Source: thetokendispatch

Translation: Blockchain in Plain Language

A war is quietly unfolding in your pocket, and most people don't even notice.

The two major financial apps in the US—Robinhood and Coinbase—are conducting starkly contrasting experiments on millions of users. Robinhood ranks 14th in the App Store's finance category, while Coinbase ranks 20th, with both having a market capitalization of around $80 billion. They both target young investors but believe the other's approach is entirely wrong.

Both experiments have succeeded to some extent.

The essence of Robinhood vs. Coinbase

These two companies are not traditional competitors; they are conducting different experiments on the same subject (us).

Robinhood sees the pain points in finance and asks, 'What if we fix all the annoying parts?' They offer 15 cryptocurrencies, zero-commission trading, and an interface that allows you to buy Tesla stock without a finance degree. Their philosophy is: you don't need to know how sausages are made to enjoy a hot dog.

Coinbase, on the other hand, takes the opposite approach, asking, 'What if we rebuild the whole financial system on blockchain technology?' Coinbase charges higher fees than competitors like Robinhood, but it builds a platform for users who want comprehensive exposure to the crypto ecosystem, offering over 260 cryptocurrencies. They bet that traditional finance will eventually go on-chain and aim to become the infrastructure for that transformation.

Coinbase CEO Brian Armstrong stated: 'In the next 5 to 10 years, our goal is to become the leading financial services app globally because we believe cryptocurrencies are consuming financial services and we are the number one crypto company. All asset classes—money market funds, real estate, securities, debt—will be on-chain.'

The two companies went public just months apart in 2021, both with a market capitalization of $80 billion, targeting smartphone-first young investors, but their products seem designed for different species.

This is not a war for dominance, but a race to serve different financial futures.

The race for expanding crypto products

Both companies are accelerating the expansion of crypto products, but in very different ways.

Robinhood's recent announcement shows they are trying to directly surpass Coinbase. In June, they launched Robinhood Chain—its own Layer-2 network supporting tokenized stocks and crypto trading, with plans to support private assets like SpaceX and OpenAI in the future. European users can now trade tokenized US stocks around the clock, not just during market hours. This is the 24/7 trading model that crypto users expect, applied to traditional assets.

They also launched crypto staking for ETH and SOL, acquired Bitstamp, Europe's oldest crypto exchange (for $200 million), and plan to introduce crypto perpetual futures for European users. The crypto infrastructure they build seamlessly integrates with the existing stock trading experience rather than simply tacking on crypto features to traditional brokerage services.

All of this—chains, tokenized stocks, low fees—is designed for the next generation of investors, who will inherit trillions of dollars in wealth.

In the fee war, Robinhood's crypto trading fees are about 40 basis points (0.4%), while equivalent trades on Coinbase can reach 1.4% or higher. Buying $1,000 in Bitcoin, Robinhood charges about $4, while Coinbase charges over $14.

Robinhood profits through payment for order flow, where market makers pay for executing retail trades, similar to their stock trading model. This mature model allows them to offer 'free' trading while still making money.

But Coinbase offers functionalities that Robinhood cannot compete with: true ownership of cryptocurrencies. With Robinhood, you purchase a crypto 'receipt'; it’s merely a receipt for the crypto assets that Robinhood owes you. You cannot transfer Bitcoin to your own wallet or use it elsewhere—you can only buy and sell within the Robinhood app. You cannot participate in DeFi, stake most tokens, or use cryptocurrencies for purposes other than buying and selling.

For most people, it doesn't matter; they just want exposure to cryptocurrencies, not practicality. But for users looking to perform complex crypto operations, Coinbase is the only realistic choice among major platforms in the US.

Q2 earnings report analysis

This summer's earnings reports reveal the effectiveness of both approaches.

