I specifically reviewed the performance of the market in August over the years, and indeed, it is quite 'shadowy.' Historical data shows that both Bitcoin and Ethereum have a higher probability of decline in August.

But interestingly— the average return rate is surprisingly positive.

In other words, although August is often a peak period for fluctuations and corrections, when the bull market is in a strong phase of a larger cycle, it may not be a source of risk, but rather a continuation of the main rising wave.

The position in 2025 corresponds precisely with the two 'explosion years' of 2021 and 2017, which means it may be too early to assert that the bull market has ended.

Bitcoin: The longer the period of fluctuation, the more limited the potential for a breakout.

From the hourly chart of #BTC, the longer this low-level consolidation lasts, the more the 'momentum' for subsequent rebounds will be consumed. If the fluctuation pattern escalates to a 4-hour or even daily level, it could lead to the risk of breaking support and trend reversal.

Therefore, in short-term operations, a more reasonable strategy is: wait for the 15-minute cycle to rearrange the upward structure, or wait for the 4-hour chart to retest the bottom, showing clearer 'pullback confirmation.'

Ethereum: Monthly structure is robust, and the trend still has continuation potential.

#ETH's monthly chart actually looks very healthy, with lows gradually rising, overall still showing an upward channel. Even though the 'psychological barrier' of $4000 has failed to break through twice, the underlying reasons are also easy to understand: in the last bull market, many people stood guard at this position, leading to heavy selling pressure.

However, it is worth noting that after each dip, there has been increasing buying support at the lower shadow line, such as the long bullish candle with volume in July, which is a typical 'dip recovery'.

Moreover, this upward rhythm is different from past 'false bullish candles.' This time it is accompanied by significant volume and acceleration, not weak.

The MACD indicator is still forming a golden cross above the zero line, indicating that the main force is still holding firm. As long as there isn't a sudden massive sell-off, ETH in August still has hope for further upward movement.

Macroeconomic variables: Is it true that the 'worse' the data is, the better it is for the market?

There are also some key signals on the macro front worth noting. The latest U.S. employment data:

Unemployment rate higher than market expectations → Positive

Non-farm payrolls lower than expected → Still positive

This seems a bit unusual, but in the 'Federal Reserve rate cut logic', the weaker the economic data, the more likely it is to prompt policy easing, thus providing support for risk assets.

However, the recent PCE price index unexpectedly came in high, causing market sentiment to cool instantly. This drop is essentially a 'correction of overly high expectations for rate cuts.'

But it is worth mentioning that: the SEC chairman has just officially announced the launch of the Project Crypto plan, which is a substantial policy benefit for multiple sectors such as #DeFi, #RWA, and #L1 public chains.

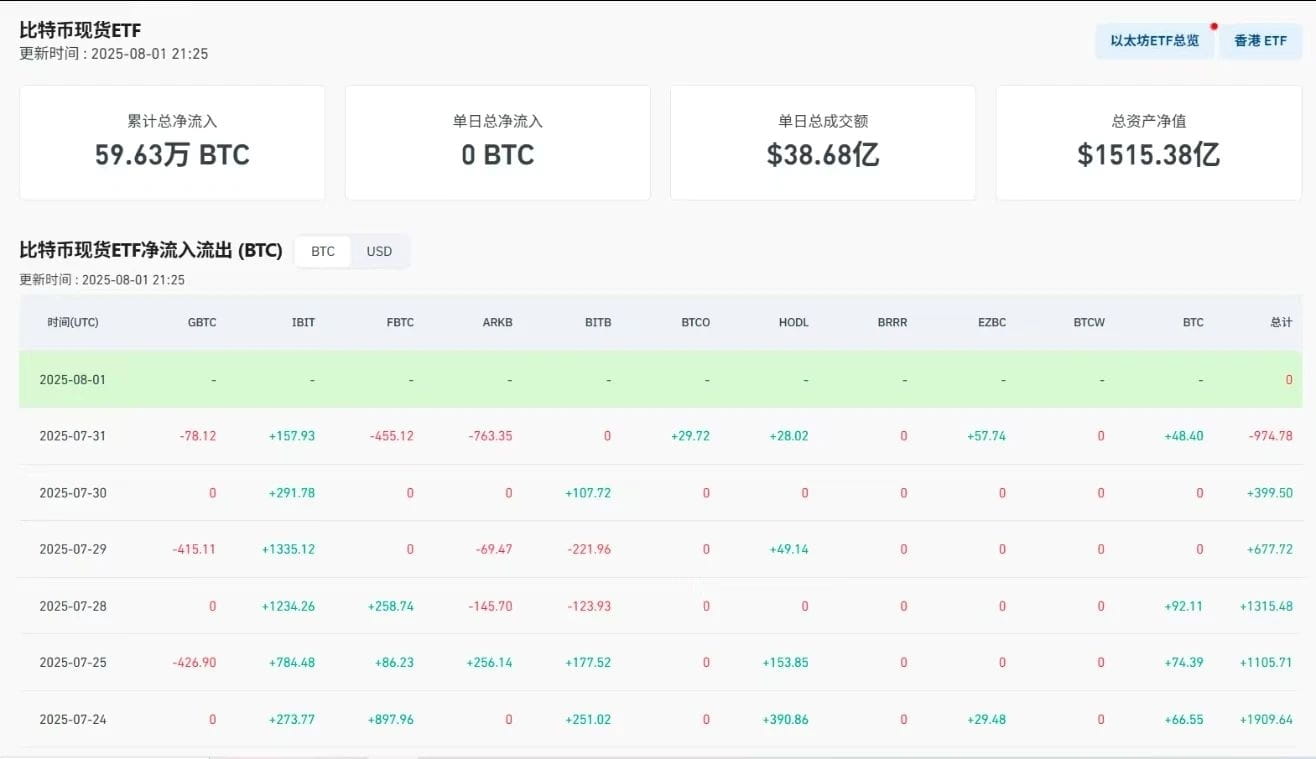

ETF fund flow: although there has been a pullback, the pattern remains unchanged.

From a funding perspective:

Bitcoin ETF saw a net outflow of $114 million yesterday;

BlackRock has not purchased new shares for two consecutive days;

Although Ethereum ETF saw a small inflow (about $17 million), the momentum has noticeably weakened.

Although there was a $2 million inflow into ETFs from Solana, the overall market performance remains poor, almost causing no ripple effect.

This actually sends a signal: projects that can truly attract traditional and on-chain funds must meet several conditions simultaneously, such as:

Has ETF or treasury backing.

Grayscale or WLFI holdings

Actively subscribed by large institutions

Altcoins lacking these supports are likely just 'air.'

Final summary: August may not be the endpoint, but rather a starting point.

Although August is often seen as a 'quiet month' for the market, in strong bull years (like 2017 and 2021), it often becomes a starting point for structural market explosions. The key is: when funds will rotate again and how sentiment will switch.

Currently, although facing adverse factors such as ETF fund outflows, macro policy disturbances, and tax rate pressures, Ethereum's structure still leans bullish, the SEC's attitude has softened, and the heat in the RWA and chain reform sectors has increased. This round of correction is more likely a segment correction of the market rather than an end.

Final suggestion:

When selecting investment targets, please keep in mind a core judgment criterion:

For projects that 'institutions don't touch, treasury hasn't entered, and ETFs are absent,' don't engage in battle, and definitely don't hold on blindly.