With 5000, earning 200,000, let me tell you something practical! Watch how I made it in a month

Contract rolling compound interest +: from over 700 U, which is equivalent to 5000 yuan, to earn a million!

To understand how leverage in futures trading is formed, we need to go back to the past and see how 'speculation' first emerged.

Take the early tulip market as an example.

Suppose you have just signed a tulip futures contract for delivery in May, and you are the buyer (going long), with the agreed delivery price of 1000 yuan per ton and a delivery volume of 10 tons, meaning you need to prepare 10,000 yuan in cash by the delivery date in May.

However, shortly after you purchase, people have a very optimistic expectation for tulip prices, scrambling to sign May buying contracts, meaning there are many long positions in the futures market, far outnumbering short positions, leading to a continuous rise in the price of tulip futures May contracts (note that this refers to the futures contract price, not the spot price, which may behave oppositely). The latest contract transaction price has now risen to 1200 yuan per ton.

So you might think, since you have a buying contract for delivery at 1000 yuan, why not just resell it for a price difference?

You just need to do this: open another position, but this time in the opposite direction. Find an opposite party to sign a May selling contract, meaning you will short at the contract price of 1200 yuan, with a delivery volume of 10 tons—this means you need to prepare 10 tons of tulips for the buyer you signed with in May.

So how do you get these 10 tons of tulips? - Remember you previously signed a 1000 yuan May delivery purchase contract? This means that by then you can first purchase 10 tons of tulips at 1000 yuan per ton, for a total of 10,000 yuan, then sell this 10 tons of tulips you just acquired at delivery to the buyer you signed the contract with at a price of 1200 yuan per ton, receiving 12,000 yuan. Therefore, you netted 2000 yuan.

So it gets even trickier, you will think that you don't even need to prepare this 10,000 yuan in cash, and you don't have to wait for the delivery date to perform the above operations. You just need to say this to the contracting counterpart when shorting: 'Aren't you willing to buy 10 tons from me at 1200 yuan per ton on the delivery date? I happen to have a contract to buy 10 tons at 1000 yuan per ton. I just need to transfer this contract to you; then you take this contract to find the seller of this contract to buy 10 tons on that day, and that will fulfill my contract with you. Oh, of course, you need to give me the price difference, since we signed for 1200 yuan per ton, and I signed with that seller for 1000 yuan per ton, so you need to give me 2000 yuan in price difference right now, especially since tulips are rising so well now, you may not find anyone willing to sign with you at 1200 yuan later.'

Thus the other party also agreed, since it doesn't matter, their total cost is still 12000 yuan, the same as agreed in the contract. Look, in this process you actually do not need to prepare 10,000 yuan; back and forth you have hands-free made 2000 yuan.

We refer to this process as 'closing the position', which can simply be understood as hedging the original contract by making a contract in the opposite direction. At this point, you have no contracts left.

The above process has not yet involved the concept of 'margin', which can be considered as having a margin of 0 in this process, that is, infinite leverage, because you do not need to prepare any funds to net 2000 yuan hands-free.

The above closing brought profit, we can call it profit-taking closing.

Thus, you start to repeatedly implement this brilliant idea, just open a position in the futures market and close it in the same way, without waiting for the delivery date to earn the price difference.

However, the situation may also develop in the opposite direction. Suppose the market has a very pessimistic expectation for tulip prices, with everyone scrambling to sign May selling contracts, meaning there is a lot of short selling in the futures market, far exceeding long positions, then the price of tulip futures May contracts keeps declining, and now the latest price has dropped to 800 yuan per ton.

And you also have a very pessimistic expectation, worrying that by May, the spot market price will be worthless, but you still have to buy at 1000 yuan per ton, and you may not even have 10,000 yuan in cash, so you want to stop-loss beforehand. So you open another position in the opposite direction, opening a May selling contract at a price of 800 yuan per ton, with a delivery volume of 10 tons.

This time you will say to the opposite side: 'We agreed to deliver at 800 yuan in May; I happen to have a buying contract, and I will transfer it to you. You just need to take this contract to the seller I signed with, and they will sell the goods to you, then I will have fulfilled my contract with you. However, my contract stipulates a price of 1000 yuan per ton, but that’s fine, I will make up the difference for you. I’ll give you 2000 yuan, please agree, my friend~'

The opposite side is just the same; ultimately, the total cost they pay is still 8000 yuan, so they agreed to you. You successfully closed the position, but you lost 2000 yuan in this process. We call this 'stop-loss closing'. The above is just an example to illustrate going long; the principle of closing a short position is the same. I won't repeat it here.

So those shorting do not necessarily need to have that much goods in hand; they just need to close their positions before delivery to pocket the price difference. This is also called 'short selling without goods.'

But remember, the profit-taking closing for short positions occurs when the delivery price of the futures contract declines; if the delivery price rises, the closing is a stop-loss closing, which is the opposite of going long.

In simple terms, going long is betting on a rise, while going short is betting on a decline.

As more people operate this way, many do not intend to wait for delivery, wanting to close positions before delivery to earn a price difference. To cater to this group, exchanges introduced standardized contracts. This means a unified format, unified currency, and unified delivery standards. This is what we can see in the futures market on software today. It greatly facilitates speculators who only want to 'speculate'.

