Geopolitical tensions escalated over the weekend, as US bombers made a surprisingly quick and precise attack on 3 Iranian nuclear installations situated well underground. Damages to the sites were stated to be severe according to US reports, though there has yet to be official confirmations on whether the nuclear material had been destroyed or evacuated away earlier.

The knee-jerk reaction was to sell risk assets over the week, with crypto taking the brunt of the damage by virtue of being the only asset class open as BTC fell ~4% from >102k to ~99k as the attacks were first launched. Don’t forget that crypto will continue to be treated as a frontier/risky asset class by TradFi investors until further notice.

Participants were originally worried about a tough Monday open given the kinetic escalation, though those concerns appear to be dissipated quickly in the early Asian hours. Instead of worrying about the onset of a larger global conflict, a nascent view is emerging that this might have been a successful “escalate to de-escalate”, where the US’s critical show of force becomes a powerful motivator for negotiating parties. Practical difficulties with blocking the Strait of Hormuz (vast majority of Iran oil/LNG exports are to China) have also eased concerns on a runaway oil spike.

The early morning price action would seem to agree with this view, with US equity futures having rebounded back nearly to the Friday levels, oil prices steady at ~$75/barrel, spot gold giving up all its early gains, and USD-Shekel having recovered back to pre-conflict lows.

In general, geopolitical stress tends to be short-lived with only temporary effects on equity prices. A recent study from Citi shows that the SPX tends to react negatively heading into geopolitical event risk, but tends to fare just fine once it takes place. This makes logical sense if we continue to believe that equity markets are generally efficient and forward looking at pricing-in all available known and known-unknown risks. Absent an unfathomable WMD strike or a truly outlier development, we would also expect risk markets to normalize themselves to this latest conflict and to refocus back on the ongoing tariffs negotiations and economic developments.

In rates markets, despite all the noise surrounding outsized US interest payments, possible runaway inflation, implied rates volatility have cratered back to interim lows, with the markets not expecting DM central banks to be ‘in-play’, as the forward rate trajectory remains highly stable with bond traders back in cruise-control mode.

