Between Trump and Powell, who truly understands the impact of tariffs on the U.S. economy and inflation more?

With the release of the slightly below-expectations U.S. June CPI report on Tuesday, Trump evidently believes he has 'won' again; however, judging by the performance of financial markets, investors seem to think that Powell was the real 'winner' last night—because expectations for a Fed rate cut in September further declined after last night's data...

This may be an interesting scene, where both Trump, who calls for an immediate rate cut by the Fed, and the Fed, which has been cautious and inactive this year, can find arguments favorable to their positions in this latest June CPI report...

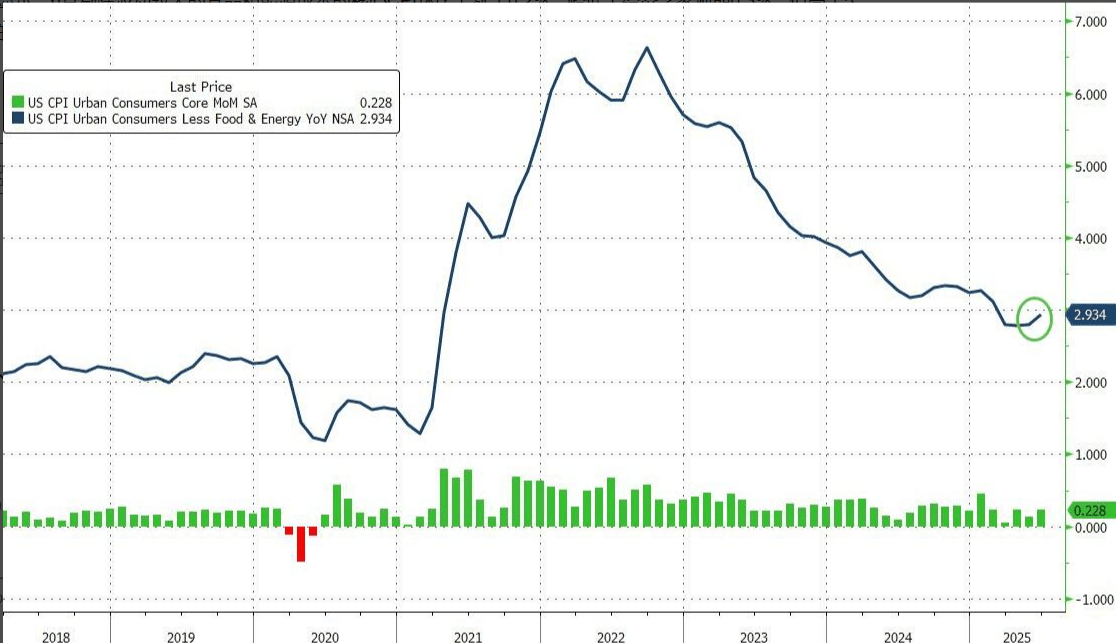

This is evidently related to the final results presented by the June CPI data. Among a set of indicators that have garnered the most attention from industry insiders: although the month-on-month increase in U.S. core CPI was below expectations, it was indeed higher than the previous month.

Data shows that in June, the core CPI excluding volatile food and energy costs rose by 0.2% month-on-month, slightly below economists' expectation of 0.3%, but higher than May's increase of 0.1%.

