privilege any users, and limit the ownership of certain holders to less than 20% of the total units outstanding. "Mature blockchain" is defined as "a blockchain system, along with its related digital assets, not controlled by any individual or group of individuals under common control."

Issuers may certify to the SEC that their related blockchain has matured, with criteria for the SEC to assess the maturity of the blockchain. Mature blockchains will enjoy fewer reporting requirements, more lenient insider trading rules, and an easier path to be listed on exchanges. This framework is a development from the previous 'decentralized' concept of the FIT21 bill. The core mechanism of the CLARITY Act in distinguishing digital commodities (CFTC) from securities (SEC) and the concept of 'mature blockchain' encourages projects to achieve decentralization. This creates a 'regulatory escape' from tighter securities oversight to lighter commodity regulation, potentially promoting innovation by reducing compliance burdens for mature projects. However, it also creates a complex context where the classification of digital assets determines its regulatory pathway, potentially leading projects to self-design to fit a more favorable category.

Disclosure, Segregation, and Operational Requirements for Market Participants

The CLARITY Act strengthens consumer protections through stringent requirements. Developers will be required to provide accurate, relevant disclosures, including information related to the operation, ownership, and structure of the digital asset project. Digital asset companies interacting with customers, such as brokers and dealers, will be required to provide appropriate disclosures to customers, segregate customer funds from their own, and address conflicts of interest through registration, disclosure, and operational requirements.

Digital asset developers will have a clear path to raise funds under the SEC's jurisdiction, with an exemption from the Securities Act of 1933 registration requirements for investment contract offers related to digital commodities on mature blockchains, as long as sales are limited to $75 million over a 12-month period and a 'offering report' is filed. Issuers of digital commodities related to immature blockchains will have additional reporting requirements. The bill directs the SEC to issue rules within 270 days of enactment to implement additional requirements for immature blockchains and will be allowed to restrict that issuer from relying on the exemption to raise further capital. The act also exempts developers, validators, and non-custodial infrastructure providers from registration requirements. It requires digital commodity brokers-dealers to be members of a registered futures association and clearly adds digital commodity exchanges, brokers, and dealers to the list of financial institutions subject to the Bank Secrecy Act.

Legislative status and bipartisan support

The CLARITY Act has been favorably reported from the House Financial Services Committee (with a bipartisan 32-19 vote) and the House Agriculture Committee (with a dominating bipartisan 47-6 vote) on June 10, 2025. The bill was introduced by Chairman French Hill (R-AR), with bipartisan co-sponsors including Representative Warren Davidson (R-OH), Representative Angie Craig (D-MN), Representative Ritchie Torres (D-NY), and Representative Don Davis (D-NC). Currently, the bill is heading towards a final vote in the House. Its bipartisan support in both committees enhances its chances of passage.

Industry perspectives and critiques

Supporters view the CLARITY Act as a step towards regulatory certainty and innovation. They believe it will restore trust, encourage innovation, and retain businesses in the U.S. The bill also aims to democratize blockchain development by eliminating compliance costs that only well-capitalized large companies can overcome.

However, critics are concerned that this regulatory overhaul prioritizes industry interests over protecting ordinary investors, who may lack the sophistication to navigate increasingly complex digital asset markets without strong regulatory safeguards. Concerns exist that compliance costs related to segregation, custody requirements, and disclosure obligations could be passed on to investors through higher fees, potentially decreasing the number of innovative projects and trading venues as smaller participants withdraw due to regulatory burdens. Representative Maxine Waters (D-CA) described this as the 'Disaster Act,' arguing that it legitimizes corruption, creates significant loopholes that leave investors vulnerable to fraud, and undermines national security, while claiming it is detrimental to startups, giving more power to large banks and cryptocurrency giants. Critics also point to a 'significant gap' in coverage for 'non-native tokens' (e.g., AAVE) that are not closely tied to a blockchain network, suggesting that these tokens could still be considered securities, inadvertently encouraging the proliferation of blockchains seeking lighter regulation.

