This week, U.S. Treasuries experienced the largest weekly decline since the 2019 repo crisis, with volatility even surpassing levels seen during the COVID-19 pandemic in March 2020. More worryingly, the severe fluctuations in the Treasury market put basis arbitrage funds at risk of large-scale liquidation, reminiscent of the situation during the liquidity crisis in March 2020: at that time, many hedge funds were forced to sell other assets to raise liquidity, causing the repo market to freeze and multiple circuit breakers to trigger in the U.S. stock market. So, is the unusual volatility in Treasuries a further release of risks from the Trump tariff war or the beginning of a major crisis?

From a trading perspective, the current volatility of U.S. Treasuries still falls within the category of conventional risk release. There are three main reasons for this.

Firstly, the widening yield spread has triggered clearing pressures that remain limited to basis trading strategies and have not yet spread to systematic strategies such as CTA trend-following or risk parity funds.

Secondly, the money market remains stable—the Federal Reserve's reverse repurchase agreement (RRP) balance of nearly $500 billion constitutes a liquidity buffer, and the overnight repo rate and SOFR spread continue to stay within a normal range of 10 basis points.

Thirdly, the 10-year yield fluctuates within the range of 4.25%-4.5%, with a safe margin remaining from the critical point of 4.8% that would trigger duration hedging for MBS investors. Based on these phenomena, the Federal Reserve still characterizes the current volatility as 'the normal operation of the market's self-adjustment mechanism.'

As long as systemic risks do not erupt, Bitcoin's benefits in the second phase of the trade war have almost become a foregone conclusion.

Firstly, Trump's tariff policy will significantly weaken the dollar's dominant position in global trade settlements, accelerating the diversification of the international payment system. As de-dollarization deepens, the proportion of local currency settlements such as the renminbi and ruble will continue to rise, and gold and Bitcoin will become important anchors for value stability. For example, in 2022, when Russia's foreign exchange reserves were frozen by the West, the Russian central bank implemented a policy of fixed-price gold purchases (5000 rubles/gram) from March 28 to June 30 to alleviate depreciation pressure on the ruble, successfully stabilizing the ruble exchange rate while its gold reserves surged by 300 tons.

It is noteworthy that during the same period, Russia's Bitcoin trading volume surged 17 times, forming a dual-track value storage system of 'official gold + private Bitcoin.' In the context of the U.S. gradually reducing or even stopping the deficit-driven outflow of dollars, this new structure may become an important supplement in the process of de-dollarization.

Secondly, the Trump administration may emulate the operational model of the 1985 'Plaza Accord' by using tariff leverage to force major trading partners to accept a dollar depreciation arrangement. While this 'high tariffs + weak dollar' policy combination could enhance the competitiveness of U.S. manufacturing, it will inevitably erode the credit foundation of the dollar.

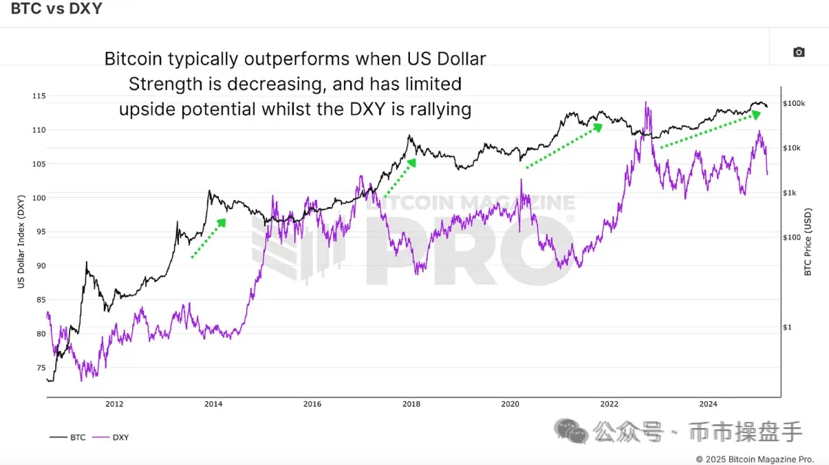

Historical experience shows that when the market forms a sustained expectation of dollar depreciation, hard currencies with 'super-sovereign' attributes often perform outstandingly—during the period from 1985 to 1987 following the Plaza Accord, the dollar depreciated by 50% against the yen and 47% against the Deutsche Mark, while the price of gold rose from about $300 per ounce to around $500, an increase of about 66%, facilitating the reallocation of trillions of dollars in assets. Over the past decade, Bitcoin has shown a clear negative correlation with the dollar index, suggesting that Bitcoin is likely to strengthen during a dollar downtrend.