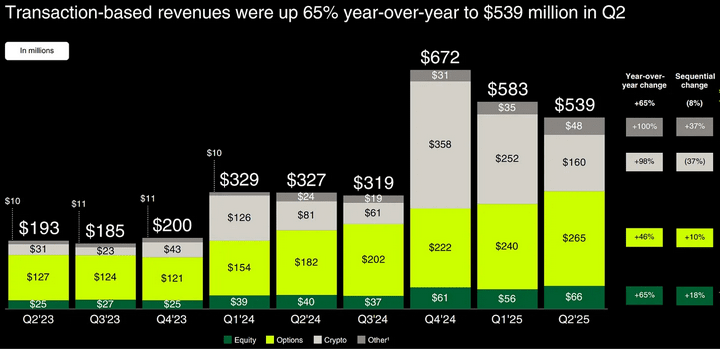

Robinhood has performed impressively. Total revenue grew 45% year-over-year to $989 million. Crypto revenue surged 98% to $160 million (increasing from 10% of total revenue last year to 16% this quarter), despite a relatively stable overall crypto market. They have 26.5 million active accounts, managing $279 billion in assets, representing a 99% year-over-year increase. The acquisition of Bitstamp added approximately 520,000 crypto users, with Bitstamp generating $7 billion in nominal crypto trading volume since the acquisition was completed in June.

Platform assets reached $279 billion, a 99% year-over-year increase, with net deposits at $13.8 billion. Active accounts grew by 10% to 26.5 million, and cash balances surged by 56% to $32.7 billion, indicating an increase in customers' wallet shares.

Coinbase, on the other hand, experienced a 'challenging quarter.' Total revenue fell 26% from Q1 to $1.5 billion, missing analyst expectations. Trading revenue declined 39%, due to a slump in retail trading. Stock prices dropped 16% on earnings report day as investors tried to determine whether this was a temporary downturn or a sign of a high-cost model.

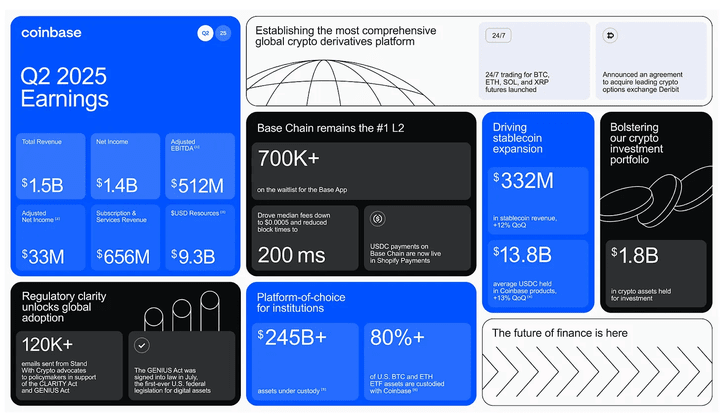

But calling this quarter a failure overlooks the bigger picture. Coinbase achieved $1.4 billion in net revenue, exceeding $512 million in adjusted EBITDA, primarily due to $1.5 billion in unrealized gains from portfolio and strategic crypto asset holdings. Even excluding these one-time gains, adjusted net income still showed $33 million, indicating actual profitability.

Increased operating expenses were primarily due to a $307 million one-time loss from a data breach in May. Core costs (technology, administration, marketing) actually decreased, demonstrating cost control capabilities. USDC stablecoin business revenue reached $332 million, with average balances growing by 13%. Custodial assets hit a record high of $245.7 billion. Prime Financing (institutional financing) balances also reached new highs, as part of Coinbase Prime, which provides custodial, trading, lending, and financing services to hedge funds and family offices.

Coinbase continues to launch new products: new derivatives, expanding the Base chain, and introducing the Coinbase One Card. Despite declining revenues, the foundation remains solid.

Coinbase's infrastructure empire

Coinbase's infrastructure strategy is more complex. They provide custodial services for $245.7 billion in assets, capturing a large share of the institutional crypto market. When you buy a Bitcoin ETF through a 401k, it’s likely that you are using Coinbase's infrastructure.

Coinbase is the primary custodian for over 80% of Bitcoin and Ethereum ETFs in the US, managing about $113.4 billion (out of a total crypto ETF asset pool of $140 billion). When BlackRock's IBIT or Fidelity's FBTC needs to store billions of dollars in Bitcoin, they turn to Coinbase. PayPal's launch of PYUSD stablecoin or JPMorgan's need for a crypto payment rail also relies on Coinbase's backend.

