Update: The GENIUS Act was signed into law by U.S. President Trump at 6 AM Beijing time on July 19.

On Thursday local time, the U.S. House of Representatives passed three cryptocurrency-related legislations, including the (CLARITY Act), (GENIUS Act), and (Anti-CBDC Surveillance State Act). The (CLARITY Act) and (Anti-CBDC Surveillance State Act) will be sent to the Senate for review.

(GENIUS Act) is expected to be officially signed into law by Trump on Friday local time. The act will take effect 18 months after Trump's signature, or 120 days after the so-called 'major federal payment stablecoin regulatory agencies' including the Treasury and the Federal Reserve issue final regulations implementing the (GENIUS Act).

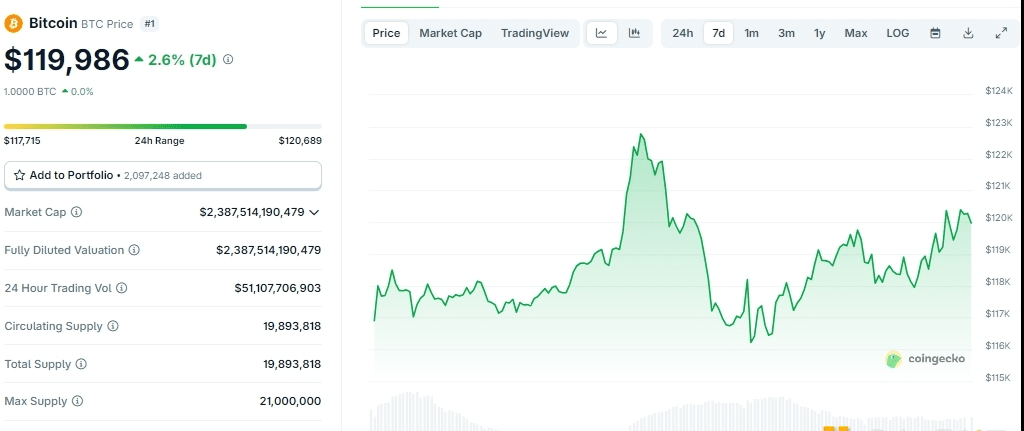

With the positive news of the U.S. regulatory policy landing, the crypto market is experiencing a broad rally. BTC has once again surpassed $120,000, and as of the time of writing, it is at $119,986, with a 7-day increase of 2.6%.

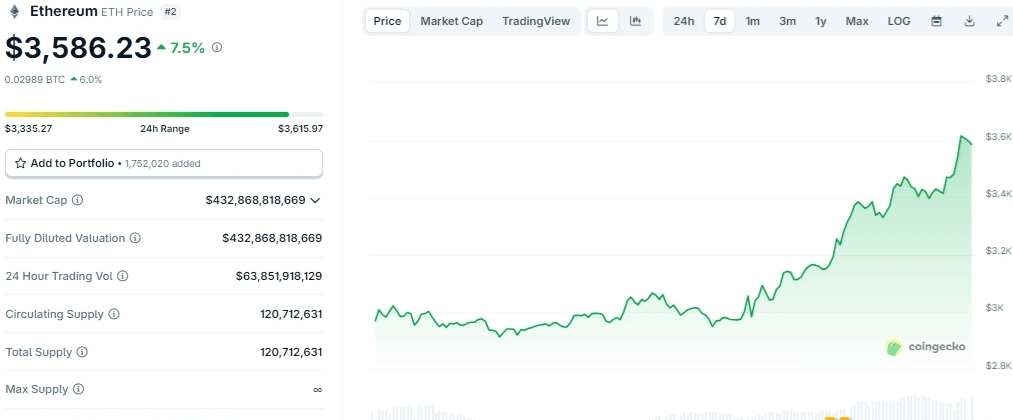

Due to numerous favorable factors, ETH has risen significantly in recent days, surging this morning to break through $3,600, and as of the time of writing, it is at $3,586.23, with a daily increase of 7.5%.

For details, please refer to the article from Golden Finance: '(ETH Returns to $3,000: Six Reasons to Drive the Surge—Is Altcoin Season Coming?)'

