01 Ethereum's tenth anniversary

(Ethereum still has 100 times the growth potential)

(A decade of the world computer's itch)

(The risk dilemma behind the Ethereum treasury)

02 Regulatory trends

(Hong Kong's stablecoin regulation is about to take effect, and the licensing competition has begun)

(SEC new standards announced, is a wave of spot ETF approvals about to unfold?)

(Full text of SEC Chairman's speech on the 'Crypto Project')

(The power games behind stablecoins)

(Under a $4 trillion market value: dissecting the funding dynamics of the cryptocurrency market)

03 The wave of U.S. stock tokenization

(How to make U.S. stocks great again?)

(In Q2, net profit of $386 million, Robinhood made a fortune from 'trading coins')

(Robinhood's crypto ambitions: to become the 'only financial entry point' for the younger generation)

(The tokenized stock market size is expected to grow 2600 times, who will benefit?)

01 Ethereum's tenth anniversary

On July 30, Ethereum celebrated its tenth anniversary, with a market value growth of 3600 times to $450 billion over the past decade, becoming one of the top thirty assets globally, nurturing epoch-making products such as stablecoins and DAOs. This article analyzes whether it can achieve another hundredfold growth in the future. Recommended article:

(Ethereum still has 100 times the growth potential)

Looking back over ten years, Ethereum's ecosystem has at least given birth to three epoch-making products, just like Apple's launch of the Mac, iPhone, AirPods, and iPad; Ethereum is also the absolute market leader among them.

Stablecoins have a yearly trading volume of $28 trillion, with over 70% of the trading volume occurring on Ethereum; in 2016, the world's first DAO was born on Ethereum, and today, over 90% of the global TVL (Total Value Locked) largest DAOs are within the Ethereum ecosystem; during the summer of 2020's DeFi, Ethereum was the only center, with a market share of 95%-99%; in 2021, NFTs broke out on a large scale for the first time, with Ethereum as the main battleground, accounting for over 90% of annual trading volume... Meanwhile, U.S. stock tokenization, U.S. treasury tokenization, RWA, AI Agent memes, etc., are only just beginning.

What about ten years later? Ethereum is now an asset ranked in the top 30 globally, surpassing famous companies like Meta, TSMC, Visa, and Mastercard. Is this its endpoint?

No, this may actually be the true starting point.

Ten years ago, it ignited the imagination of decentralization with a white paper. Ten years later, it remains at the core of the crypto world, but is no longer the only stage. Recommended article:

(A decade of the world computer's itch)

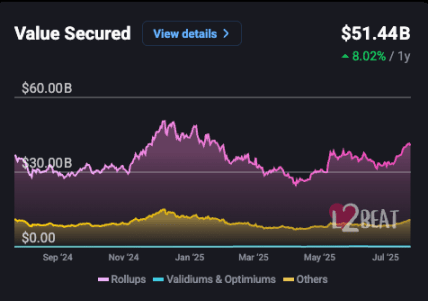

The Rollup-centric approach that Ethereum has embraced in recent years alleviates pressure on the main chain while causing a large volume of transactions and value to remain on Layer 2 networks, failing to flow back to the mainnet. A report from Standard Chartered Bank at the beginning of 2025 explicitly stated that the rise of Layer 2 networks has eroded the value capture of the Ethereum main chain. The report estimated that just the leading Ethereum Layer 2, Base, launched by Coinbase, has 'taken away' about $50 billion of Ethereum ecosystem market value.

Recently, news of PayPal co-founder Peter Thiel investing in Ethereum mining company BitMine shook the market. Meanwhile, several companies continue to increase their holdings in Ethereum. Wall Street investment bank Bernstein pointed out that Ethereum treasuries face liquidity and security risks when staking for yield, and companies need to balance this cautiously, a situation that has garnered attention from all sectors. Recommended article:

(The risk dilemma behind the Ethereum treasury)

Analysts pointed out: 'If the Ethereum treasury stakes ETH for yield, staking contracts usually have liquidity, but sometimes unlocking requires waiting several days. Therefore, Ethereum treasury companies must find a balance between ETH liquidity and yield optimization. Additionally, more complex yield optimization strategies such as restaking (e.g. Eigenlayer restaking model) and DeFi-based yield generation need to address security risk management issues related to smart contracts.'

Bernstein added: 'The advantage of the Ethereum treasury model is that staking yields can provide real cash flow for operations, but liquidity risks and security issues still need to be a focus of attention.'

