Yesterday, the U.S. dollar index fluctuated downward throughout the day, ultimately closing down 0.54%. U.S. stocks opened lower and the three major indices closed slightly down. Bitcoin fluctuated sideways and fell by 0.02%, while Ethereum dropped by 2.51%.

Yumi mentioned on Monday that the declines in the first two days of this week were market corrections testing lower levels. This morning, major orders entered the market, leading to continuous bullish sentiment. Bitcoin has effectively rebounded above 970, driven by optimistic market sentiment, and investors' confidence in Bitcoin's long-term growth potential has increased.

Sentiment in the crypto market is heating up, with today's fear and greed index at 67.

Yumi operated a rebound on the Silk Road from Monday to Tuesday, with Bitcoin collecting 2424 points and Ethereum collecting 84 points.

Key News:

1. Kansas City Fed President George will be absent from the FOMC meeting; Minneapolis Fed President Kashkari will vote in place of George.

2. The U.S. trade deficit expanded to a record high in March as companies increased imports before tariffs were imposed.

3. Tariffs - ① It is reported that if negotiations fail, the EU will impose tariffs on U.S. goods worth €100 billion; ② The UK and India reached a free trade agreement, where India will cut tariffs on 90% of UK imports, with 85% achieving zero tariffs within ten years; ③ UK media: The UK and U.S. will reach a trade agreement this week, proposing to lower tariffs on cars and steel; ④ Trump: May renegotiate the USMCA.

4. The White House has suspended equivalent tariffs for 90 days and exempted ICT product tariffs, adjusting tariffs on auto parts to avoid overlapping with steel and aluminum tariffs and to compensate automotive companies' costs. The trade negotiation atmosphere between the U.S. and some countries has improved, and a preliminary agreement is expected to be reached soon.

5. Although the data collection period for April non-farm payrolls was early (April 6-12), the latest seasonally adjusted unemployment claims data show that the labor market remains robust (at least on the layoffs side). This data significantly boosts financial conditions.

6. Economist Hazus stated: We are pushing back our first rate cut expectation from June to July (still expecting three rate cuts for the year). Trump's criticisms will not affect Fed decisions—provided inflation expectations remain stable, the Fed will neither cut rates prematurely nor refuse to cut rates in the event of worsening employment.

Latest updates from the Fed:

The Fed's May meeting is approaching, with a growing divergence between 'hard data' and 'soft data', and Powell may stick to a 'wait-and-see' stance.

The Fed's latest interest rate decision will be announced at 02:00 Beijing time on Thursday, with Powell's press conference starting at 02:30. Due to the stronger-than-expected April employment report, the market generally expects the rate to remain unchanged at 4.25%-4.50%, with the money market showing only a 2% probability of a 25 basis point rate cut, and an expected total rate cut of 72 basis points for the year. (Note: This meeting will not update the economic forecast summary, with the next update in June.)

JPMorgan expects the Fed to maintain its policy unchanged, with no substantial adjustments to the statement, as officials emphasize the benefits of waiting and observing, and this decision is expected to be unanimous. The description of the labor market as 'robust' and inflation as 'slightly above target' may be retained.

Morgan Stanley believes the Fed may lower its assessment of economic activity, changing 'sustained robust expansion' to 'slowing growth', and emphasize that 'dual mandate risks are rising'. Additionally, there are variables in the FOMC regarding economic uncertainty.

Regarding forward guidance, Old Powell is likely to not change policy before obtaining clearer information.

Currently, much attention is focused on the impact of Trump's tariffs and to what extent this impact has permeated the economy. 'Soft data' and 'hard data' currently show differences; although the U.S. GDP slipped into a contraction area in the first quarter, labor data has remained solid, showing no obvious weakness.

Overall, 'hard data' remains resilient, while 'soft data' paints a different picture, but the Fed does not seem concerned about this unless these trends begin to reflect in 'hard data'. Regarding inflation, the latest CPI and PCE data show a mild downward trend, aligning with Morgan Stanley's expectations.

As Trump continues to pressure the Fed and recent data reports show that the market has gradually digested the macro effects, there remains an insufficient buffer against recession risks.

April can be said to be a month of turmoil; Yumi believes the Fed will likely maintain a cautious attitude and continue to observe future data reports, with the path to rate cuts potentially being briefly delayed in the coming weeks.

Will the situation in May unfold as expected? Key attention this week is on news developments on Thursday and Friday.