While supporters claim strong consumer protections through disclosure and fund segregation, concerns that prioritize industry interests and the potential for increased fees may undermine protections for ordinary investors. The gap for 'non-native tokens' also suggests not all digital assets will receive the same level of protection, potentially leaving some investors at risk. This indicates a tension between promoting innovation and ensuring comprehensive safety for investors. Furthermore, the CLARITY Act includes 'strong federal prioritization language to prioritize federal regulation over state regulation for digital commodities.' This is a significant move toward a unified national framework aimed at reducing the patchwork of existing state regulations. However, this may lead to legal challenges and opposition from states that have established their own digital asset frameworks.

3. Anti-CBDC Surveillance Act: Protecting Financial Privacy and Private Sector Innovation

The Anti-CBDC Surveillance Act is a legislative measure focused on preventing the development and issuance of central bank digital currency (CBDC) in the U.S. Its primary aim is to protect citizens' financial privacy and promote innovation in the private sector, in contrast to state-controlled digital currency models.

Core prohibitions

The bill prohibits the Federal Reserve and Federal Reserve banks from providing products or services directly to individuals, maintaining accounts for individuals, or directly issuing central bank digital currency (CBDC) or significantly similar digital assets. It also prohibits the Federal Reserve and the Federal Open Market Committee from using any CBDC to implement monetary policy.

The bill requires Congressional authorization to design, build, develop, establish, or issue CBDC by the Federal Reserve System or the Secretary of the Treasury. It also prohibits the indirect issuance of CBDC through financial institutions or other intermediaries, and prohibits CBDC testing without an Act of Congress. CBDC is defined as a form of digital currency or monetary value denominated in the national currency unit, directly owed by the Federal Reserve/central bank. The bill includes an exception for dollar-denominated currency that is open, non-licensed, and private, while fully preserving the privacy protections for coins and physical currency of the U.S.

Reasons

The main concern behind the Anti-CBDC Surveillance Act is the potential privacy concerns and government oversight. Critics argue that it would grant the government the ability to track all purchases and gather detailed personal information on citizens. Additionally, there are concerns about disrupting banking operations, limiting banks' lending capacity, and supporting economic growth. The bill also argues that CBDCs would overshadow private investment and innovation, threaten persistent inflation, and increase volatility in financial markets. Supporters also argue that CBDCs would violate the separation of powers, as only Congress should authorize and regulate forms of exchange. There are concerns that CBDCs could be 'weaponized' to tax and harass small businesses and individuals. Ultimately, the bill is seen as a safeguard against threats to financial independence and personal freedom, particularly for older Americans who rely heavily on cash.

The Anti-CBDC Surveillance Act is not only a financial technical regulation but also a heightened ideological battleground focused on privacy, personal freedom, and government power abuse. The language used by supporters ("surveillance state", "unconstitutional financial oversight", "tracking all purchase transactions", "weaponized for taxation") reflects a deep mistrust of centralized digital currency control, framing the legislation as a safeguard of fundamental rights rather than merely an economic policy.

Legislative status and strong stakeholder support

The House Bill H.R. 5403 (118th Congress) was passed by the House on May 23, 2024, with a vote of 216-192, and was referred to the Senate Committee on Banking, Housing, and Urban Affairs on June 3, 2024. A new version, H.R. 1919 (119th Congress), was introduced by Representative Tom Emmer (R-MN-6) on March 6, 2025. This version was reported by the Financial Services Committee on May 6, 2025, and was placed on the Union Calendar. Senator Ted Cruz (R-TX) introduced a similar bill, S.1124, in the Senate on March 25, 2025. The bill has received strong support from the American Bankers Association (ABA), the American Priority Policy Institute, the Blockchain Association, the SBE Council, the Independent Community Bankers Association, Restore The Fourth, and the American Citizens Alliance.

Economic and geopolitical implications of the U.S. anti-CBDC stance

The U.S. clearly opposes the issuance of CBDCs, instead prioritizing dollar-backed stablecoins issued by private entities. This stance creates a favorable competitive position for banks to issue their own stablecoins or tokenized bank deposits. Proponents assert that this framework will expand the stablecoin market to $2 trillion by 2030 and ensure 'the dominance of the dollar.' The anticipated growth of dollar-backed stablecoins is expected to increase demand for U.S. Treasury securities. Many central banks, particularly in China and Europe, increasingly voice opposition to the global expansion of the dollar in the digital realm through privately issued stablecoins but face challenges in CBDC adoption due to low demand. The Congressional Budget Office (CBO) estimates that passing the legislation will generate a negligible amount of revenue in the 2025-2035 period due to administrative cost savings from the Federal Reserve not researching digital currency.