02 Regulatory trends

On August 1, the Hong Kong (Stablecoin Regulation Draft) officially took effect. The licensing competition has long since begun. Recommended article:

(Hong Kong's stablecoin regulation is about to take effect, and the licensing competition has begun)

It is worth noting that the Monetary Authority has repeatedly pointed out that the core of determining whether to grant a license is not limited to the level of asset reserves, but rather depends on whether the applicant's stablecoin business model has practical application scenarios and sustainability. In this regard, the regulatory side maintains a tone of 'strict first, lenient later', cautiously maintaining the licensing rhythm in the initial stages of the system to prevent market bubbles and conceptual speculation, emphasizing the long-term sustainable development of Hong Kong's digital asset ecosystem.

Deeper changes are underway, and U.S. regulation is gradually becoming more in-depth. On July 29, the U.S. Securities and Exchange Commission (SEC) announced the approval of the physical creation and redemption mechanism for crypto asset exchange-traded products (ETPs). Previously, crypto ETPs primarily adopted cash creation and redemption models. This change significantly reduces transaction costs and increases efficiency. Recommended article:

(SEC new standards announced, is a wave of spot ETF approvals about to unfold?)

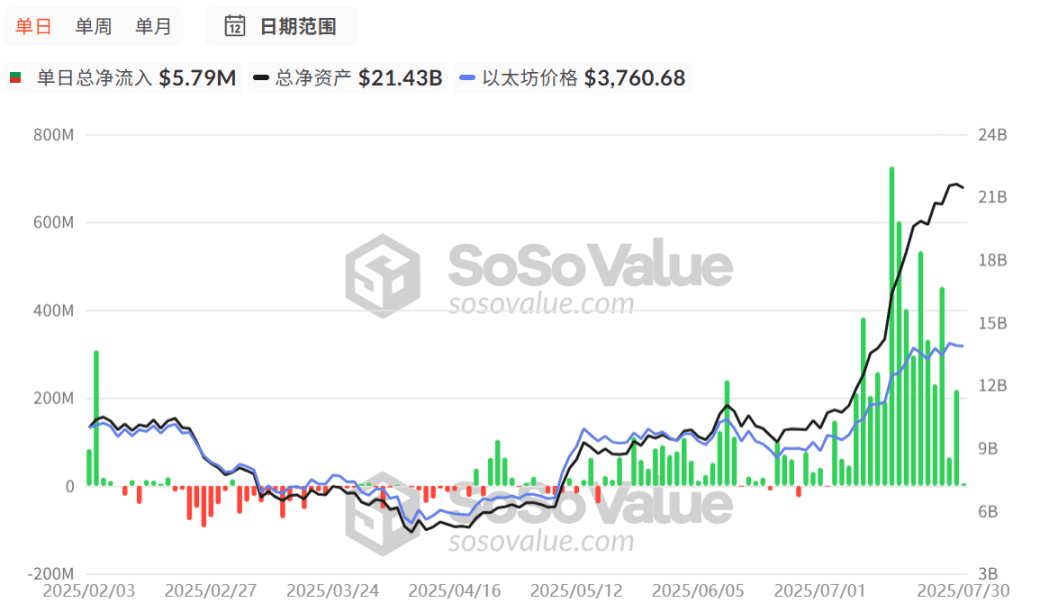

According to SoSoValue data, as of July 31, 2025, the total net inflow of U.S. Bitcoin spot ETFs has reached $55.11 billion. The U.S. Ethereum spot ETF has achieved a total net inflow of $9.62 billion, and after breaking free from a sluggish period, is experiencing rapid growth. The approval of spot ETFs undoubtedly has a good effect on supporting the price increase.

On July 31, the SEC Chairman announced the 'Crypto Project', aimed at making the U.S. the 'global crypto capital'. This initiative will modernize securities regulations, assist in the full on-chain migration of financial markets, attract crypto companies back, and lead the digital asset revolution. Let's take a look at SEC Chairman Paul S. Atkins' speech:

(Full text of SEC Chairman's speech on the 'Crypto Project')

Today, I want to discuss what Commissioner Hester Peirce and I refer to as 'Project Crypto', which will become the North Star for the SEC in its historic effort to help President Trump make the United States the 'global crypto capital'. But before discussing our plans for dominance in the crypto market, I want to revisit some turning points in the history of capital market development, as they are quite similar to the juncture we are at now, and the future we shape should be worthy of the legacy we inherit.

