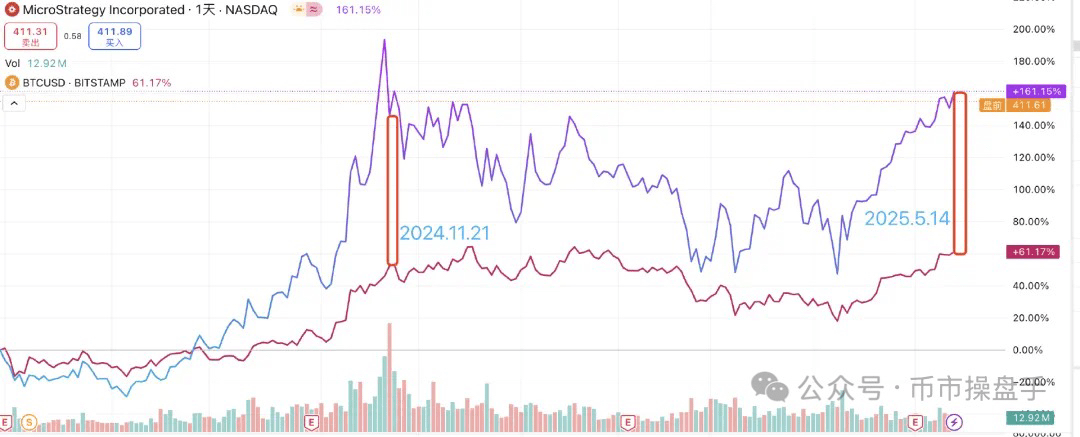

On November 24, 2024, the well-known short-selling institution Citron Research stated on social media that while they are long-term bullish on Bitcoin, they believe MicroStrategy's (MSTR) stock price has deviated from Bitcoin's fundamentals. Therefore, they adopted a hedging strategy of shorting MSTR while going long on BTC, betting that the trends of the two would eventually converge. However, data six months later shows that the price difference between MSTR and BTC not only did not narrow but actually widened by 7%. This means that if the strategy proposed by Citron were strictly executed, the hedging position would have incurred substantial losses over the past six months.

Why is MSTR's Bitcoin asset premium as high as 103%? Although the market generally believes this phenomenon stems from its 'debt issuance to buy coins' leverage strategy, as of May 12, 2025, MSTR had held nearly $60 billion in Bitcoin, while its total liabilities were only $8.5 billion, resulting in an actual debt ratio of less than 15%. This financial structure indicates that traditional leverage theory cannot fully explain its high premium phenomenon. In fact, MSTR's extremely high asset premium reflects more the market's valuation reconstruction of its 'Bitcoin bank' business model—strategic first-mover advantage and strong profit expectations.

For example, in securities trading, there is a significant layered effect in market liquidity: when investors buy a small amount of individual stocks, the trading price is usually close to the market price; however, if trying to acquire more than 5% of shares, due to insufficient order book depth, stock prices may rise significantly. This additional cost caused by large trades is known as liquidity premium. According to Coinglass, the total balance of centralized exchanges currently stands at only 2.17 million coins, while replicating one MSTR (568,840 coins) would come at a cost far exceeding $60 billion.

The liquidity premium essentially reflects the market's expected price difference for Bitcoin in the future, and the rising premium rate reflects a further strengthening of bullish sentiment. From April 7 to May 12, 2025, the premium rate of MSTR's Bitcoin assets rose rapidly from 55% to 103%, indicating that:

1. The market's valuation expectations for Bitcoin are being systematically revised upward.

2. The liquidity of selling in the spot market is showing structural tension (the exchange balance is only 2.17 million coins).

Based on these analyses, we remain optimistic about Bitcoin continuing to reach new historical highs this year.

From May 7 to May 9, the price of ETH skyrocketed from $1,760 to $2,490, an increase of 40%. However, strangely, during the same period, the Ethereum ETF not only did not see inflows but also had an outflow of $20 million. This divergence indicates that the main driving force behind this round of market activity comes from retail investors rather than institutions. The sharp rise combined with retail-led activity has also raised significant concerns about the sustainability of this market rally.

In fact, this situation is not unique to the crypto market. According to a report from JPMorgan, on April 3, the S&P fell by 5%, but retail investors made a record net purchase of $4.5 billion in stocks and ETFs, with net purchases reaching $50 billion in just the first week of April. Earlier, from January to March 2025, retail investors net bought $67 billion in stocks and ETFs. Historically, although institutional positions tend to be more directional, institutions often make mistakes as well.

During the outbreak of COVID-19 in March 2020, institutional investors caused four circuit breakers in the US stock market due to panic selling, but after a surge in April, they aggressively rebuilt positions at high prices, missing the fastest bear market rebound in history (similar to the current situation). Ironically, according to Goldman Sachs' prime brokerage data, on March 23, 2020, the day the market hit bottom, hedge funds had a net sell of the largest scale of the year, while retail investors set a single-day account opening record through platforms like Robinhood. The crypto market is no different; from December 5, 2024, to February 4, 2025, during ETH's peak and subsequent drop, the ETH ETF had a cumulative net inflow of $3.2 billion, but as ETH entered a new round of decline, the institutions that bought the dip sold off their ETH ETFs. Interestingly, after the institutions sold off, the market began to rebound. Therefore, in many cases, institutions also make the mistake of chasing highs and cutting losses.

On May 14, ETH fell by 2.6%, but ETH ETF saw an inflow of $63 million, suggesting that some institutions that missed the opportunity began to rebuild their positions as prices corrected. If the net inflow of ETH ETF funds expands further in the next 2-3 days, then the institutional 'wrong-way' trend may begin.

Although the logic supporting ETH's trend reversal is still weak, the fundamental and financial improvements brought by the Pectra upgrade can at least support Ethereum returning to a valuation range of $2,800 to $3,200. Therefore, investors with costs below $2,800 will definitely not be caught in a long position in the medium to long term.