The U.S. anti-CBDC stance, along with the push for stablecoin regulation (GENIUS Act), represents an intentional strategy to reinforce the role of the private sector in digital currency innovation. This is a stark contrast to approaches in China and Europe and aims to leverage the existing strength of the U.S. dollar through privately issued dollar-backed stablecoins, thereby extending 'dollar dominance' into the digital realm without requiring the government to directly issue digital currency. Strong support from banking associations indicates a critical alignment of interests. Banks view CBDCs as a threat that could 'disrupt banking operations and limit banks' lending capacity and support for economic growth.' This indicates that the passage of the bill is not only a win for privacy advocates but also a significant victory for the traditional financial sector seeking to protect its deposit base and market position against potential government competition.

4. The GENIUS Act: Comprehensive Regulation for Payment Stablecoins

The U.S. Guide and Establishment of National Innovation for Stablecoin Act (GENIUS Act) is a landmark bill aimed at establishing a comprehensive federal regulatory framework for payment stablecoins. Its goal is to provide clarity, protect consumers, and promote the widespread adoption of these dollar-backed digital assets.

Purpose and Objectives

The GENIUS Act is designed to provide regulation for payment stablecoins. It establishes the first regulatory framework of its kind for payment stablecoins, aimed at bringing clarity to a sector that has been clouded by uncertainty. The bill protects consumers and strengthens national security, while ensuring the stability of stablecoins and consumer protection. It may promote cryptocurrency adoption through stronger oversight, and aims to make cryptocurrency safe and accessible for everyday transactions, giving people confidence in using them. Importantly, it is not designed to replace the dollar, but rather to provide a digital version that offers a similar and safe experience.

Key Provisions

1:1 asset backing and Reserve requirements

The GENIUS Act stipulates that payment stablecoins must maintain full 1:1 asset backing. It requires identifiable reserves backing the outstanding payment stablecoins on at least a 1:1 basis. These reserves may include coins and U.S. currency, demand deposits or shares insured at insured depository institutions, short-term Treasury bills/bonds, funds received under overnight repurchase agreements backed by Treasury bills, reverse repos collateralized by bonds/bills, securities of registered investment companies or government money market funds investing in the aforementioned assets, or other assets approved by the primary regulatory agency, or tokenized forms of these reserves. The bill prohibits riskier reserve assets such as corporate debt or stocks and prohibits rehypothecation of reserves.

Capital, liquidity, and risk management standards

The GENIUS Act establishes strict requirements for capital, transparency, and federal oversight. It requires capital, liquidity, and risk management requirements to be adjusted to the business model and risk profile. This includes standards for diversifying reserve assets and managing interest rate risk. Issuers must have audited reserve reports submitted monthly by a registered public accounting firm, with criminal penalties for false certifications.

Anti-money laundering (AML) and anti-terrorism financing (ATF) measures

The bill establishes anti-money laundering and anti-terrorism financing procedures for coin issuers. Authorized payment stablecoin issuers are considered financial institutions under the Bank Secrecy Act and must comply with all relevant federal laws (economic sanctions, AML, customer identification, due diligence). It requires coordination with issuers to block foreign stablecoins under legal orders. The bill prohibits the offering/selling/trading of foreign-issued stablecoins in the U.S. by digital asset service providers unless the foreign issuer can comply with legal orders.

Priority for Stablecoin Holders in Bankruptcy Proceedings

A key provision prioritizes the claims of authorized payment stablecoin holders over all other creditors in the event of the payment stablecoin issuer's bankruptcy. The bill mandates swift court review and distribution of reserves to stablecoin holders. It amends Title 11 of the U.S. Code to include redeeming payment stablecoins from required reserves as an exception to automatic suspension in bankruptcy proceedings. It gives first priority to any residual claims of stablecoin holders to assets if they cannot redeem all outstanding claims from required reserves. At the same time, it excludes required payment stablecoin reserves from the bankruptcy estate's assets.