Look at charts more and practice

As long as you can accurately identify the several situations mentioned earlier

Regardless of the cycle or situation

You have the ability to discern what the market is doing

Will help you filter out many wrong decisions

More flexible in formulating the right trading plan

Greatly improve your trading performance

In the elements that make up Price Action

Price occupies a significant proportion

I mentioned this at the beginning of the article

Candlestick Yin Yang is a visual representation of price

We can obtain a lot of helpful information for our market analysis from candlesticks

But for more convenient transactions

The market has set regular quantitative signals for us

Thus various candlestick patterns emerged

Many times

Besides the market structure we just learned

We also rely on the candlestick patterns to provide us with double assurance

Give us confidence

Trigger our trading

So learning candlestick patterns is equally important

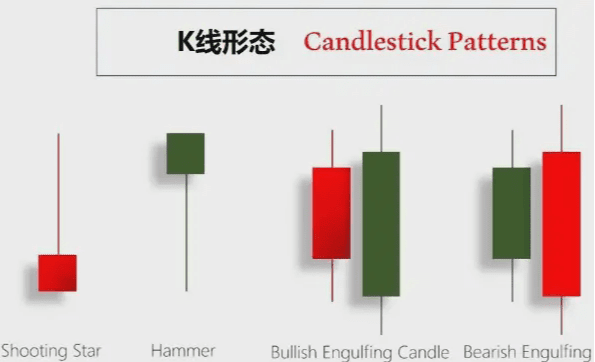

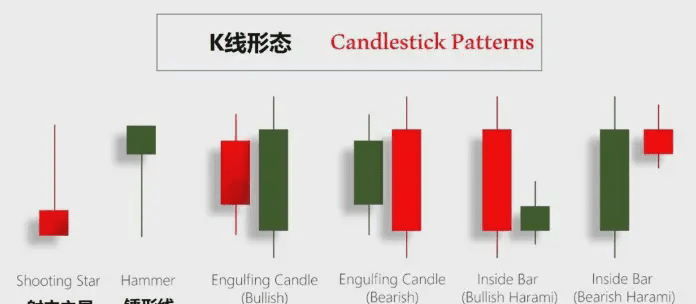

In addition to the shooting star, hammer candlestick, and bearish engulfing patterns we discussed earlier

(Beginner's guide, the source of market profits, interpreting the three levels of Yin and Yang (candlesticks))

Today I will share a more useful candlestick pattern here

First, let's briefly introduce the definition of this pattern

Next, I will tell you how to navigate the market structure in Price Action

Find the most advantageous position

And integrate this candlestick pattern to enter the market

Win a high win-rate trade

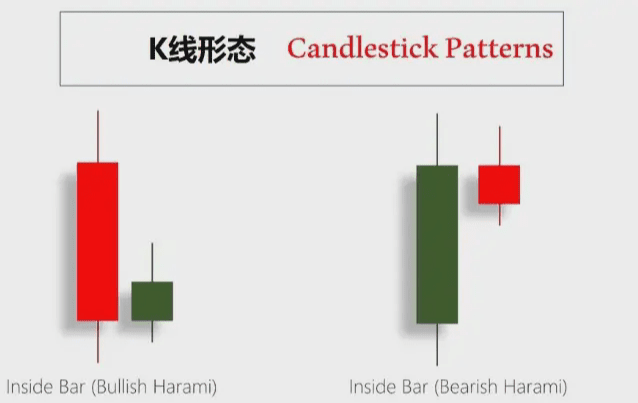

Inside Bar (Pregnant Line Pattern)

Because its shape resembles a pregnant woman

So in Chinese, it is called bearish engulfing and bullish engulfing

A bullish engulfing is formed by a bearish candlestick plus a very small bullish candlestick

This bullish candlestick, whether its body or shadow

All within the previous candlestick

A bearish engulfing is the opposite

The body and shadow of the bearish candlestick are all within the previous bullish candlestick

Generally speaking

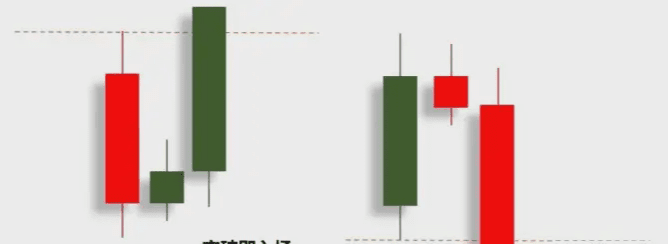

There are two common methods to trade using this pattern

The first one

When the price breaks through the high or low of the previous candlestick

Whether this latest candlestick has ended or not

We will enter to buy or sell

Belongs to left-side trading

The second more conservative approach

It is just waiting for this current candlestick

Truly end at the high or low of the previous candlestick

Only enter the market after establishing a clear direction

When we refer to candlestick patterns for trading

The most taboo is to see a Pin Bar and immediately enter the market

We sell when we see a Pin Bar

Buy when you see a bullish engulfing

.......

This is a very wrong approach

Because of candlestick patterns

Their role should be to confirm the model

Can only serve as assistance

Their composition often does not exceed 3 candlesticks

So it cannot represent comprehensive information and trends

Make trading decisions solely based on them

In fact, this is not a wise choice

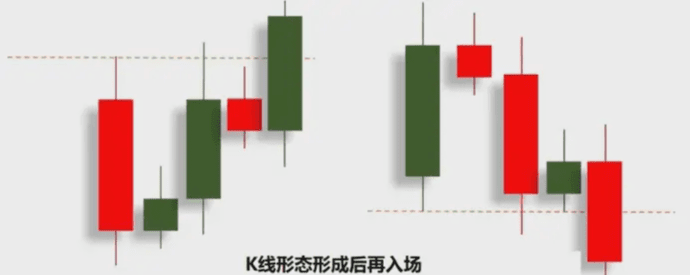

The best practice is to combine with market structure

At the most favorable position

With the most precise entry timing

If you can grasp this principle

I believe you will stay away from the harmful mentality of chasing gains and cutting losses

And stable profits are not too far away