Please note that the reading time for this article is about 20 minutes. If you are impatient to understand the market and just want to gamble blindly, then you can swipe away.

This answer is quite long; if you can’t read it, skip to the end of the article. There is a sentence that summarizes my ten years of ups and downs in the crypto space, and the experience I gained in turning losses into profits!

Perpetual contracts have become the largest trading method in cryptocurrency trading, but perpetual contracts are a unique product in the crypto space, completely different from other trading products we usually encounter, so understanding perpetual contracts can be somewhat difficult. Even many people frequently use perpetual contracts but still do not understand the meaning of various indicators and how they are calculated.

Many people face liquidation because they fundamentally do not understand the essence of perpetual contracts in the cryptocurrency space. After reading many exchange help center documents and combining my own trading experience, I try to explain the product principles of perpetual contracts, as well as the calculations for margin, position profit and loss, and liquidation price using the simplest formulas and mathematics.

The full name of the perpetual contract should be "futures perpetual contract," with three key terms being "futures," "perpetual," and "contract." First, we need to understand what futures trading is. Futures trading is in contrast to spot trading; in spot trading, both parties directly exchange money for goods.

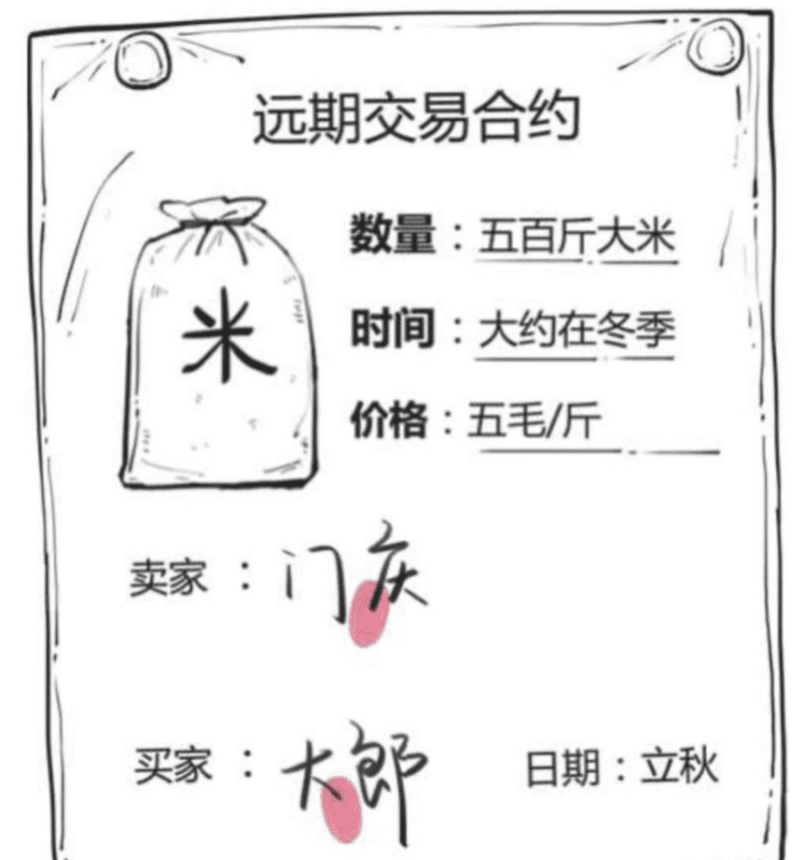

In futures trading, both parties agree to trade a certain commodity at a certain price at a future time. For example: Xiao Ming and Xiao Hong agree that in two months, Xiao Ming will sell 100 pounds of rice to Xiao Hong at a price of 200 yuan per pound, and both parties sign a contract, making Xiao Ming the seller of this contract and Xiao Hong the buyer.

So futures contracts refer to contracts in the form of futures trading. But if during this process, Xiao Hong suddenly no longer wants to buy rice according to the original agreement, she can sell this contract to someone else, at which point she shifts from the buyer to the seller of the contract. The contracts we just mentioned all have an expiration date, and must be settled in the end, meaning that on the settlement date, both parties are compelled to settle according to the original agreement, thus these contracts are also called futures settlement contracts.

To ensure that both parties in the contract can adhere to the agreement on the contract expiration date, both must pay a certain amount of capital, which is the margin.

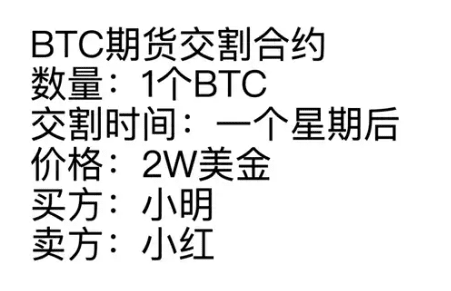

Returning to the cryptocurrency example, assume the current BTC price is $20,000, and Xiao Ming believes that by next week, BTC will rise to $25,000. Xiao Ming pays a certain margin and buys a BTC bullish contract, which represents that next week, Xiao Ming has the right to buy BTC at $20,000. However, Xiao Ming's contract requires a counterparty, which we assume is Xiao Hong. Xiao Hong believes that BTC will fall next week, so she wants to sell BTC for $20,000 next week.