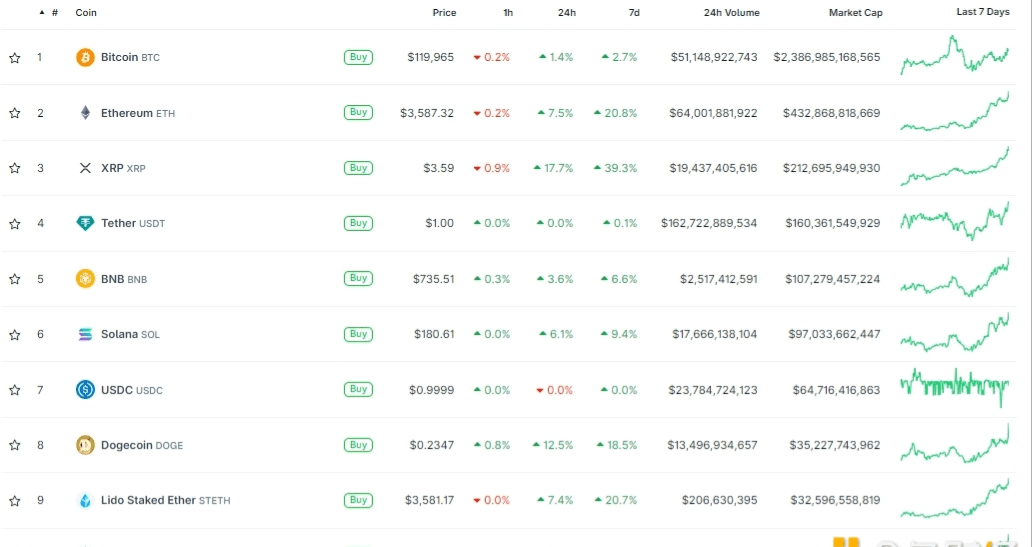

The entire crypto market is showing positive trends, with XRP, DOGE, ADA even recording double-digit gains.

The implementation of U.S. regulatory policies undoubtedly provides a reassurance for the future development of the crypto market. As the (GENIUS Act) is about to be signed into law by President Trump, what impact will the act have on regulators, the banking industry, stablecoin issuers, retail, payment systems, Wall Street financial giants, and publicly listed companies? How do industry insiders view the passage of the act? Will it lead to a season of altcoins?

1. Review of the content of the (GENIUS Act)

(GENIUS Act) Seven key points:

The act prohibits any non-'approved payment stablecoin issuers' from issuing payment stablecoins in the United States.

The act defines 'payment stablecoins' as digital assets that maintain a fixed value supported by fiat currency or other secure reserves.

The act imposes federal standards on institutions approved to issue payment stablecoins, including full reserve requirements, reserve segregation, monthly certifications, and capital and liquidity requirements, as well as a prohibition on rehypothecation.

The act allows state-regulated payment stablecoin issuers to issue stablecoins, provided that the applicable regulatory framework is substantially similar to the federal framework.

The act grants federal banking agencies enforcement authority over approved payment stablecoin issuers, similar to the powers granted under Section 8 of the Federal Deposit Insurance Act to insured depository institutions and their holding companies and affiliates.

The act sets client protection standards for those providing custodial services for approved payment stablecoins, including supervision and regulation, fund segregation, mixed prohibition standards, and monthly audit reports of statutory reserves.

The act prohibits federal banking agencies, NCUA, and SEC from requiring custodial assets to be treated as liabilities. The act also amends federal securities laws, clarifying that payment stablecoins are not securities.

(GENIUS Act) represents a milestone initiative by the federal government to regulate the U.S. payment stablecoin industry through the establishment of clear licensing and regulatory requirements. The act balances federal and state regulatory powers, ensures transparency through audits and reporting, and establishes clear enforcement mechanisms.

If payment stablecoins are recognized within the U.S. regulatory framework, this could open the door for companies to issue their own tokens. Reports indicate that during the debates on the (GENIUS Act), companies like Apple, Google, social media platform X, and Airbnb are investigating this matter, with two U.S. senators questioning whether Meta would have similar plans if the act is passed.

The passage of the act has positive implications for providing regulatory clarity, building a bridge between traditional payments and blockchain, and benefiting the crypto market. Previous articles from Golden Finance have discussed the content and significance of the (GENIUS Act), which will not be repeated here.

For details, please refer to the article from Golden Finance: '(GENIUS Act Passed by U.S. Senate: What Impact on the Crypto Industry?)'

2. The impact of the (GENIUS Act) on various fields.

1. U.S. regulatory agencies: Dual legal framework.

(GENIUS Act) allows various types of regulated entities (such as banks, credit unions, and non-bank institutions) to issue stablecoins and establishes a dual legal framework at the federal and state levels to regulate them.