Cryptocurrency, once seen as a 'revolution to disrupt traditional finance', has ultimately not taken the path of violent confrontation, but has instead deeply bound itself with the regulatory system and political consensus, becoming a 'tamed revolution'. From impacting tradition to seeking permission, from decentralization ideals to centralized regulatory realities, the absurdity and contradictions of this 'revolution' are the core of this article's analysis. When rebels bow to the system, is it a game of interests behind it, or an inevitability of the times? Recommended article:

(The power games behind stablecoins)

(The GENIUS Act) is the most ingenious diplomatic maneuver, yet disguised as domestic financial regulation.

This raises some interesting questions: What will happen when the entire crypto ecosystem becomes an appendage of U.S. monetary policy? Are we building a more decentralized financial system or creating the world's most complex dollar distribution network? If 99% of stablecoins are pegged to the dollar, meaningful innovation requires approval from U.S. monetary regulators, have we inadvertently turned revolutionary technology into the ultimate export business for fiat currency? If the rebellious energy of cryptocurrency is directed towards enhancing the efficiency of the existing monetary system rather than replacing it, as long as payments and settlements are faster, everyone can make money, does anyone really care? These may not be questions, but rather a far cry from the problems people wanted to solve when this movement began.

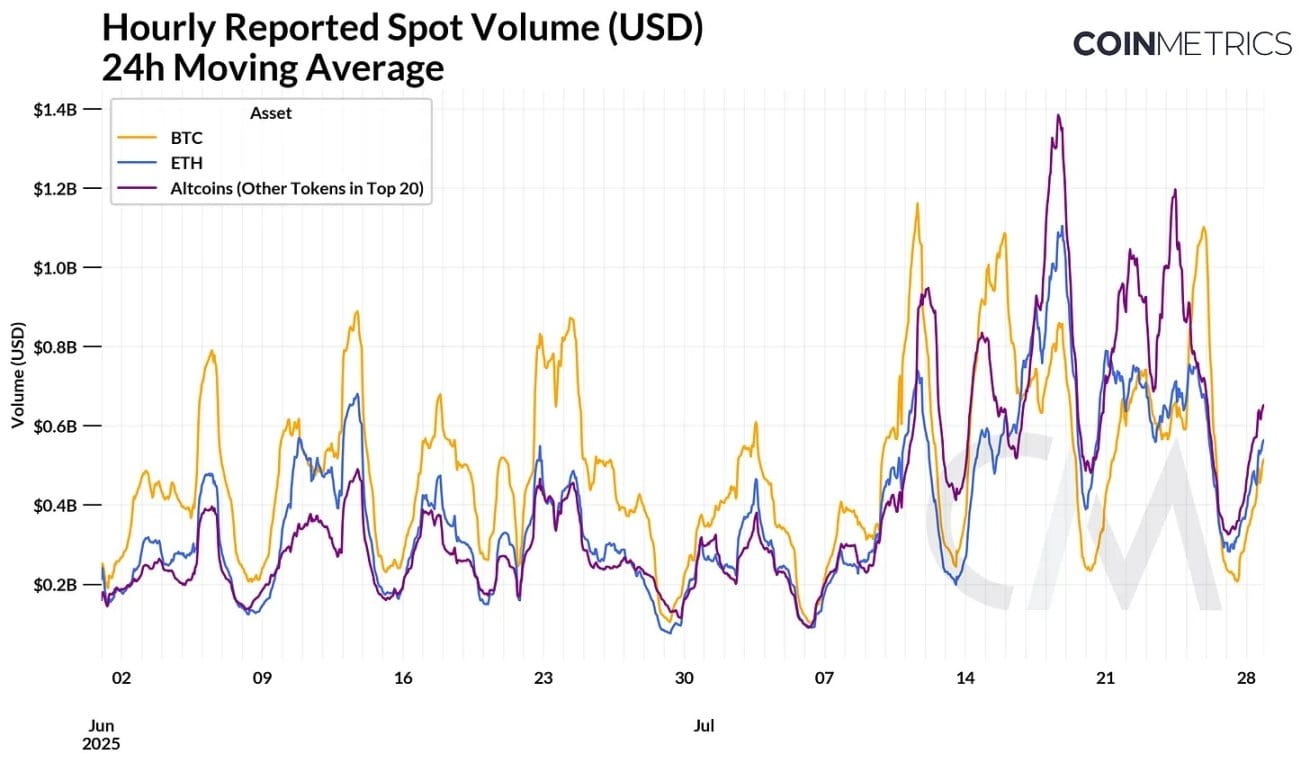

The digital asset market has approached the $4 trillion mark for the first time, marking an important milestone in the industry's development. This latest surge is driven by a combination of structural and cyclical factors, including continued inflows into Bitcoin and Ethereum spot ETFs, accelerated accumulation by digital asset fund management companies, and significant regulatory breakthroughs such as the passage of the (GENIUS Act). Recommended article:

(Under a $4 trillion market value: dissecting the funding dynamics of the cryptocurrency market)

Recent market dynamics indicate that we may be in the early stages of an expanded market dominance pattern. Ethereum has begun to show relative strength, with the ETH/BTC exchange rate rebounding 73% since May, and ETH price breaking through $3,900. This momentum is attributed to record ETF inflows, increased adoption rates of corporate capital reserves, and Ethereum's sustained dominance in the stablecoin field, making it a beneficiary of the (GENIUS Act).

