In August 2023, MakerDAO's ecological lending protocol Spark offered an 8% annual yield on $DAI, and then Sun entered in batches, accumulating an investment of 230,000 $stETH, which accounted for over 15% of Spark's deposit amount, forcing MakerDAO to urgently propose lowering the interest rate to 5%.

MakerDAO's original intention was to 'subsidize' the usage rate of $DAI, but it almost turned into Sun Yuchen's Solo Yield.

In July 2025, Ethena played with the treasury strategy of 'coin - stock - debt', rapidly raising the APY of $sUSDe to around 12%, with $ENA surging by 20% in a single day.

As a treasury strategy originating from the BTC ecosystem, it brushed past $SBET/$BMNR, ultimately landing on USDe.

Ethena once again leverages the capital market, successfully creating a dual flywheel of $ENA and $USDe in the on-chain market and stock market.

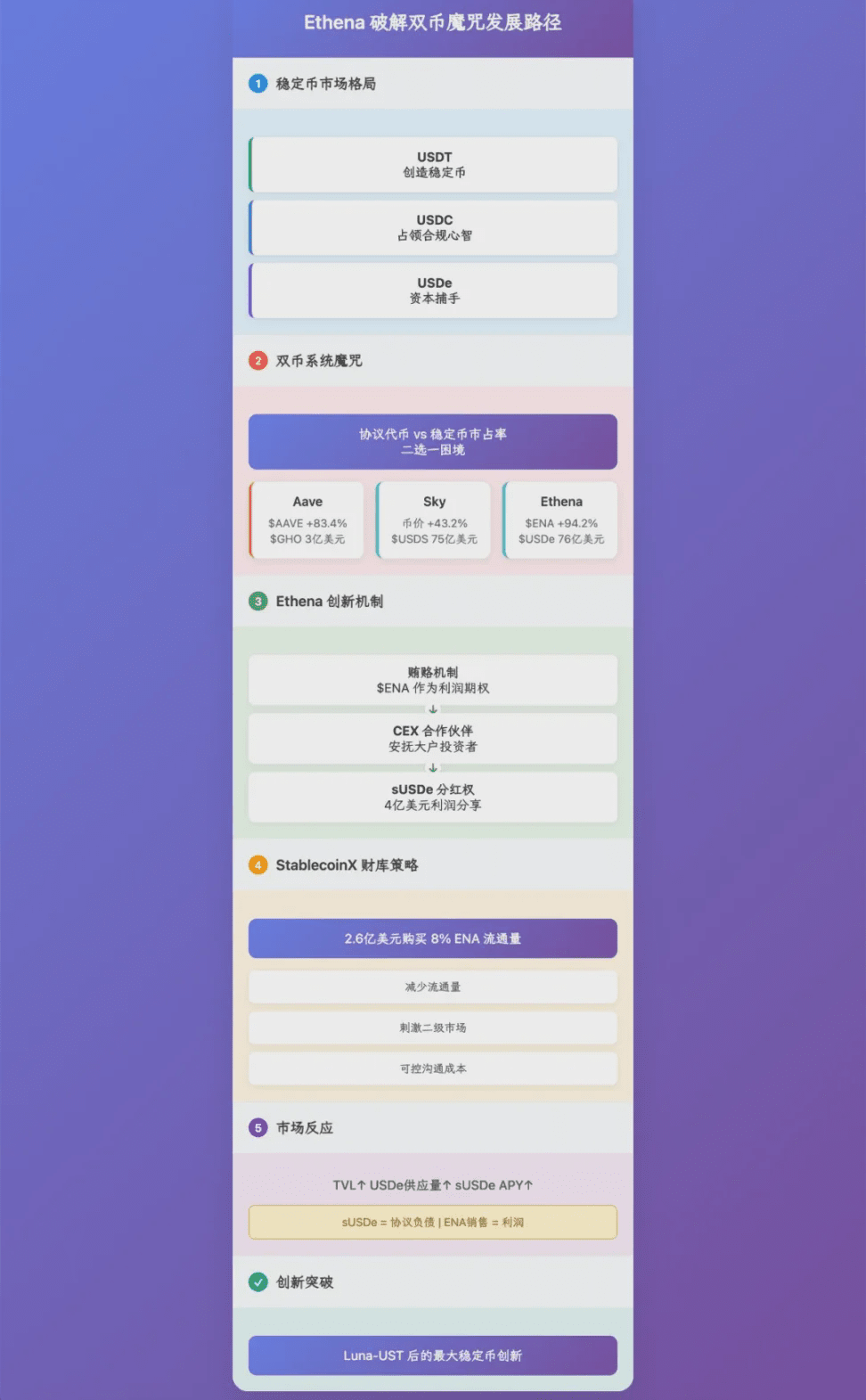

The great escape of the dual-token system.