These entities will be regulated according to their type by the National Credit Union Administration, Federal Deposit Insurance Corporation, Office of the Comptroller of the Currency, Treasury, or Federal Reserve.

It is noteworthy that if the stablecoins issued by entities do not exceed $10 billion, they can choose to be regulated at the state level, but states are not required to establish stablecoin regulatory agencies.

2. Banks: Will be forced to venture into infrastructures like smart contracts.

(GENIUS Act) puts greater pressure on banks and fintech companies, requiring them to provide faster and more programmable payment services. The act will make regulated stablecoins possible and fundamentally promote real-time settlement, round-the-clock fund flow, and programmable financial interactions. This method of fund transfer does not rely on traditional channels such as ACH, wire transfers, or even FedNow.

If end-users and businesses gradually become accustomed to real-time, programmable payments, banks must also keep up with this trend. This adjustment will be tricky for banks, as many will need to invest in infrastructure that supports tokenized payments, smart contracts, and on-chain compliance.

3. Stablecoin issuers:

1) Apply for a national trust bank charter.

Winston & Strawn attorney Logan Payne pointed out: '(GENIUS Act) incentivizes stablecoin issuers to seek banking licenses, as the new stablecoin licenses under the act will restrict companies' activities to 'purely stablecoin issuance,' but most stablecoin issuers do much more than this.

'Currently, almost all stablecoin issuers operating under U.S. law are engaging in activities outside the scope of that license.' Therefore, even if issuers obtain licenses approved under the (GENIUS Act), they will still need state-level money transmission licenses to operate nationwide. This will incentivize stablecoin issuers to apply for national trust bank charters from the OCC.

2) Unapproved issuers will be prohibited.

Three years after the act is signed, it will prohibit the issuance of stablecoins in the U.S. by any unapproved issuers.

Unless stablecoin issuers can and are willing to comply with the legal requirements of the act, it is also illegal to provide foreign-issued stablecoins in the U.S.

The act provides a range of exemptions for foreign stablecoin issuers, including if the Treasury determines that their home country has a similar regulatory regime.

3) Publicly disclose monthly reserve reports.

Institutions approved to issue stablecoins must reserve 1:1 backing for their tokens in U.S. dollars or other currency products (like treasury bills).

Issuers must publicly disclose the composition of these reserves and 'have them reviewed by a registered accounting firm,' while also submitting proof of report accuracy to federal or state regulatory agencies.

4. Payment systems: Facing competition.

Federal Reserve Board member Waller stated that stablecoins bring competition to the payment system but do not pose a threat.

Deloitte researchers believe that stablecoins could steal business from traditional financial institutions and give an edge to emerging fintech companies with experience in digital asset trading. Deloitte's head of digital asset financial services, Roy Ben-Hur, stated: Once stablecoins occupy a more significant position in the payment landscape, stablecoin issuers like New York's Circle Internet Group will have advantages over traditional financial institutions.

5. Retail: Giants explore issuing or using stablecoins.

According to informed sources, retail giants such as Walmart and Amazon are exploring whether to issue their own stablecoins in the U.S. because stablecoins can allow merchants to bypass traditional payment methods—which incur billions of dollars in fees annually, including transaction fees paid when customers use credit cards. Additionally, stablecoins can expedite payment processes, which can be particularly attractive for merchants with suppliers located overseas.

6. Wall Street giants: Exploring the issuance of stablecoins.

Currently, several Wall Street giants, including Citigroup, JPMorgan, Bank of America, and Wells Fargo, are exploring whether to jointly issue stablecoins. The move by traditional Wall Street giants to issue stablecoins marks a gradual bridging of mainstream finance and crypto finance.

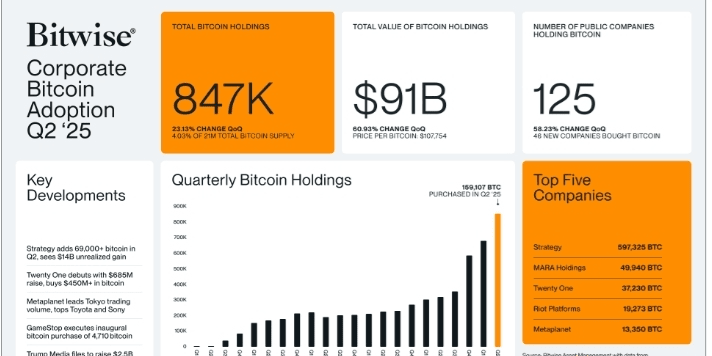

7. Publicly listed companies: Continuing down the path of crypto treasuries.

According to Bitwise data, in the second quarter, 46 publicly listed companies added Bitcoin to their balance sheets, bringing the total number of publicly listed companies holding Bitcoin to 125. These companies collectively hold 847,000 Bitcoins, worth approximately $91 billion.