While this provision aims to protect consumers and prevent losses as seen in previous cryptocurrency bankruptcies, critics like Professor Adam Levitin of Georgetown University argue that this 'attempts to break existing bankruptcy law' and could set a precedent for a 'public bailout package' for the cryptocurrency sector, as it prioritizes stablecoin holders over administrative claims. This indicates a fundamental tension: while aiming to protect individual holders, the novel bankruptcy prioritization could create systemic risk or moral hazard, potentially shifting the burden onto taxpayers if a major stablecoin issuer fails.

Interest rate prohibition and fraudulent marketing

The GENIUS Act prohibits any authorized or foreign payment stablecoin issuer from paying interest or yield to stablecoin holders solely for holding, using, or retaining stablecoin. It also prohibits misrepresentation of insured status (not backed by the full faith and credit of the U.S., not FDIC insured). Marketing a digital asset as a payment stablecoin is illegal unless that digital asset complies with the GENIUS Act.

The main regulatory requirements for payment stablecoin issuers under the GENIUS Act include:

Reserve support: Requires 1:1 backing in cash, U.S. Treasury bills, bank deposits, or other highly liquid federal assets; prohibits rehypothecation of reserves; prohibits risky reserve assets (corporate debt, stocks).

Transparency: Publicly disclose clear and visible redemption policies; publicly disclose all fees; monthly disclosure of reserve composition (including total outstanding stablecoins, reserve composition, average maturity, geographic custodial location); monthly certification by CEO/CFO regarding the accuracy of reserve reports.

Capital, liquidity & risk management: Capital, liquidity, and risk management requirements are adjusted according to the business model and risk profile; standards for diversifying reserve assets and managing interest rate risk.

AML/ATF: Considered a financial institution under the Bank Secrecy Act; compliance with federal laws on economic sanctions, AML, customer identification, due diligence; coordination to block foreign stablecoins under legal orders.

Bankruptcy priority: Claims of payment stablecoin holders are prioritized over all other creditors for required reserves; redemption of stablecoins is exempt from automatic suspension; required reserves are not assets of the bankruptcy estate.

Marketing prohibition: Prohibits misrepresentation of insured status (not backed by the full faith and credit of the U.S., not FDIC insured); prohibits marketing a product as a payment stablecoin unless it complies with the GENIUS Act; prohibits the use of terms such as 'U.S.' or 'United States Government' in the name of the stablecoin.

Interest rate prohibition: No interest or yield shall be paid to stablecoin holders solely for holding, using, or retaining stablecoin.

Other key provisions

The bill limits stablecoin issuance to 'authorized parties.' It empowers existing federal regulators: the Federal Reserve, the OCC, and the FDIC. The bill establishes a dual oversight model: federal oversight for major issuers and coordinated state oversight for others. Ultimately, it clarifies that payment stablecoins issued by authorized issuers are not securities or commodities.

Legislative status: Senate passage and prospects in the House

The GENIUS Act was passed by the Senate on June 18, 2025, with significant bipartisan support (68-30 vote). The bill was led by Senator Bill Hagerty (R-Tenn.) and co-sponsored by Chairman Tim Scott (R-S.C.), Senator Kirsten Gillibrand (D-N.Y.), Senator Cynthia Lummis (R-Wyo.), and Senator Angela Alsobrooks (D-Md.). It was passed by the Senate Banking Committee in March, with support from all Republican members and five Democratic members. Currently, the bill is moving to the U.S. House, where it is expected to pass due to bipartisan support. Polymarket, a cryptocurrency-focused prediction platform, gives an 89% chance that the bill will be signed into law before 2026. President Trump has expressed strong support, urging lawmakers to 'get it to my desk' and stating he would sign the bill 'as is' if the House passes it quickly.

Industry reception and criticism

Supporters view the passage of the GENIUS Act as a significant win for the cryptocurrency industry. They believe it will bolster confidence in a sector that has seen significant instability. The bill provides a safety net for investors, financial institutions, and businesses, encouraging broader adoption of stablecoins and cryptocurrency overall. The stablecoin market is projected to grow significantly, potentially reaching $3.7 trillion by 2030, up from approximately $250 billion today.