USDT created stablecoins, USDC occupied users' compliance mindset, and USDe is a capital catcher.

Image description: The path of Ethena's capitalization.

When the $ENA treasury strategy was launched, I instinctively thought it was a simple imitation of the current Strategy trend, but upon careful review, Ethena is actually attempting to break the 'dual token' system curse.

The curse is that on-chain stablecoin issuers must choose between the protocol token price and stablecoin market share.

Aave chose to empower $AAVE with a 83.4% price increase in three months, but the issuance of $GHO is only 300 million dollars.

MakerDAO evolved into Sky, with a 43.2% price increase in three months, and $USDS issuance of 7.5 billion dollars.

Ethena token ENA saw a 94.2% price increase in three months, with $USDe issuance of 7.6 billion dollars.

Adding to the collapse of the Luna-UST dual-token system, maintaining balance between the two becomes incredibly difficult; the root cause is limited protocol income, which diverts to market share, leading to price instability for the tokens, and vice versa.

In the entire stablecoin market, this is the entry barrier set by USDT. USDT invented the stablecoin track, so it naturally doesn't need to worry. Circle needs to share profits with partners, but still won't share with USDC holders.

Ethena uses a bribery mechanism to share ENA as profit 'options' with CEX partners, temporarily soothing large holders, investors, and CEX, while prioritizing the protection of USDe holders' dividend rights.

According to A1 Research's calculations, Ethena has shared approximately 400 million dollars in profits with USDe holders in the form of sUSDe since its establishment, breaking through the entry barriers set by USDT/USDC.

Ethena not only surpassed Sky in stablecoin market share (not counting the residual share of DAI), but also outperformed Aave in the performance of its main token project, which is not coincidental.

The price increase of Ethena's ENA, while influenced by Upbit's stimulation, is also due to Ethena deeply reforming the value transfer method of the dual-token system by introducing stock market treasury strategies.

Returning to the previous question, prioritizing the protection of USDe's market share, ENA's dividend rights still need to be realized. Ethena's choice is to imitate treasury strategies to launch StablecoinX, but to modify it.

BTC treasury strategy, taking Strategy as an example, bets on the long-term upward trend of BTC prices. Holding 600,000 BTC is a catalyst for price increase and also hell during a downturn.

ETH treasury strategy, taking Bitmine (BMNR) as an example, bets on eventually acquiring 5% of the circulation share, becoming a new player, and following the path of stock market figures like Sun and Yi Lihua to profit from volatility trends.

BNB/SOL/HYPE treasury strategy involves project foundations or single entities driving up stock prices to stimulate local currency growth. This is the most trend-following batch, as these assets have not yet achieved market value similar to BTC/ETH.

ENA's treasury StablecoinX is quite different from the above; on the surface, it involves ENA's on-chain entity investment and fundraising, spending 260 million dollars to purchase 8% of the ENA circulation, stimulating ENA's price increase by transferring from one hand to the other.

The market responded positively to this, with Ethena's TVL, USDe supply, and sUSDe APY rising in response. However, note that sUSDe is essentially the protocol's liability; ENA's sales revenue is the profit.

StablecoinX reduces the circulation of ENA, stimulating sales growth in the secondary market. The communication costs involved are controllable, as Ethena and investors Pantera, Dragonfly, and Wintermute can negotiate.

Of these, Dragonfly is the lead investor in Ethena's seed round, and Wintermute is also an investor. Compared to new investments, this looks more like accounting.

Ethena is on the path of capital operations, successfully escaping the dual-token system. This should be the biggest stablecoin innovation after Luna-UST.

Real adoption has yet to occur.

When the false prosperity is shattered, those things that have long been rooted will be exposed.

The new upward trend of ENA is one of the sources of project profit, and the holdings of USDe/sUSDe will also increase accordingly. At the very least, USDe now has the potential to become a truly application-oriented stablecoin.

ENA's treasury strategy mimics BNB/SOL/HYPE, driving up yields to stimulate stablecoin adoption. It can both profit from volatility trends, and the high control under the negotiation mechanism alleviates sell pressure during downturns.