Recent crypto digital asset investment products recorded the second-highest weekly inflow, reaching $3.7 billion. This brought the total assets under management (AUM) of crypto products to a historic high of $211 billion, with Bitcoin-backed products accounting for $179.5 billion, or 85%.

For details, please refer to the article from Golden Finance: '(From Betting Operators to 'ETH Version of MicroStrategy': Understanding SharpLink's Path to Ethereum Treasury)'

3. Praise and skepticism from industry insiders.

Praise

Digital Assets, Fintech, and AI Subcommittee Chair, Congressman Bryan Steil: Praised the (GENIUS Act) as an important milestone in U.S. crypto policy. 'It encourages innovation and development of U.S. Web3 businesses, establishes clear rules to ensure consumer protection, and provides businesses with a clear regulatory framework to responsibly engage in the digital asset ecosystem.'

Former Commodity Futures Trading Commission member and current CEO of the Blockchain Association, Summer Mersinger: Voting on the (Anti-CBDC Surveillance State Act) indicates support for 'privacy, market competition, and personal financial freedom.'

USDC issuer Circle: The House voted to approve the (GENIUS Act) for submission to the President, which is crucial for the future of the monetary and internet financial system. This indicates strong bipartisan support for responsible innovation and clearly shows that the U.S. will play a leading role in the regulation of dollar-backed payment stablecoins. Circle highly praises the regulatory foundation built by congressional leaders, prioritizing consumer protection, financial integrity, and U.S. competitiveness.

Republic Technologies CEO Daniel Liu: 'We expect two major shifts in the post-GENIUS era. First, financial officers seeking crypto-denominated yields will increasingly turn to native ETH staking and transparent re-staking vaults. Second, yield-generating tokens will evolve into clearly defined, auditable assets—distinct from stablecoins and not bound by traditional regulatory assumptions. Both trends could increase Ethereum's trading activity and fee generation, thereby enhancing ETH's long-term value and strengthening the rationale for institutional funds to hold ETH.'

Bitwise Onchain Solutions Strategic Advisor Tim Lowe:The stablecoin legislation may have a greater impact on Ethereum than on other networks, as over half of the stablecoin supply remains within its ecosystem.

Skepticism

California Congresswoman Maxine Waters: 'The Republican crypto legislation we are considering will create huge loopholes in our federal financial laws, putting consumers and investors at risk in the name of innovation. These bills will increase the likelihood of a costly financial crisis re-emerging, like in 2008, resulting in trillions of dollars in wealth evaporating under the guise of innovation.'

Democrat Sean Casten: 'Central bank officials warned last week that stablecoins threaten global financial stability and require stricter regulations than traditional finance.' 'The GENIUS Act ignores all these expert opinions and instead ties stablecoins to our financial system without the safeguards demanded by banks and investment firms.'

4. Will a season of altcoins arrive?

OSL Chief Business Officer Eugene Cheung stated: 'The resilience of the cryptocurrency market reflects growing confidence among institutional investors. Major companies are rapidly accumulating ETH as part of their reserve strategies, while BTC maintains its stable dominance. SharpLink's bet on ETH highlights the structural shift of cryptocurrency as a macro asset class.'

Risk appetite sentiment has risen following the passage of the (GENIUS Act), which is widely seen as a catalyst for favorable cryptocurrency legislation. Bitcoin once hit an all-time high and is currently stabilizing around $120,000, while the strong momentum of ETH has driven the rise of other altcoins—during periods of rising market confidence, altcoins often rise in sync with ETH.

BTSE COO Jeff Mei stated: 'A season of altcoins seems very likely to arrive, especially if the Federal Reserve cuts interest rates.'

As the ETH/BTC ratio rebounds, ETH's dominance—long overshadowed by BTC's macro narrative—begins to re-establish itself. Given that ETH's 24-hour trading volume reached $64 billion and the inflows of ETH-related ETFs continue to rise, traders are likely preparing for a third-quarter upward trend led by Ethereum.

BTC ETH PEPE CETUS