03 The wave of U.S. stock tokenization

What would happen if purchasing such assets no longer required an account, and was not limited by region or trading time? Just with a mobile phone and a balance in a crypto wallet, one can buy 'stocks' of U.S. giants anytime and anywhere; this is no longer a fictional scenario, but a reality brought about by 'U.S. stock tokenization'. Recommended article:

(How to make U.S. stocks great again?)

So why is the wave of tokenization flooding into U.S. stocks?

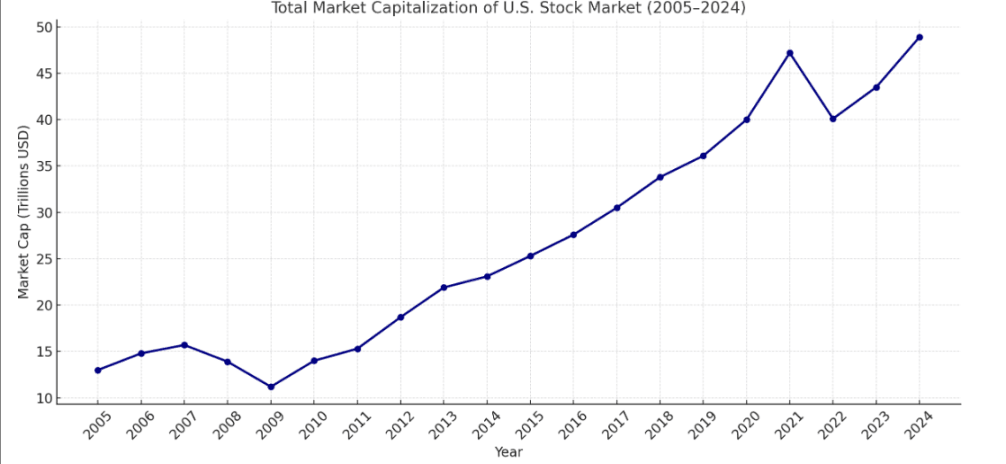

U.S. stocks have unique advantages not found in other assets. First, as the largest stock market in the world, the total market value of U.S. stocks reached between $52 trillion and $59 trillion by 2025, far surpassing the stock markets of other countries or regions. The total global stock market value is about $124 trillion, with U.S. stocks accounting for more than 40%.

The tokenized stock market currently stands at $500 million; if 1% of the global stocks are tokenized, it could reach $13.4 trillion by 2030, an increase of 2,680 times. By 2025, regulatory and infrastructural maturity will become driving forces, and its unique advantage lies in the integration with DeFi, where multiple participants are positioning themselves in this field.