Capital operations can only stimulate token prices; stabilizing the growth flywheel of USDe and ENA requires the real application of USDe in the long term to cover market-making costs.

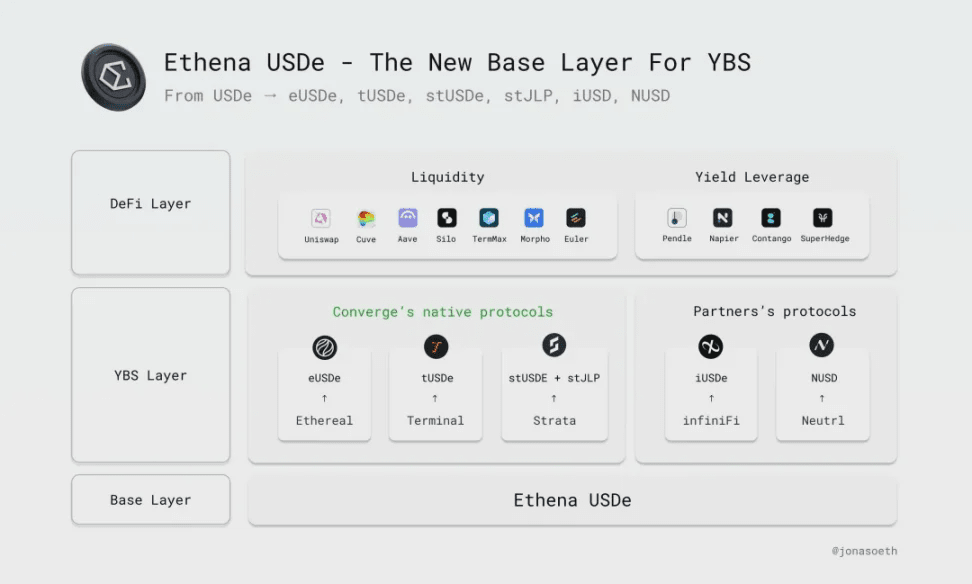

Image description: Ethena's ecological expansion, image source.

On this point, Ethena has always walked on two legs: both on-chain and off-chain.

On-chain: Ethena has a long-term partnership with Pendle to invigorate the on-chain interest rate market, and is also gradually cooperating with Hyperliquid, while internally supporting Ethreal as a backup for Perp DEX.

Off-chain: Partnering with BlackRock's partner Securitize to issue Converge EVM chain, targeting institutional adoption. After the latest Genius Act, Anchorage Digital has increased the issuance of compliant stablecoin USDtb.

Additionally, both Anchorage Digital and Galaxy Digital are recent hot institutions. In a sense, they represent the third wave of market makers after Jump Trading/Alameda Research, with the second wave being market makers like DWF/Wintermute, which will be detailed later.

Outside the on-chain and off-chain capital landscape, real-world adoption of Ethena remains lacking.

Compared to USDT and USDC, USDe/USDtb only scratches the surface in cross-border payments, tokenized funds, and DEX/CEX pricing. The only commendable aspect is the partnership with TON; cooperation with DeFi protocols is hard to penetrate into thousands of households.

If Ethena's goal is on-chain DeFi, then it is already very successful, but if it enters off-chain institutional adoption and retail usage, it can only be said that the long march has just completed the first step.

Moreover, ENA's hidden concerns have emerged, and the fee switch is on the way. Remember that Ethena currently only shares profits with USDe holders, but the fee protocol switch requires ENA holders to share profits through sENA.

Ethena uses ENA to stabilize CEX in exchange for USDe survival space, and through treasury strategies, it stabilizes the interests of large ENA holders and investors. However, what is inevitable will eventually come; once ENA starts sharing protocol income, ENA will also become Ethena's debt rather than income.

Only by truly becoming a USDT/USDC analog can ENA enter a real hematopoietic cycle; currently, it still struggles, and pressure never truly dissipates.

Conclusion

Ethena's capital operations inspire more stablecoin and YBS (yield-bearing stablecoin) projects. Even Genius Act compliant payment stablecoins can be said to allow RWA to be tokenized for interest calculation.

Following Ethena, Resolv also announced activation of the fee switch protocol, but it will not actually share profits with token holders for now. Ultimately, the premise for profit sharing from protocol income is to have protocol income.

Uniswap has been cautious with the fee switch for years, aiming to maximize protocol income between LP and UNI holders. However, most YBS/stablecoin projects currently lack sustainable revenue capabilities.

Capital stimulation is a pacemaker; real adoption is a hematopoietic protein.