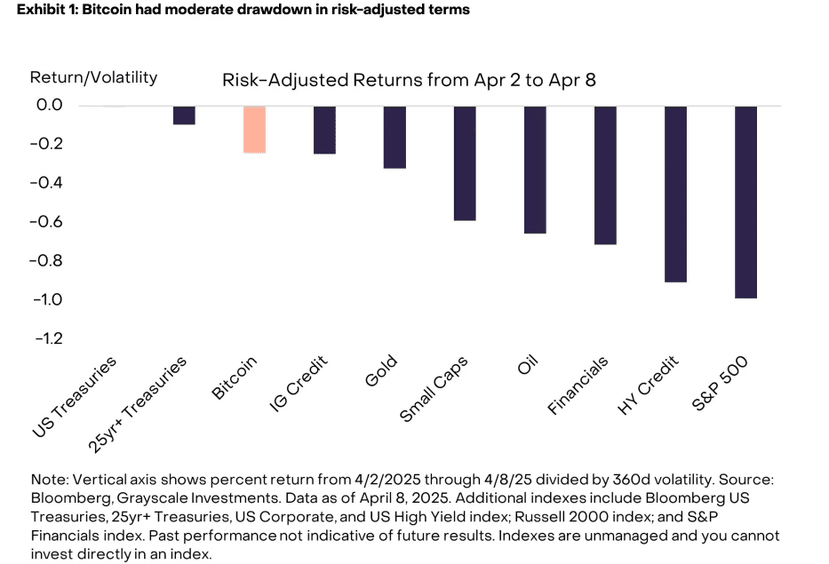

From historical experience, high-quality safe-haven assets must meet two core standards: significant positive risk premiums and controllable price volatility. Over the past decade, gold has been the only asset that has consistently met these two requirements, while Bitcoin has long been excluded from the safe-haven asset category due to its excessive volatility in extreme market conditions (e.g., a single-day fluctuation of 37% in March 2020). However, this traditional understanding is being challenged by new market data. During the market turbulence caused by Trump's tariff policy, the performance of various assets has shown significant changes.

From April 2 to April 8, Bitcoin's risk-adjusted return was -0.24, significantly outperforming the S&P's -0.98 and also higher than gold's -0.29. This shift indicates that Bitcoin is developing a unique 'crisis alpha' attribute—although its absolute volatility remains higher than gold's, its relative performance during systemic risk events has begun to surpass traditional safe-haven assets.

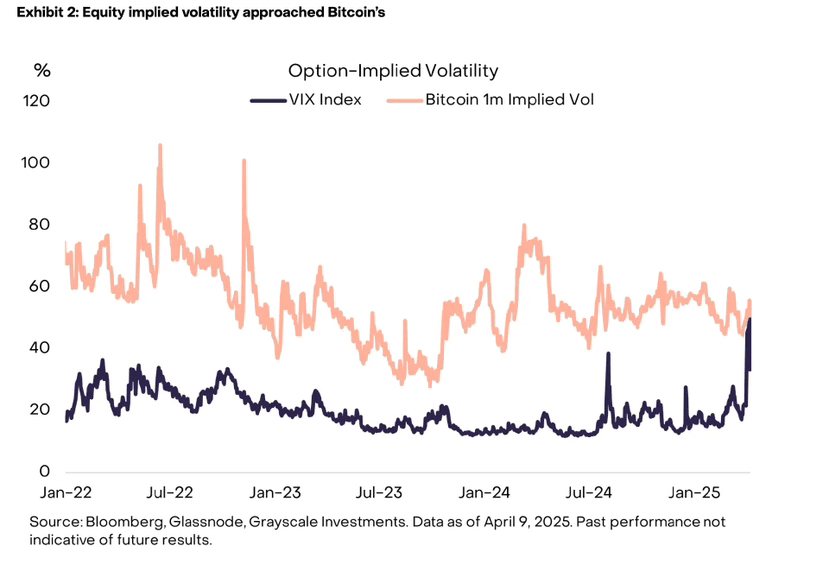

Moreover, despite the VIX index soaring to its highest level in nearly three years (60), Bitcoin's 1-month implied volatility only slightly increased, remaining a considerable distance from historical highs. At the same time, there has been no significant correlation between Bitcoin's price and the implied volatility of its at-the-money options. This suggests that the market generally believes the potential impact of a U.S. stock market crash on Bitcoin is limited, and options investors have not aggressively sought to go long on volatility in light of this event, breaking the past market consensus that Bitcoin acts as leverage for U.S. stocks.

Looking back, Trump's timing for establishing a Bitcoin strategic reserve is no coincidence—this is both a forward-looking arrangement to hedge against dollar credit risk and a strategic move to maintain global currency dominance. However, as U.S. strategic intentions become clearer to the market, U.S. capital has quietly accumulated nearly 30% of the circulating Bitcoin.