Coinbase has over 240 institutional clients, 420 liquidity providers, and regulatory licenses that most competitors cannot match. Its custodial business is licensed by the New York State Department of Financial Services, a regulatory approval that takes years to acquire and is hard for competitors to replicate.

Their 'all-in-one exchange' strategy is beginning to show results. They launched perpetual futures with up to 10x leverage, bringing derivatives trading that was previously only available on overseas exchanges to US retail users. They are directly integrating decentralized exchanges into the app, allowing users to trade Ethereum or any token on Base without leaving Coinbase.

Its Base Layer-2 network processes over 54,000 token issuances daily, surpassing Solana. The real highlight of Base lies in its integration with Coinbase's other businesses: ETF providers can use it for instant settlement, companies can directly tokenize assets, and retail users can access institutional-grade infrastructure.

The generational takeover by Robinhood

Coinbase builds infrastructure for institutions, while Robinhood executes the smartest long-term strategy in finance: capturing young people before they become wealthy.

A similar strategy brought success to Disney. In the early 20th century, Disney captured children's hearts through animation and theme parks, establishing emotional ties before they had money. When these kids grew up and started earning, their loyalty translated into spending on movies, merchandise, streaming, and vacations, creating a multi-generational cash machine.

Robinhood dominates among young investors, and traditional brokers should be concerned:

About 50% of customers are millennials, 25% are Gen Z, and 20% are Gen X.

Robinhood users typically start investing at ages 19-22, much younger than other platforms, where millennials start in their 20s and baby boomers in their 30s.

Robinhood guides new users quickly through their first sell order, not to encourage frequent trading, but because locking in actual gains (even just $50) creates an emotional hook that keeps users coming back.

Their 'all-financial' expansion aligns with this logic. Robinhood Gold ($5 per month subscription) includes a 3% cash back credit card, high-yield savings, retirement matching, and margin discounts. Gold subscribers increased by 60% year-over-year to 2 million. These users are using Robinhood for banking, credit cards, and retirement.

The platform currently holds $279 billion in assets, targeting the massive wealth transfer of $84-124 trillion from the baby boomer generation to younger generations over the next 20 years. Robinhood bets that if they can establish user habits early, they don’t need to predict wealth inheritance patterns; they just need to secure a place when the wealth arrives.

Who is winning?

The market capitalizations of the two companies are close: Robinhood at $81 billion and Coinbase at $85 billion. In terms of performance this year, Robinhood is up 135%, while Coinbase is only up 30%, with much of that coming in the last month.

Bank of America analyst Craig Siegenthaler recently raised Robinhood's target price to $119 while lowering Coinbase's from $383 to $369, citing: 'Robinhood's crypto revenue surge, while Coinbase is too reliant on retail users abandoning volatile altcoin trading.'

Coinbase's global market share fell from 5.65% to 4.56%, with a slight rebound in July, while Kraken's market share in the US grew the most this year. Coinbase faces a dilemma: lowering fees harms profit margins, or maintaining high fees risks losing traders. They chose to prioritize margins, adding fees to previously free stablecoin trades, whereas Robinhood's rates are about 50% lower.

Mizuho reaffirmed a target price of $120 after meeting with Robinhood CEO Vlad Tenev, praising its crypto resilience and aggressive push for tokenized stocks. They stated: 'European tokenized stock opportunities, expansion to upstream and youth markets, 15% of net deposits from competitors, focus on NPS and execution, and inelastic crypto pricing are all impressive.'

But Coinbase has institutional credibility. While other exchanges compete on trading fees, Coinbase builds relationships with institutions that will determine the integration of crypto and traditional finance over the next decade.

Neither company will disappear. They cater to different user needs, both of which are growing. This is not a winner-takes-all competition, but rather market segmentation—Robinhood targets mainstream finance while Coinbase focuses on crypto infrastructure.

This reveals two competing theories about how people will interact with money in the future:

Robinhood believes the future of finance will be 'invisible,' abstract, simple, and integrated into lifestyle apps, making finance a part of the environment.

Coinbase, on the other hand, bets on winning trust through architecture.

There are no right or wrong answers; it's just different goals. One side pursues simplicity and trust, while the other builds the underlying architecture.