However, critics express concerns that the bill could undermine the dominance of the U.S. dollar and risk turning private issuers into 'shadow banks,' potentially threatening global financial stability (according to Amundi, Europe's largest asset manager). Other critics, such as law professor Adam Levitin of Georgetown University, argue that the bill 'attempts to break established bankruptcy law,' setting a precedent for a public bailout package for the cryptocurrency sector, as it prioritizes stablecoin holders over administrative claims. Senators Elizabeth Warren and Jack Reed warn that the bill is insufficient to protect consumers from financial risks and opens the door to government corruption, citing President Trump's income from a family-backed cryptocurrency venture. Although the act prohibits current officials from issuing stablecoins, it does not affect President Trump's previous investments.

The Senate's passage of the GENIUS Act with strong bipartisan support and high likelihood of being signed into law signals an important shift toward legalizing stablecoins within the U.S. financial system. By establishing clear federal oversight, reserve requirements, and consumer protections, the bill aims to bolster confidence and pave the way for stablecoins to transition from speculative assets to widely used payment and transaction instruments, potentially accelerating their adoption by traditional financial institutions and corporations.

The provision prioritizing the claims of payment stablecoin holders in bankruptcy proceedings is an important consumer protection measure, aimed at preventing losses seen in previous cryptocurrency failures. However, critics like Professor Adam Levitin argue that this "attempts to rewrite existing bankruptcy law" and may set a precedent for a "public bailout package." This highlights a fundamental tension: while aiming to protect individual holders, the novel bankruptcy prioritization could create systemic risk or moral hazard, potentially shifting the burden onto taxpayers if a major stablecoin issuer fails.

Furthermore, while the Anti-CBDC Surveillance Act strengthens private stablecoins against government CBDCs, the GENIUS Act directly supports the growth of dollar-backed stablecoins. This dual approach is a strategic move to extend the dominance of the U.S. dollar into the digital asset space. The anticipated growth of the stablecoin market to $3.7 trillion by 2030 and their role as significant holders of U.S. Treasury securities indicate that this legislation is not just about cryptocurrency but also about maintaining the global financial influence of the U.S. in an increasingly digitized world.

5. Broader Implications for the U.S. Digital Asset Landscape

The event 'Crypto Week' and the bills being considered during this time have far-reaching implications for the U.S. digital asset ecosystem, affecting innovation, investment, global competitiveness, and the legal framework.

Impact on innovation, investment, and talent retention in the U.S.

Supporters argue that the new legislative clarity could help retain startups, capital, and talent in the United States. The goal is to encourage innovation and develop Web3 businesses in the U.S. The bills aim to provide regulatory certainty, likely attracting institutional capital. The CLARITY Act specifically aims to democratize blockchain development by removing compliance costs that only well-capitalized large companies can overcome.

The interaction between the three bills and existing regulatory agencies

The three bills together aim to establish a clear regulatory framework for digital assets. The CLARITY Act clarifies the jurisdiction of the SEC and CFTC, with the CFTC taking a central role for digital commodities. The Anti-CBDC Surveillance Act prevents the Federal Reserve from issuing CBDCs, reinforcing the role of the private sector. The GENIUS Act provides a framework for stablecoins, relating to the Federal Reserve, OCC, and FDIC. The overall approach is 'growth-supportive and business-friendly.' This legislative package aims to protect the financial privacy of Americans and fulfill the promise of making the U.S. the crypto capital.

The simultaneous consideration of the CLARITY Act (market structure), the Anti-CBDC Surveillance Act (monetary policy/privacy), and the GENIUS Act (stablecoins) during "Crypto Week" is not coincidental but a deliberate effort to build a comprehensive, interconnected regulatory architecture for digital assets. This integrated approach seeks to provide clarity on various aspects of the cryptocurrency ecosystem, reducing regulatory arbitrage opportunities and creating a predictable environment for growth, rather than addressing issues in isolation.

U.S. competitiveness in the global digital economy

Efforts to make the U.S. the world's cryptocurrency capital are a key driving force. The goal is to maintain the competitive edge of the U.S. and ensure that the U.S. remains a global leader in financial technology. The U.S. approach (private stablecoins, no CBDCs) contrasts with China and the EU (CBDCs). The crafting of this policy will likely provoke predictable global reactions, with other central banks likely to oppose the global expansion of the dollar through private stablecoins.

This legislative move, particularly under President Trump's 'lighter' and 'growth-supporting' agenda, signals a potential shift from the 'regulation by enforcement' approach criticized under previous administrations. By establishing clear legal frameworks, the U.S. aims to promote 'innovation without permission' within defined boundaries, encouraging cryptocurrency businesses to build and operate domestically rather than seek friendlier jurisdictions abroad. This could significantly reshape the global competitive landscape for digital asset development.

