On the macro level, in the cryptocurrency sector, following the repeal of the highly anticipated SAB 121 bill, a milestone event for compliance has arrived. Global financial giant JPMorgan officially launched compliant lending services backed by Bitcoin and cryptocurrency ETFs. This move marks the first clear acknowledgment by traditional financial institutions of crypto assets as 'financial products'. Although compliance with KYC and AML regulations is still required, this breakthrough obviously paves the way for financing channels for crypto assets and lays the foundation for more flexible financial innovations in the future.

Additionally, there is significant good news regarding Circle's IPO process, with subscription demand reaching 25 times. As the first company centered on compliant dollar stablecoins, Circle's listing not only marks a deep integration of crypto dollar infrastructure with Wall Street, but also indicates that USDC is expected to become a benchmark under the US stablecoin bill, leading the way in achieving a hard-backed stablecoin template.

The traditional financial market is even more turbulent. Trump once again publicly called for the Federal Reserve to cut rates, directly targeting Chairman Powell. However, the market's expectations for a rate cut have been pushed back to after the third quarter. More strikingly, Tesla founder Musk publicly 'fell out' with Trump, criticizing his proposed spending bill as 'disgusting' and calling for its repeal. Musk warned that the bill would lead to a federal deficit soaring to $25 trillion, increasing the burden on citizens. Trump did not respond clearly to this and continued to push his policy agenda.

On the geopolitical front, Trump revealed that he had a long conversation with Putin, but the prospects for a ceasefire in the Russia-Ukraine conflict remain bleak. Putin may take further action against Ukraine, adding uncertainty to global markets. While these events have not directly impacted the markets, they all point to Trump's policy influence. Whether in the crypto industry or the macroeconomy, market logic is tightening around his policy focus.

According to on-chain data, loss-making players are still the main force behind the current turnover. Although the turnover rate has slightly decreased from the previous day, it remains at a high level. Market attention is focused on this Friday's non-farm payroll data, especially the unemployment rate, which remains a key reference for the Federal Reserve's decisions. Unless economic data shows significant weakness, the likelihood of a rate cut in the third quarter remains low.

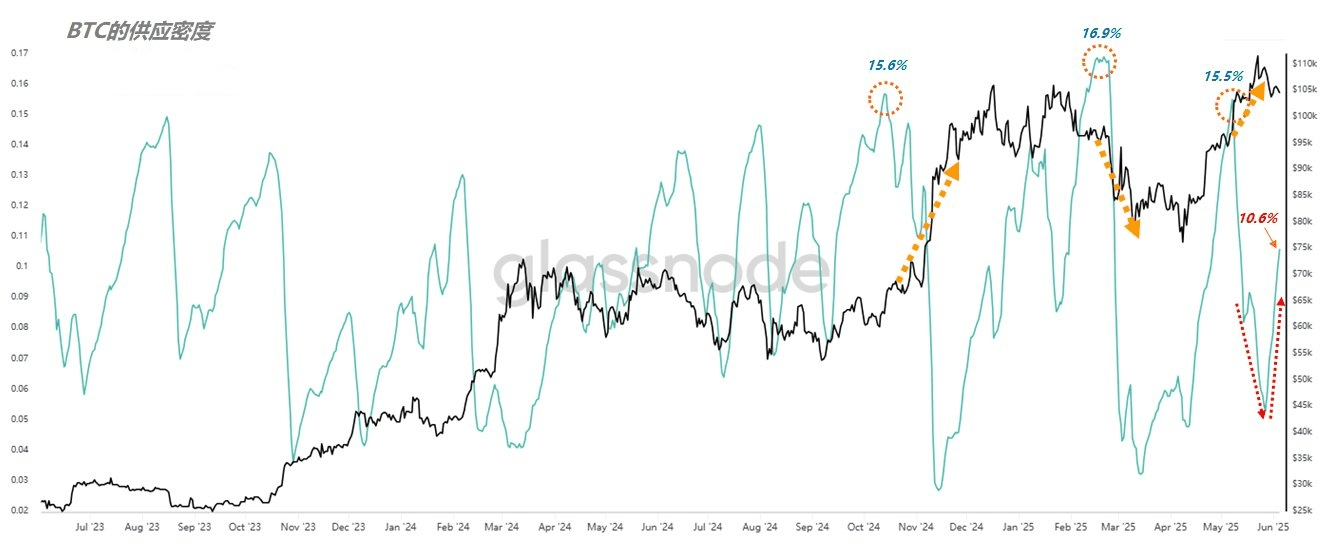

On-chain chip distribution shows that the $93,000 to $98,000 range remains a stable strong support, but more chips are shifting towards the $100,000 to $105,000 range. These players mostly hold short-term positions, making them susceptible to price fluctuations. Recently, Bitcoin's price has been oscillating narrowly around $105,000, but on-chain data reveals a concerning trend: the concentration of holdings has rapidly risen from 5.3% to 10.6% over the past 10 days, with signs of acceleration. If this trend continues, the concentration may break the critical threshold of 15% within one to two weeks, triggering structural adjustments in the market.

Overall, historical data shows that a high concentration of Bitcoin holdings often accompanies severe volatility. For example, in May of this year, when the concentration reached 15.5%, the market redistributed holdings with a rally; while in February, when the concentration rose to 16.9%, it triggered a significant drop. Now, similar signals are reappearing; the current calm may be a sign of the storm before it arrives.#比特币走势分析