By next week, if BTC price drops to $18,000, then Xiao Ming incurs a loss while Xiao Hong makes a profit.

The futures contracts discussed above ultimately must be settled, while there is another type of contract without a settlement time, which is the futures perpetual contract we mainly discuss today. Perpetual contracts are divided into two types: forward contracts and reverse contracts:

Forward contracts are easy to understand, similar to the examples we discussed earlier, tracking the trading target is BTC, priced in USDT, and the margin is also in USDT.

In contrast, while reverse contracts track the same underlying asset and pricing method as forward contracts, they use BTC as margin.

From the trading experience perspective, forward contracts use USDT as a margin for various coins, which indeed is more flexible and suitable for beginners. The unit of contracts is "lots," but what are the par values for a forward contract and a reverse contract? The par value of a BTC contract usually needs to be agreed upon in advance. The difference lies in that a forward contract's par value is based on the amount of BTC (how many BTC it is worth), while a reverse contract is based on the amount of USDT (how much USDT it is worth). For example, we can hypothesize this:

Contract type contract value one forward BTC contract value 0.1 BTC one reverse BTC contract value 100 USDT

It is important to note that the contract values may not be the same across different exchanges. Although usually they copy each other, specifics still depend on each exchange's announcements.

Margin is the capital required at the time of opening a position, and the margin calculations for the two types of contracts are as follows:

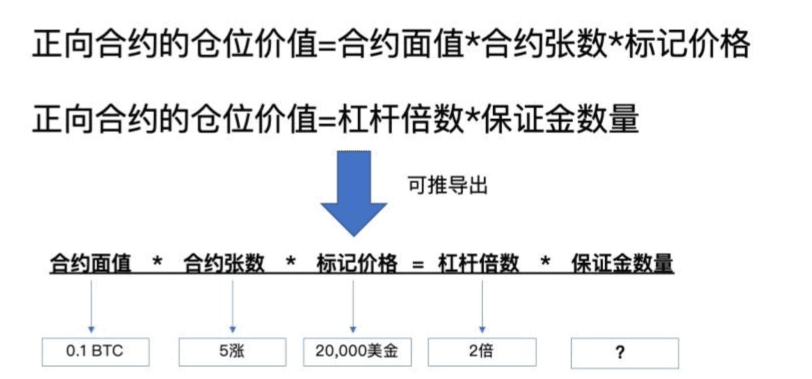

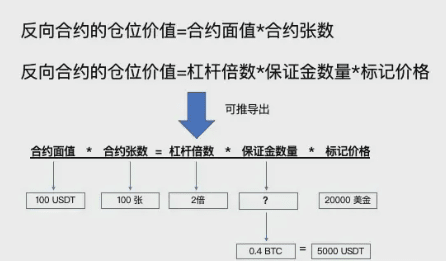

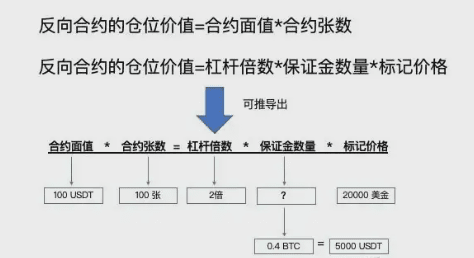

The position value of a forward contract = contract value * number of contracts * mark price

The position value of a forward contract = leverage multiplier * margin amount

So in forward contracts: contract value * number of contracts * mark price = leverage multiplier * margin amount

From this formula, we can deduce the amount of margin. For example, when the BTC price is $20,000, buying 5 BTC forward contracts with 2x leverage gives: margin = 0.1 * 20000 * 5 / 2 = 5000 USDT. (Assuming 0.1 BTC as one contract value, 20000 as the mark price, 5 as the number of contracts, and 2 as the leverage multiplier)

The situation for reverse contracts is:

The position value of a reverse contract = contract value * number of contracts

The position value of a reverse contract = leverage multiplier * margin amount * mark price

Thus, in reverse contracts: contract value * number of contracts = leverage multiplier * margin amount * mark price

In the same situation, the position value of the forward contract in the above example is $10,000, so in the reverse contract we also buy contracts with the same position value, needing to buy 100 contracts (assuming one BTC reverse contract is 100 USDT, buying 100 contracts equals $10,000), thus: margin = 100 * 100 / (2 * 20000) = 0.4 BTC. 0.4 BTC is exactly worth 5000 USDT, which is consistent with the margin amount calculated for the forward contract above.

