The two leading financial apps in the U.S. are conducting completely opposite experiments on millions of users.

Robinhood and Coinbase represent two distinctly different bets on what people want from money applications. Robinhood ranks 14th in the financial category of the App Store, while Coinbase ranks 20th, with both having a market cap of around $80 billion.

Both are chasing the same young investors, both believe the other is doing it wrong.

A bet on people wanting finance to operate like other apps on their phones: simple, intuitive, and invisible. Coinbase has built the infrastructure for the transition from traditional finance to blockchain-based systems.

Both experiments have succeeded to some extent.

01

The essence of Robinhood versus Coinbase

The key for Robinhood and Coinbase is: they are not competitors in the traditional sense; they are conducting completely different experiments on the same subjects (us).

Robinhood examines finance and asks, "What if we fix all the annoying parts?" They offer 15 cryptocurrencies, zero-commission trading, and an interface that makes you feel like you can buy Tesla stock without a finance degree. Their pitch is that you don't need to understand how sausages are made to enjoy a hot dog.

Coinbase is going in the opposite direction. They say, "What if we rebuild all finance on blockchain technology?" Coinbase's fees are higher than competitors like Robinhood, but its platform is built for those who want access to the full crypto ecosystem, offering over 260 cryptocurrencies.

They bet that traditional finance will eventually shift on-chain, and they want to be the infrastructure driving that transformation.

"In five to ten years, our goal is to be the number one player in global financial services applications, targeting these customer segments, because we believe crypto is eating financial services and we are the number one crypto company," said CEO Brian Armstrong. "All these asset classes — money market funds, real estate, securities, debt — will go on-chain."

Both companies went public a few months apart in 2021, with both having a market capitalization of around $80 billion and targeting the same generation of mobile-first investors. But they may be building products for different species.

They are solving different problems for different users. This makes it more of a race to serve a differentiated financial future rather than a war for supremacy?

02

The race for crypto product expansion

Both companies are racing to expand their crypto products, but their approaches are completely different.

Robinhood's recent crypto announcement shows they are trying to completely outpace Coinbase. In June, they announced Robinhood Chain, their own layer-2 network that will support tokenized stocks, crypto trading, and eventually support private market assets like SpaceX and OpenAI stock.

European users can now trade tokenized versions of U.S. stocks around the clock, not just during market hours. This is the 24/7 trading that crypto users expect, applied to traditional assets.

They also launched crypto staking for ETH and SOL, acquired Bitstamp (the oldest crypto exchange in Europe) for $200 million, and plan to launch crypto perpetual futures for European users. They are building a crypto infrastructure that feels native to the existing stock trading experience, rather than tethering crypto to traditional brokerage.

That’s why all of this — chains, tokenized stocks, low fees — feels naturally designed for the next generation of investors who will inherit trillions.

In the fee war, Robinhood charges around 40 basis points (0.4%) for crypto trades. Coinbase may charge 1.4% or more for the same transaction. If you buy $1,000 worth of Bitcoin, it costs $4 on Robinhood and over $14 on Coinbase.

Robinhood achieves this through payment for order flow, where market makers pay them for the right to execute retail trades, just as they do for stock trades. This is a proven model that allows them to offer "free" trading while still making money.

But Coinbase offers what Robinhood cannot: actual crypto ownership. On Robinhood, you buy a crypto IOU, which is essentially a receipt that Robinhood owes you that amount of crypto. This means you cannot transfer Bitcoin to your own wallet or use it elsewhere. You can only buy and sell it within the Robinhood app.

You can't participate in DeFi, you can't stake most tokens, and you can't actually use crypto for anything other than buying and selling.

For most people, this doesn't matter; they want crypto exposure rather than crypto utility. But for anyone wanting to do anything slightly complex with crypto, Coinbase is the only realistic choice among the major U.S. platforms.

03

Q2 earnings analysis

This summer's earnings revealed a lot about which approach is currently effective.

Robinhood crushed their quarter, with total revenue up 45% year-over-year to $989 million. Their crypto revenue exploded by 98% to $160 million (growing from about 10% of total revenue last year to 16% this quarter), despite the overall crypto market remaining relatively stable. They now have 26.5 million funded accounts, holding $279 billion in total assets, a 99% increase from last year.

Plus, the approximately 520,000 new crypto users added through the Bitstamp acquisition, along with the $7 billion nominal crypto trading volume generated after the Bitstamp acquisition is completed in June 2025.

The company held $279 billion in platform assets at the end of the quarter, a 99% increase from the previous year, along with $13.8 billion in net deposits. Fund accounts grew 10% to $26.5 million, while cash sweep balances surged 56% to $32.7 billion, indicating a stronger wallet share for each customer.