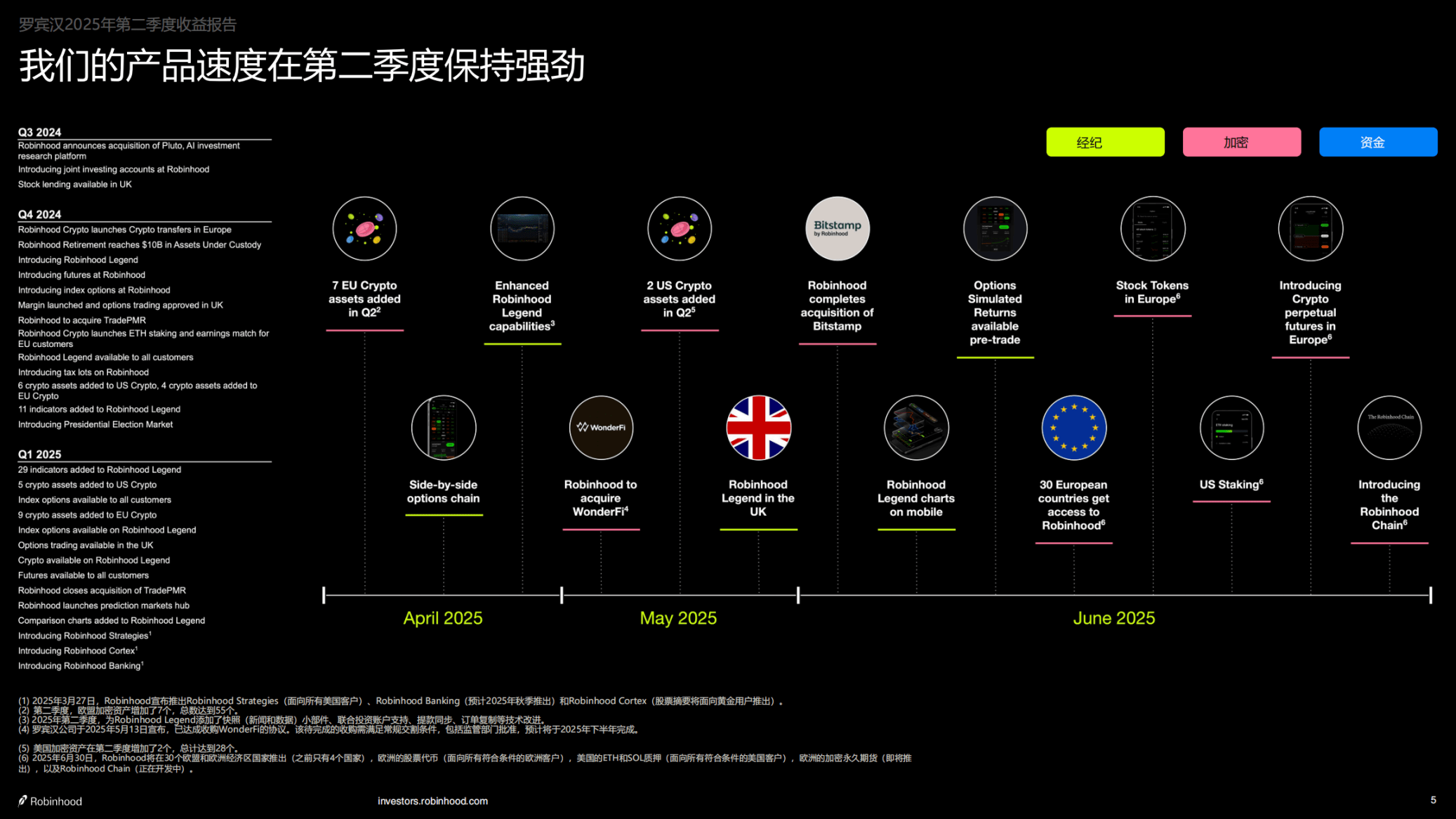

(In Q2, net profit of $386 million, Robinhood made a fortune from 'trading coins')

On the product level, Robinhood continues to iterate in the crypto sector. In Q2 2025, the company expanded its service range to 30 European countries, far exceeding the 4 countries from the same period last year. Robinhood has also launched 'stock tokens', allowing users to trade token versions of over 200 U.S. stocks and ETFs in Europe. In the U.S. market, the company has launched staking services for ETH and SOL, and plans to introduce crypto perpetual contracts.

Robinhood rises strongly with its cryptocurrency business, hitting new highs in stock price with a market capitalization of nearly $98 billion. Its layout includes stock tokens, crypto staking, and acquisitions of exchanges to expand its market, aiming to be the 'only financial entry point' for the younger generation, revealing a glimpse of its ambitions. Recommended article:

(Robinhood's crypto ambitions: to become the 'only financial entry point' for the younger generation)

Tokenization may be Robinhood's long-term goal, but its core crypto business is already a powerful force. In 2024, Robinhood's crypto-related revenue reached $626 million, a significant increase from $135 million the previous year, accounting for more than one-third of total trading revenue. In Q1 2025, crypto-related revenue reached $252 million. 'They are currently capturing market share from Coinbase in the U.S.,' says Rob Hadick, a general partner at crypto venture firm Dragonfly. Cantor Fitzgerald's Knoblauch pointed out that in May 2025, Robinhood's crypto trading volume surged by 36% month-over-month, while Coinbase saw a decline. He acknowledged that Coinbase still occupies the institutional market, 'their services are broader and they have custody services,' but after Robinhood's acquisition of Bitstamp in June, it gained 5,000 institutional accounts and licenses in Europe and Asia.

The tokenized stock market currently has a scale of $500 million. If 1% of global stocks are tokenized, it could reach $13.4 trillion by 2030, an increase of 2,680 times. By 2025, regulatory and infrastructure maturity will become a driving force, and its unique advantage lies in its integration with DeFi, with multiple participants strategically positioning themselves in this field.