Next, let’s see how the profit and loss of the two types of contracts are calculated:

In a forward contract,

When going long: Profit and loss of a forward contract = (closing price - opening price) * contract value * number of contracts

When shorting: Profit and loss of a forward contract = (opening price - closing price) * contract value * number of contracts

Still using the example above, assuming we buy 5 BTC contracts when the price is $20,000 and sell when the price is $25,000, then the profit and loss for this operation is:

Profit and loss = (25,000 - 20,000) * 0.1 * 5 = 2500 USDT

In the reverse contract,

When going long: Profit and loss of a reverse contract = (1/opening price - 1/closing price) x contract value x number of contracts

When shorting: Profit and loss of a reverse contract = (1/closing price - 1/opening price) x contract value x number of contracts

Assuming we buy 100 BTC contracts when the price is $20,000, the position value at opening is = 100 * 100 = $10,000, and we sell when the price is $25,000, then the profit and loss for this operation is: = (1/20000 - 1/25000) * 100 * 100 = 0.1 BTC, profit and loss is 2500 USDT

This means that the BTC earned in a reverse contract, if sold again at the closing price, equals the USDT earned in a forward contract.

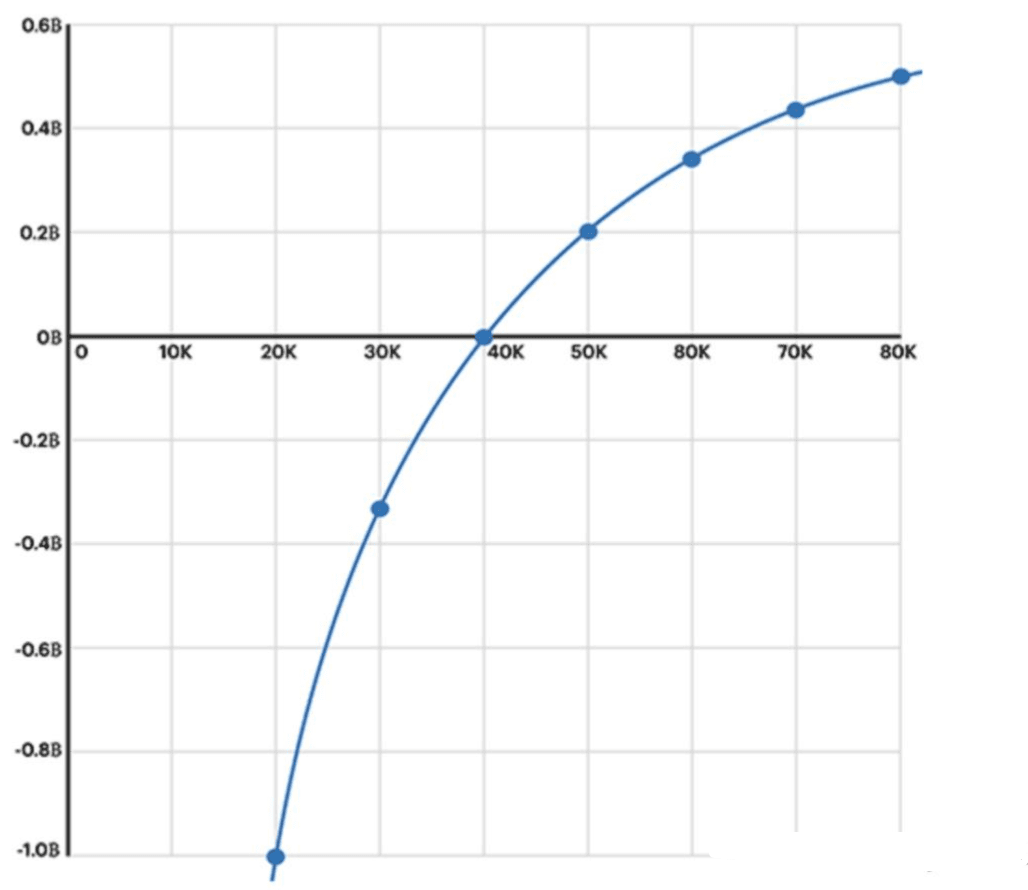

From these two formulas, we see that the relationship between forward contracts and the difference between opening and closing prices is linear, but for reverse contracts, it is not; they present a convex function relationship.

Therefore, the characteristic of a reverse contract is that when the price rises, the BTC earned does not increase linearly but decreases more and more. Conversely, when the price drops, the BTC lost does not decrease linearly but increases more and more.