@robinhood

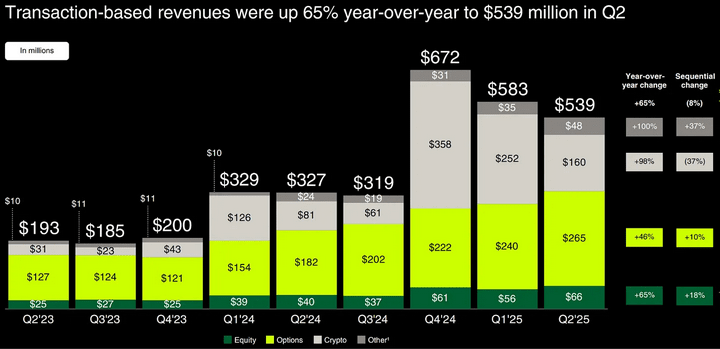

Meanwhile, Coinbase experienced what polite people would call a "challenging quarter."

Total revenue fell 26% from Q1 to $1.5 billion, below analyst expectations, with trading revenue down 39% due to retail trading exhaustion. Stocks fell 16% on earnings day as investors tried to figure out whether this was a temporary fluctuation or a sign that people really don't want to pay high fees for complexity.

"We still see their growth facing long-term risks due to above-average retail trading costs and increasing competition from platforms like Robinhood," said Arca analyst Alex Woodard. "Coinbase needs to implement cheaper trading fees and continue to expand its product offerings through M&A to avoid losing market share."

@coinbase

But to call this quarter a failure overlooks the bigger picture.

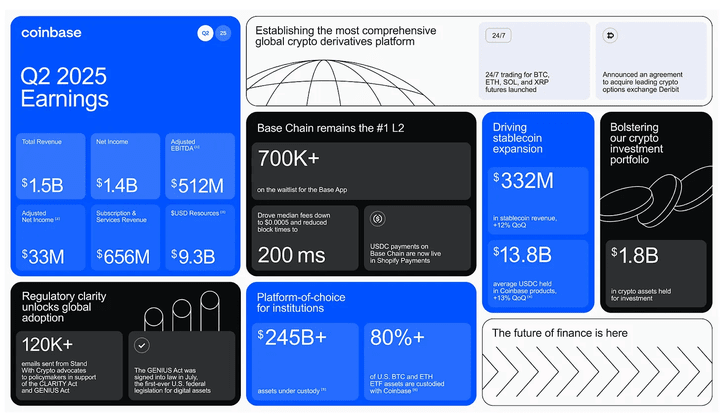

Coinbase reported $1.4 billion in net income, actually exceeding their adjusted EBITDA of $512 million due to $1.5 billion in unrealized gains from portfolio and strategic crypto holdings. These paper gains will push net income far above their core operational performance.

Even excluding these one-time windfalls, adjusted net income is still a solid $33 million, showing actual profitability in a weak quarter.

Underneath the surface, there are many things to like; operating expenses are up, but mainly due to a one-time $307 million hit from the data breach in May. Core costs — such as technology, administration, and marketing — have actually decreased, showing real cost control, and their USDC business continues to hum along, with stablecoin revenue reaching $332 million, thanks to a 13% increase in average balances and custody assets hitting a record high of $245.7 billion.

Prime Financing balances also reached record levels. This is part of Coinbase Prime, their institutional service, operating like traditional prime brokerage — they provide custody, trading, lending, and financing services to hedge funds, family offices, and other large crypto investors. Prime Financing specifically refers to margin lending, with institutions able to borrow against their crypto holdings for additional trading or investment.

Coinbase continues to deliver: launching new derivatives products, growing their Base chain, and launching Coinbase One Card. So yes, revenue is down, but the fundamentals look stronger than ever.

04

Coinbase's infrastructure empire

But Coinbase's infrastructure play is more complex than it seems on the surface.

Coinbase holds $245.7 billion for institutions — a record high, representing a significant portion of the entire institutional crypto market. When you buy a Bitcoin ETF through a 401k, you are probably using Coinbase's infrastructure.

Coinbase is the primary custodian for over 80% of all Bitcoin and Ethereum ETFs in the U.S., controlling about $113.4 billion of approximately $140 billion in total crypto ETF assets. When BlackRock’s IBIT or Fidelity’s FBTC need to store tens of billions of dollars in Bitcoin, they call Coinbase. When PayPal wants to launch the PYUSD stablecoin or when JPMorgan needs a crypto payment rail, they use Coinbase's backend.