The cumulative effect of the U.S. ban on CBDCs (Anti-CBDC Surveillance Act) while simultaneously providing a strong regulatory framework for privately issued dollar-backed stablecoins (GENIUS Act) represents a distinct 'digital dollar' strategy for the U.S. This strategy aims to maintain the global dominance of the U.S. dollar in the digital realm without requiring the government to directly issue digital currency, instead relying on the private sector for innovation in a regulated environment. This stands in stark contrast to state-led CBDC initiatives elsewhere and could become a defining feature of the U.S.'s global financial leadership.

6. Conclusion and Outlook

"Crypto Week" from July 14 to July 18, 2025, represents a turning point in the United States' journey toward establishing a comprehensive regulatory framework for digital assets. This event, driven by President Trump's vision of making the U.S. the global crypto capital, has brought together three key bills—the CLARITY Act, the Anti-CBDC Surveillance Act, and the GENIUS Act—aimed at addressing fundamental aspects of the digital asset market.

If enacted, these bills would provide much-needed clarity on regulatory authority, delineate the roles of the SEC and CFTC, and introduce the concept of 'mature blockchain' to guide asset classification. This approach is designed to promote innovation by providing clearer regulatory pathways, although critics express concerns about potential compromises on consumer protection and the possibility of creating new loopholes.

Furthermore, the U.S. firm stance against government CBDCs, as reflected in the Anti-CBDC Surveillance Act, underscores the nation's commitment to financial privacy and private sector innovation. This, combined with the strong regulatory framework for payment stablecoins in the GENIUS Act, positions the U.S. under a unique 'digital dollar' strategy. This strategy seeks to maintain the global dominance of the dollar through privately issued digital assets, in contrast to state-led CBDC models pursued by other economic powers.

Despite significant legislative momentum and bipartisan support for many aspects of these bills, challenges remain. Implementing new frameworks, coordinating internationally to address cross-border issues, and addressing ongoing criticisms regarding consumer protection and systemic risks will be areas needing continued focus.

Overall, "Crypto Week" marks a significant leap in shaping the future of digital finance in the U.S. If passed, these bills have the potential to solidify the U.S.'s position as a global leader in digital asset innovation, attracting capital and talent while establishing a regulatory framework that could serve as a model for other jurisdictions. However, the development of these regulations will require ongoing oversight and adaptability to navigate the rapidly evolving digital asset landscape.