Finally, let’s talk about how to calculate the liquidation price. If you don’t want to see the calculations, you can directly look at the conclusions in this table:

Liquidation price for long and short reverse contracts drop by 1/(N+1) rise by 1/(N-1) forward contracts drop by 1/N rise by 1/N

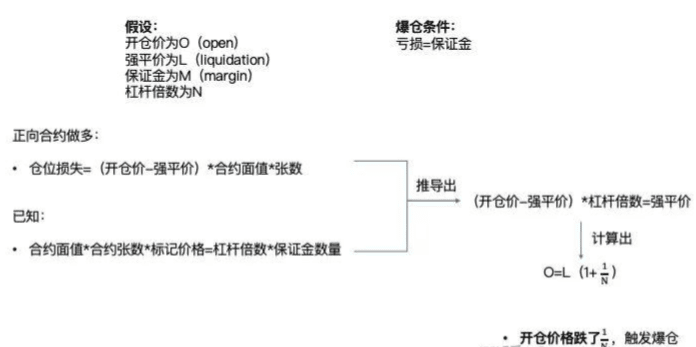

The basic principle of liquidation is that when losses equal the margin, liquidation will be triggered.

Let’s assume the opening price is O (open), the liquidation price is L (liquidation), the margin is M (margin), and the leverage multiplier is N.

In the forward contract long scenario, the position value at opening = contract value * number of contracts * opening price, and the position value at liquidation = contract value * number of contracts * liquidation price. When the position loss = (opening price - liquidation price) * contract value * number of contracts = margin, the position is liquidated.

Given: contract value * number of contracts * mark price = leverage multiplier * margin amount

Substituting the above formula leads to: (opening price - liquidation price) * leverage multiplier = liquidation price calculated as O = L(1 + 1/N), which means that if the opening price drops by 1/N, liquidation is triggered.

Back to our example, if the opening price is $20,000, under 2x leverage, the price drops to $10,000 and liquidation is triggered; if under 50x leverage, the price drops to $19,600 and liquidation is triggered.

The same situation applies to shorting; the price rising by 1/N triggers liquidation, and I won’t elaborate further.

The situation for forward contracts is comparatively simple; we mainly focus on reverse contracts.

In the long scenario, the position value at opening is O*N*M, and the position value at closing is L*N*M, thus the loss = (O-L)*N*M, and the margin value = L*M, so when (O-L)*N*M = L*M, liquidation is triggered.

Combining the above two formulas, we can conclude: L=O(1-1/N+1), meaning that when going long, if the opening price drops by 1/N+1, liquidation is triggered.

In the above example, under 2x leverage, the price drops to 13,333 and triggers liquidation.

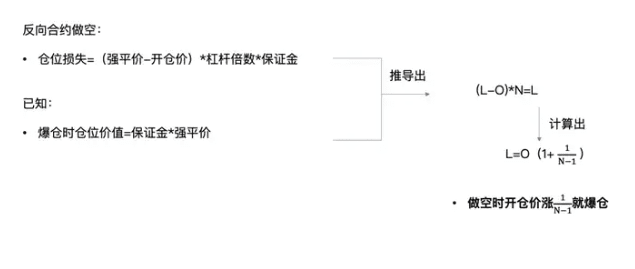

In the short scenario, the position value at opening is O*N*M, at closing it is L*N*M, the loss = (L-O)*N*M, and the margin value = L*M, so when (L-O)*N*M = L*M, liquidation is triggered.

L=O(1+1/N-1), which means that when shorting, if the opening price rises by 1/N-1, liquidation is triggered. Let's look at an example: with 2x leverage, if the price rises by 50%, liquidation is triggered; however, if with 1x leverage, it will never liquidate. This means: in a reverse contract, if you short with 1x leverage, you will never liquidate!! This is why many short sellers prefer to use reverse contracts.

The trading accumulation of over a decade in the crypto space ultimately boils down to a dual enlightenment of the market and human nature. The essence of the market is a playground for human nature, whose rules are never predicted but are repeatedly validated by human greed and fear. In the early years, I always thought about overcoming the market; later, I understood that the true survival rule is to submit to its rhythm—don’t be greedy when it rises, don’t be fearful when it falls, because the endpoint of all extreme conditions is the collective eruption of human weaknesses.

In the end, trading is just a tool, the real threshold is self-control: greed makes one stubbornly hold onto trends, fear makes one miss turning points, and luck is the prelude to liquidation. Those who survive in this market do not rely on a stroke of luck for huge profits, but on discipline to tame desire and patience to counter uncertainty. Understanding the complexity of human nature also helps to understand the ups and downs of K-line; controlling one’s inner demons allows one to step precisely on their own cycles amid volatility.

If you currently feel helpless, confused, and want to learn more about the cryptocurrency world and cutting-edge information, click on my avatar to follow me, and you won’t get lost! Clear market trends provide confidence in operations. Stably profiting is far more practical than fantasizing about getting rich quickly.