Coinbase has over 240 institutional clients, 420+ liquidity providers, and regulatory licenses that most competitors cannot match. Their custody division is chartered by the New York State Department of Financial Services, a regulatory approval that took years to obtain and will take competitors years to replicate.

Their "everything exchange" strategy is starting to show results beyond custody. They just launched perpetual futures with up to 10x leverage, bringing derivatives trading previously only available on offshore exchanges to U.S. retail traders. They are integrating decentralized exchanges directly into their app so you can trade Ethereum or any token on Base without leaving Coinbase.

Their Base layer-2 network processed over 54,000 token launches in a single day, beating Solana. But the real genius lies in how Base integrates with everything Coinbase does; ETF providers can use Base for instant settlement, companies can tokenize assets directly on the network, and retail users can access the infrastructure that drives billions of dollars in institutional investment.

05

The generational takeover of Robinhood

While Coinbase builds infrastructure for institutions, Robinhood is executing potentially the smartest long-term play in finance: capturing an entire generation before they get wealthy.

A similar strategy worked well for Disney, building its empire by capturing the hearts of children in the early 20th century when they had no wallets. From cartoons to theme parks, Disney became part of childhood itself. When those kids grew up and began making money, they brought loyalty that turned early emotional ties into multi-generational cash machines.

Robinhood dominates among young investors in a way that should worry traditional brokers.

About 50% of Robinhood customers are millennials, about 25% are Gen Z, and 20% are Gen X.

The average Robinhood user starts investing at ages 19-22, compared to those in their 20s on other platforms and those in their 30s in the baby boomer generation.

Robinhood even guides new users quickly to their first sell action, not because they want people to trade constantly, but because locking in actual gains creates an emotional hook that brings users back. Once someone makes real money on the platform, even if just $50, they are psychologically invested, making it hard to break away.

Their expansion into everything finance makes sense in this context.

Robinhood Gold, their $5 monthly subscription, bundles a credit card with 3% cash back, high-yield savings, retirement matching, and margin discounts. Gold subscribers grew 60% year-over-year to 2 million users, who use Robinhood for banking, cards, and retirement.

The platform now holds $279 billion in custody assets, seeking a share of the "great wealth transfer" involving $84-124 trillion in assets to be transferred from the baby boomer generation to younger generations over the next 20 years.

In the next twenty years, this wealth will be passed from the baby boomer generation to younger generations, and no one knows exactly who will get what or when. But Robinhood bets that if you build habits early, you don't need to predict inheritance patterns; you just need to be there when the money appears.

06

So, who is actually winning?

Both stocks have similar market capitalizations, with Robinhood at $81 billion and Coinbase at $85 billion. In their year-to-date performance, Robinhood is up 135%, while Coinbase is only up 30%, much of which came last month.

U.S. Bank analyst Craig Siegenthaler recently raised his price target for Robinhood to $119, while lowering Coinbase from $383 to $369, citing: "Robinhood's crypto revenue is exploding, while Coinbase is overly reliant on retail users abandoning volatile altcoin trading."

Coinbase's global market share fell from 5.65% to 4.56%, then saw a slight recovery in July, while Kraken recorded the largest gain in U.S. market share this year. Coinbase faces the classic dilemma: lower prices hurt margins or stick to them and risk losing traders. They chose margins, charging for previously free stablecoin trades, while Robinhood's rates remain about 50% lower.

Mizuho just reaffirmed its $120 price target for Robinhood after meeting with CEO Vlad Tenev, citing the company's crypto resilience and positive push for tokenized stocks.

"We are particularly impressed by the opportunity for tokenized stocks in Europe, moving to the high-end market, and potentially moving to teenagers, with 15% of net deposits coming from competitors, focusing on NPS/execution as key growth drivers, and crypto prices being inelastic," the analyst said.

But Coinbase has institutional credibility, while other exchanges compete on trading fees; Coinbase is building relationships with institutions that will decide how crypto integrates with traditional finance over the next decade.

07

Summary

Neither company is going away; they serve genuinely different user needs, and both needs are growing. This looks more like market segmentation than winner-takes-all competition — Robinhood for mainstream finance and Coinbase for crypto infrastructure.

This is a glimpse into two competing theories of how people will interact with money in the future.

One theory suggests the future of finance will be invisible, abstract, easy, built into applications that feel more like lifestyle products than brokerage; finance becomes ambient, and that is Robinhood’s worldview.

Neither is right or wrong. They are just targeting different ends of the spectrum. One is trying to win trust through simplicity, the other through architecture.