Source citation

1. House Announces Week of July 14th as 'Crypto Week' | U.S. House Committee on Financial Services, https://financialservices.house.gov/news/documentsingle.aspx?DocumentID=410793 2. US House Sets 'Crypto Week' to Debate Landmark Digital Asset Regulations, https://www.pymnts.com/cpi-posts/us-house-sets-crypto-week-to-debate-landmark-digital-asset-regulations/ 3. Trump's promise to make US world's 'crypto capital' to be a reality soon? Check details, https://m.economictimes.com/news/international/global-trends/us-news-trumps-promise-to-make-us-worlds-crypto-capital-to-be-a-reality-soon-trump-media-technology-group-3-billion-raise-bitcoin/articleshow/121433752.cms 4. Trump 2.0: A New Era for the Regulation of Cryptocurrency and Digital Assets, https://www.pillsburylaw.com/en/news-and-insights/cryptocurrency-digital-assets-trump.html 5. Client Alert: The GENIUS Act: A Compliance Roadmap for Stablecoin Issuers in 2025, https://www.whitefordlaw.com/news-events/client-alert-the-genius-act-a-compliance-roadmap-for-stablecoin-issuers-in-2025 6. The stablecoin race - Atlantic Council, https://www.atlanticcouncil.org/blogs/econographics/the-stablecoin-race/ 7. Chairman Hill Unveils Bipartisan Digital Asset Market Structure Legislation, https://financialservices.house.gov/news/documentsingle.aspx?DocumentID=409749 8. US CLARITY digital asset legislation may leave non-native tokens as securities, https://www.ledgerinsights.com/us-clarity-digital-asset-legislation-may-leave-non-native-tokens-as-securities/ 9. CLARITY Act Advances to Full US House After Committee Votes | PYMNTS.com, https://www.pymnts.com/news/regulation/2025/clarity-act-advances-to-full-us-house-after-committee-votes/ 10. Will Congress Finally Start Regulating the Cryptocurrency Marketplace? - Morningstar, https://www.morningstar.com/economy/will-congress-finally-start-regulating-cryptocurrency-marketplace 11. House Committees Advance Digital Asset Market Clarity Act of 2025 - Morgan Lewis, https://www.morganlewis.com/pubs/2025/06/bipartisan-majorities-in-two-house-committees-vote-to-advance-the-digital-asset-market-clarity-act-of-2025 12. H.R.1122 - 118th Congress (2023-2024): CBDC Anti-Surveillance State Act, https://www.congress.gov/bill/118th-congress/house-bill/1122 13. Text - S.1124 - 119th Congress (2025-2026): Anti-CBDC Surveillance State Act, https://www.congress.gov/bill/119th-congress/senate-bill/1124/text 14. H.R.1919 - 119th Congress (2025-2026): Anti-CBDC Surveillance State Act, https://www.congress.gov/bill/119th-congress/house-bill/1919 15. Text - H.R.5403 - 118th Congress (2023-2024): CBDC Anti-Surveillance State Act, https://www.congress.gov/bill/118th-congress/house-bill/5403/text 16. FACT SHEET: The GENIUS Act Protects Consumers | United States Committee on Banking, Housing, and Urban Affairs, https://www.banking.senate.gov/newsroom/majority/fact-sheet-the-genius-act-protects-consumers 17. Scott Champions Historic Senate Passage of GENIUS Act, https://www.banking.senate.gov/newsroom/majority/scott-champions-historic-senate-passage-of-genius-act 18. The GENIUS Act Just Passed the Senate. Here's What That Means for the Crypto Industry., https://builtin.com/articles/genius-act-crypto-regulation 19. GENIUS Act Has 89% Chance of Passage by 2026 - AInvest, https://www.ainvest.com/news/genius-act-89-chance-passage-2026-2506/ 20. The GENIUS Act: A New Federal Framework for Stablecoin Issuers, https://www.pillsburylaw.com/en/news-and-insights/genius-act-stablecoin-issuers.html 21. The Digital Asset Market Clarity (CLARITY) Act establishes clear, functional requirements for - House Financial Services Committee, https://financialservices.house.gov/uploadedfiles/2025-05-29_-_comms_one-pager_-_clarity_act_of_2025_-_final.pdf 22. Crypto Legislation: An Overview of H.R. 3633, the CLARITY Act ..., https://www.congress.gov/crs-product/IN12583 23. Congress preps July crypto push; crypto bank charters all rage - CoinGeek, https://coingeek.com/congress-preps-july-crypto-push-crypto-bank-charters-all-rage/ 24. Crypto Market Structure in Focus: The CLARITY Act | Cato at Liberty Blog, https://www.cato.org/blog/crypto-market-structure-focus-clarity-act 25. Digital Asset Market Clarity Act: The increasing role of the CFTC in regulating crypto markets, https://www.dlapiper.com/en-bh/insights/publications/2025/06/digital-asset-market-clarity-act 26. H.R. 1919, Anti-CBDC Surveillance State Act | Congressional Budget Office, https://www.cbo.gov/publication/61491 27. Congressman Emmer Announces Stakeholder Support for the Anti-CBDC Surveillance State Act, https://emmer.house.gov/media-center/press-releases/congressman-emmer-announces-stakeholder-support-for-the-anti-cbdc-surveillance-state-act 28. S. 1582 - Congress.gov, https://www.congress.gov/119/bills/s1582/BILLS-119s1582es.pdf 29. What the GENIUS Act could mean for stablecoins, crypto investors and potentially taxpayers, https://www.bankrate.com/investing/genius-act-crypto-regulation-bill-stablecoins/ 30. The crypto clarity bill: What the GENIUS Act could mean for investors - Empower, https://www.empower.com/the-currency/money/crypto-clarity-bill-what-genius-act-could-mean-investors-news

$BNB $BTC $ETH #BTCBreaksATH #BTC #cryptoweek #GENIUSAct #Stablecoins