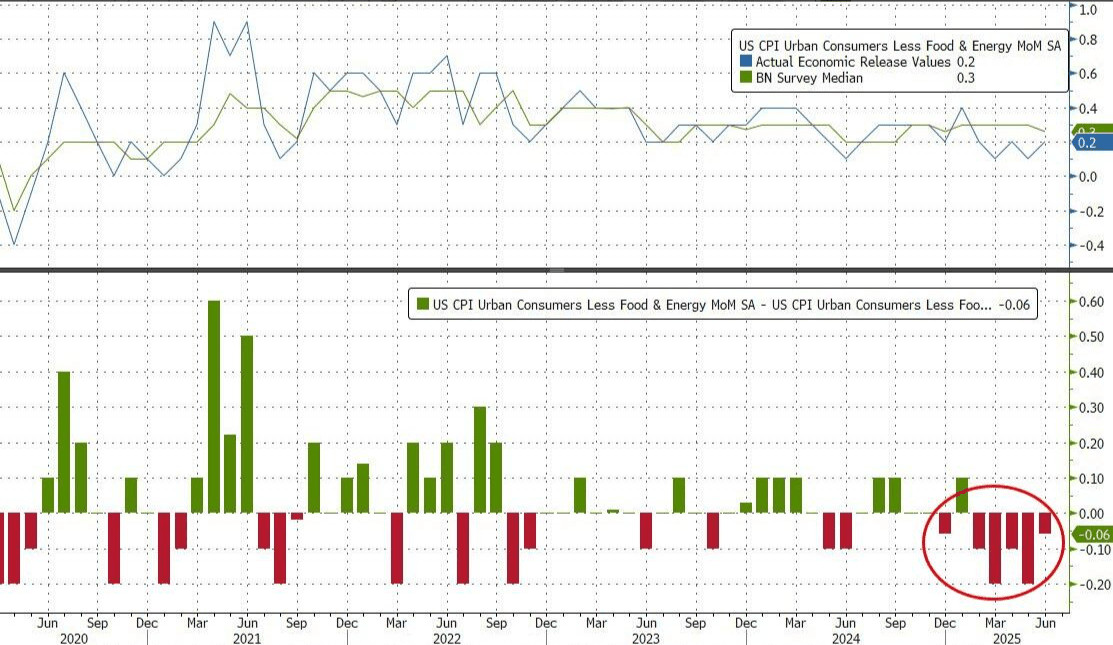

It is worth mentioning that this marks the fifth consecutive month where the actual core CPI month-on-month data in the U.S. has underperformed against market expectations:

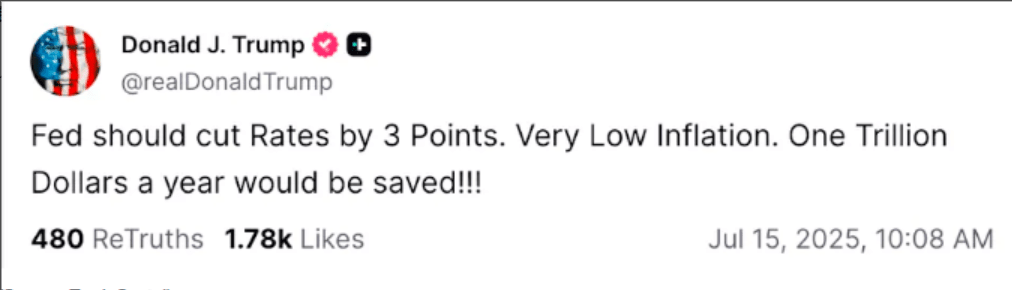

As we envisioned in our forecast yesterday, the inflation report that was slightly below market expectations quickly provided a new 'pretext' for President Trump to criticize the Federal Reserve. Shortly after the release of the data on Tuesday, Trump again publicly called for the Fed to cut rates significantly.

Trump wrote on the Truth Social platform: "The Fed should cut rates by 300 basis points. Inflation is very low. This could save a trillion dollars a year!!!"

However, unlike Trump, who believes he 'understands' that the CPI supports a Fed rate cut, financial market traders and Wall Street analysts last night seemed to think that this inflation report actually supports the Fed's cautious stance of remaining on hold...

On Tuesday, both the U.S. equity and bond markets faced pressure following the release of the CPI report. The Dow Jones Industrial Average dropped over 400 points, while the S&P 500 fell by 0.4%. Meanwhile, the yield on the 30-year U.S. Treasury bond broke above the key 5% mark on Tuesday; the benchmark 10-year Treasury yield rose by 6.4 basis points to 4.487%, marking a four-day increase. This 'anchor for global asset pricing' earlier in the day had reached a high of 4.491%, the strongest level since June 11.

Interest rate cut expectations have weakened! The real winner of CPI night is Powell?

Many industry insiders have stated that although the overall inflation data met expectations, the rising prices of goods such as furniture and large appliances suggest that Trump's tariff policies may be increasing the cost of living for Americans.

Seema Shah, chief global strategist at Principal Asset Management, stated after the release of the data on Tuesday that whether the Fed can cut rates largely depends on Tuesday's inflation data. Since core inflation has been below expectations for five consecutive months, the initial data appears to still show no signs of the inflationary boost effects anticipated by the Fed due to tariffs; however, a closer look reveals that as prices of categories such as household goods, entertainment, and clothing rise, import tariffs are gradually being transmitted to core commodity prices.