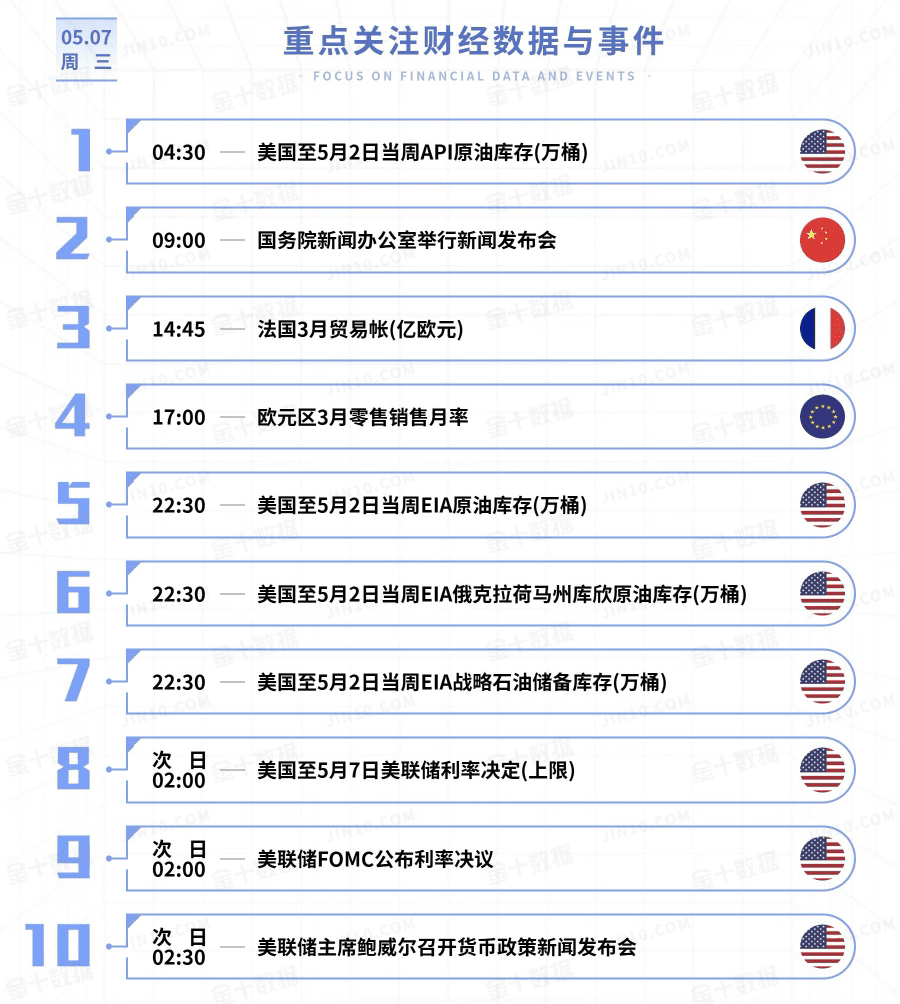

Today’s focus:

17:00, the Eurozone will release the month-on-month retail sales for March, with a market expectation of 0%, and a previous value of 0.30%;

22:30, the U.S. will release the EIA crude oil inventory for the week ending May 2, Oklahoma's Cushing crude oil inventory, and strategic petroleum reserve inventory.

⭐️On the next day at 02:00, the Fed's FOMC will announce its interest rate decision, with the market expecting the Fed to hold steady;

⭐️On the next day at 02:30, Federal Reserve Chairman Powell will hold a monetary policy press conference, and the market will look for signals of a possible rate cut later this year.

For Bitcoin in the short term, Yumi believes that the market will once again break through to new highs, but due to uncertainties in the economic situation, a pullback or sideways movement after a rise is inevitable. In the long term, Bitcoin still has significant volatility.

Some whales continue to stake ETH, showing long-term optimism for the market, which further enhances investor confidence and supports its price. Ethereum may continue to push higher after stabilizing at support levels.

For the medium to long term, current resistance is noted at 990/1900, with support at 930/1750.

Short-term recommendations suggest looking upwards around 980/1880, with attention to 948/1780 below.

Everyone should manage their positions well and defend themselves, continuing to embrace this week’s market fluctuations with a steadier pace! #比特币战略储备 #Strategy增持比特币 #美联储FOMC会议 #比特币预测