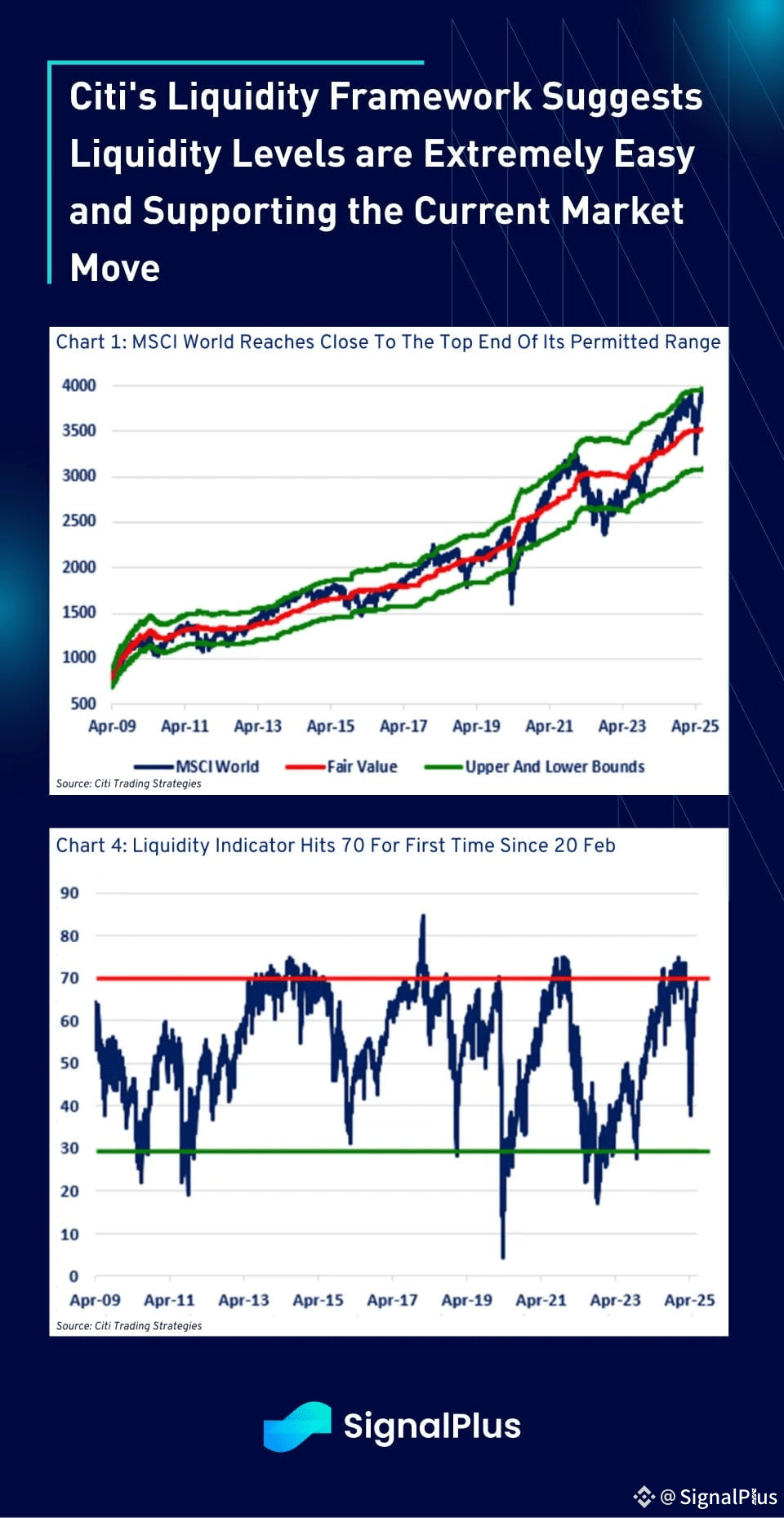

At the same time, market liquidity (aka financial conditions) remain ample by most Wall Street mentions, which has allowed risk assets (eg. equity) to continue scaling the proverbial wall of worry, with the SPX recovering smartly despite Liberation Day and ongoing Russia-Ukraine and Israel-Iran complications.

While macro observers might remain (permanently) bearish, investors are voting with their wallets and risk-sentiment remains comfortably risk-on underneath all the premonitions, as the overall economy continues to putter on with rising corporate earnings.

Unfortunately, the same cannot be said in crypto. BTC fell -4% to touch ~$98.9k, while ETH dropped ~10% to $2150, hitting the lowest intraday levels since early May. Well over $1bln in futures were liquidated over the weekend over the Iran strikes, as traders naturally sold the only market that was open.

While equities, oil, and gold prices have reversed their weekend moves early on, crypto is struggling to do the same, as participants are still caught long in the interim with a lot of PNL noise over the past month, as prices have struggled to make any headway since Q1 with BTC still struggling to break the February highs.

Glassnode performed an excellent analysis last week, which suggested that on-chain BTC activity has also slowed materially despite all the excitement from the TradFi community. Effectively, off-chain ‘OTC’ has been active as mainstream investors are trying to acquire BTC exposures via traditional instruments (eg. ETFs, futures), while on-chain activity has not recovered since FTX, as evident through the soft DeFi/Altcoin landscape, and slowdown in new narratives (outside of stables/RWA).

Similarly, ‘power rule’ outcomes are becoming more prevalent in crypto, with BTC continuing to gain market cap dominance on one-hand, but even its own transfer volumes are being increasingly dominated by larger wallets. Glassnode reports transactions >$100k have risen in dominance from 66% in 2022 to 89% today, reinforcing the view that ‘whales’ are becoming increasingly dominant in the space, and the market being ever less driven (or even exciting) for smaller accounts.

Unfortunately, this trend is likely to continue as the crypto industry matures, and maybe an unavoidable outcome of its increasing institutionalisation.

Moreover, off-chain volume remains large vs on-chain activity as BTC becomes a mainstream asset class, and will have to ‘play by the rules’ of how macro assets are expected to behave as determined by the largest capital holders. Long-term crypto observers have noted how this cycle has been ‘unprecedented’ given the lack of altcoin catch-up or rise in new narratives, but this is something that we have long feared as TradFi players are only interested in speculating via their tried and true instruments (off-chain). Self-custody and on-chain narratives offer little to this crowd, but their much larger wallet size will mean that price action will be increasingly driven by their mindshare.

This macro-correlation can be visualized through the rising open-interest changes in BTC futures, where the much higher and sharper change since 24Q4 has why we are seeing more frequent liquidation gaps, such as over this weekend. Off-chain activity and futures driven moves equal higher macro correlation and less crypto-native drivers for where prices are going.

Furthermore, similar to what SignalPlus has seen through our franchise as well, crypto options activity has experienced a significant gain in interest through this cycle. Volumes have surged from ~1.5B / day in 2024 to a peak of $5B / day most recently, highlighting the growing use of options by increasingly sophisticated participants in managing their risk exposures. Please keep engaging with the SignalPlus team on how we can help you on this journey!

Back at the current junction, momentum demand on BTC looks lethargic with CryptoQuant reporting the worst demand momentum on their index record. Short-term holder supply (ie. New money) appears to be slowing as prices have failed to break out to new highs despite overwhelming positive policy narratives (Genius Act, BTC treasury, HK stablecoin policy etc). Watch this space.

In vol space, prices suggest traders were caught off guard by the move with IV spiking against what had been a one-way downward move in vol. Put skews were heavily bid, particularly in ETH, as traders sought protection to the downside with traders caught-long in delta, with more weakness possible in the short-term.

Looking forward, we think the market will soon normalize and move on from the latest geopolitical episode, and we might actually see a renewed interest in reaching some sort of peace deal for both the Russia and Iran situations, not to mention some breakthrough in the tariff negotiations. Markets should naturally rally on those developments, but at which point the focus should shift back to high equity valuations, where the SPX earnings growth is already pricing in +12% to $296 (20x forward PE), and the US economy appears to be slowing down for real (employment indices, CEO firing intentions).

As we have been consistent with this move, we wouldn’t fight the equity move up, but believe that we are closer to the end of the current rally than not, and would be focused on de-risking. On crypto, given the latest price action, we are more worried of a bigger shake-out to stop out the recently longs and weak-hands, and are worried about the negative FOMO signals from all the public companies looking to establish new BTC treasuries as their latest financial engineering gig.

Stay stay and keep your risks tight, and may cooler heads prevail over the current situation. Good luck.