In fact, in June, U.S. clothing prices rose by 0.4% month-on-month, and shoe prices increased by 0.7% after several months of decline. Prices for furniture and bedding also rose by 0.4%, reversing a 0.8% decline in May, all of which may indicate that cost pressures related to tariffs are beginning to be transmitted to consumers.

Shah believes that the full inflation impact of tariffs may take time to manifest, especially in cases where some goods were shipped early before the latest tariffs took effect. "Given that higher tariffs have already been announced, it would be wise for the Fed to maintain a wait-and-see approach for at least the next few months."

Omair Sharif, president of Inflation Insights LLC, also pointed out that the core CPI excluding volatile food and energy costs rose by 0.55% in June, marking the highest level since November 2021. "Today's report shows that tariffs are starting to take effect."

"Powell has been very adamant about some things, one of which is—inflation is coming. Although this report does not reflect it clearly, the situation is brewing," wrote Jim Barnes, head of fixed income at Bryn Mawr Trust.

Robert Haworth, senior investment strategy director at Bank of America Asset Management, said: "Today's CPI data—especially in the appliances sector—indicates that we are starting to see the effects of tariffs." He noted that signs of accelerating inflation would only "intensify the uncertainty about what action the Fed should take."

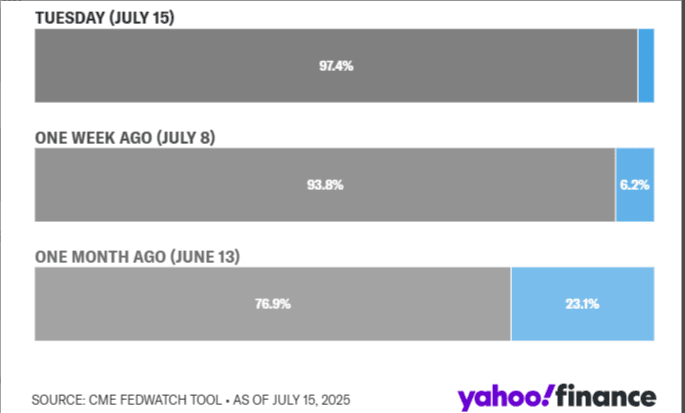

According to the CME's FedWatch tool, following the release of the CPI report, investors' expectations for the Fed to keep interest rates unchanged at the July meeting rose to 97%, up from 93% on Monday. Meanwhile, the likelihood of a rate cut in September sharply declined after the report was released, quickly falling below 60%, and then, as the market further digested the data, that probability slid down to nearly 50%.

As Wall Street has been repeatedly reminded, the Fed's cautious stance stems not only from recent data but also from concerns over the uncertainty surrounding President Trump's continually evolving tariff policies.

Ryan Sweet, chief U.S. economist at Oxford Economics, stated that if Trump's proposed tariffs effective August 1 go into effect, the inflation impact on commodity prices may take months to materialize. Sweet, who currently predicts that the Fed will not make its next rate cut until December, noted that this could keep the Fed on the sidelines unless the labor market significantly weakens.

"If the new tariffs are implemented, this may delay the timing of the next interest rate cut until after the baseline forecast," the economist said. "Due to the uncertainty surrounding the tariffs, the Federal Reserve may be willing to wait longer before making a more aggressive rate cut to compensate for it."

Old Zhu summarizes:

July PPI data (to be released today at 20:30) → If it exceeds expectations, it will solidify the 'wait-and-see' expectations.

Fed Beige Book (tomorrow 02:00) → Observing regional tariff impacts

Details on Trump's 'Small Country Tariff Letter' → Global trade chain risks resurge.

The National Congress votes tonight: the survival of the crypto industry in 48 hours!

The House will vote again on three epic bills on July 17 (tonight); if passed, it will trigger a nuclear-level market reaction.

(GENIUS Act): The issuance of stablecoins will be centralized under the Fed, putting USDT and USDC in a 'licensed stranglehold.'

(Anti-CBDC Act): Permanently prohibits the Fed from issuing a digital dollar, targeting the global central bank digital currency hegemony from the Trump administration.

(CLARITY Act): Requires the SEC and CFTC to clarify token classifications, possibly speeding up Ethereum spot ETF approvals!

Follow Old Zhu for a deep analysis and practical tutorials tonight.