The information, views, and judgments regarding the market, projects, cryptocurrencies, etc., mentioned in this report are for reference only and do not constitute any investment advice.

The information, views, and judgments regarding the market, projects, cryptocurrencies, etc., mentioned in this report are for reference only and do not constitute any investment advice.

Written by 0xBrooker

The Federal Reserve's interest rate cuts and liquidity release have raised the bottom price of BTC this week; disappointing earnings from AI tech stocks continue to squeeze the valuations of high beta assets, suppressing BTC's upward space. Ultimately, after testing last week's high, BTC continues to maintain a mid-term 'bottom-fishing' trend.

ETH, which had previously fallen more sharply, rebounded more strongly, but ultimately also fell back with the overall trend.

Under the influence of interest rate cuts and slight improvements in short-term liquidity, both attempted to break through the downward trend line this week, but ultimately returned without success, falling back within the upper edge of the downward trend line.

Overall, BTC maintains a synchronized rise and fall with the NASDAQ, waiting for the release of next week's November CPI and non-farm employment data to provide guidance for a market lacking trading points, while also facing the impact of next week's interest rate hike in Japan.

Policy, Macro Finance and Economic Data

After a rollercoaster ride that has severely impacted BTC's upward momentum, the Federal Reserve's November meeting is set to cut rates by 25 basis points to 3.50%~3.75%. The Federal Reserve's statement emphasizes that regarding the 'dual target risk trade-off', the downside risk on the employment side has increased, while inflation 'remains slightly elevated'; future decisions will depend on data, outlook, and risk balance to determine the 'magnitude and timing of further adjustments'. This indicates that the Federal Reserve is currently slightly leaning towards the employment side in its dual mandate.

This somewhat dovish statement was diluted by discord within the Federal Reserve—9 in favor, 3 opposed (1 advocated for a 50bp cut; 2 advocated for no rate cut).

The dot plot for 2026~2028 is clearly more dispersed, indicating that the trade-off between 'inflation stickiness vs. employment slowdown' is inconsistent; the points on the right side for 'Longer run' are concentrated around the 3% range, slightly above 3%, indicating that the long-term neutral interest rate may have higher policy implications than before the pandemic. This will lower the expected rate cut in 2026 to 1-2 times, totaling 50 basis points. This is a neutral guidance that may help employment to some extent, but under the current circumstances, it is insufficient to support high β assets.

In response to short-term liquidity tightness, the Federal Reserve has resumed short-term government bond purchases and explained at a press conference that it will conduct RMP to maintain 'ample reserves', with approximately $40 billion in the first month, emphasizing that RMP does not mean a change in the monetary policy stance. The first bond purchase has been completed.

After more than a month of valuation destruction, high β assets represented by AI tech stocks have not stabilized. This week, the earnings reports from Oracle and Broadcom once again shook market confidence.

After a spending expansion in Q3 drove stock prices up, the market is now more concerned about the debt issues of AI stocks and whether high investments can quickly translate into profit growth. The release of two earnings reports has created a 'soft and hard' double blow, leading the market to reevaluate the 'AI return rate realization cycle', causing AI heavyweight stocks to drag down the NASDAQ and overall market risk appetite. Nvidia and BTC have both lost their rebound gains, returning to the starting point of this week.

The 10-year U.S. Treasury yield remains around 4.18%, putting pressure on high-duration assets.

Although the Federal Reserve has begun purchasing bonds and the Treasury's TGA account has started to decline due to spending, SOFR has returned to within the federal funds rate range, and short-term liquidity is gradually easing, it is still not abundant. Against the backdrop of doubts about the debt and profit returns of AI stocks, there are signs that capital in the U.S. stock market is shifting towards consumer and cyclical stocks. The Dow Jones and Russell 2000 indices both reached new highs this week.

Against the backdrop of unclear interest rate cuts in 2026, coupled with the fact that the new chair of the Federal Reserve has not yet been determined, high β assets, including AI tech stocks and BTC, have still not received favor from investors. The most optimistic estimate is that after next week's interest rate hike in Japan and the release of U.S. employment and inflation data, the market may open up a 'Christmas rally.'

Crypto Market

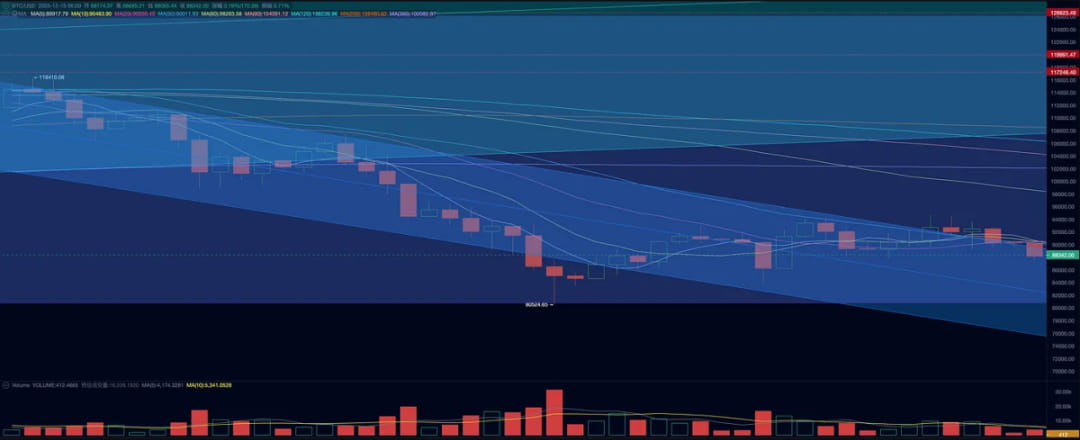

This week, BTC opened at $90,402.30, closed at $88,171.61, with a decline of 2.47%, a fluctuation of 7.83%, and a slight shrinkage in trading volume. Technically, BTC temporarily broke through the downward trend channel before the interest rate cut, but was completely reversed due to the impact of AI stock earnings reports.

BTC Price Trend (Daily)

Currently, BTC is still in a phase of platform consolidation after a significant drop. Whether it will rebound upwards along with U.S. stocks to establish a 'new cycle,' or crash again after consolidation to continue the decline and solidify the 'old cycle,' still depends on the interplay of internal and external factors and the reactions of various market participants.

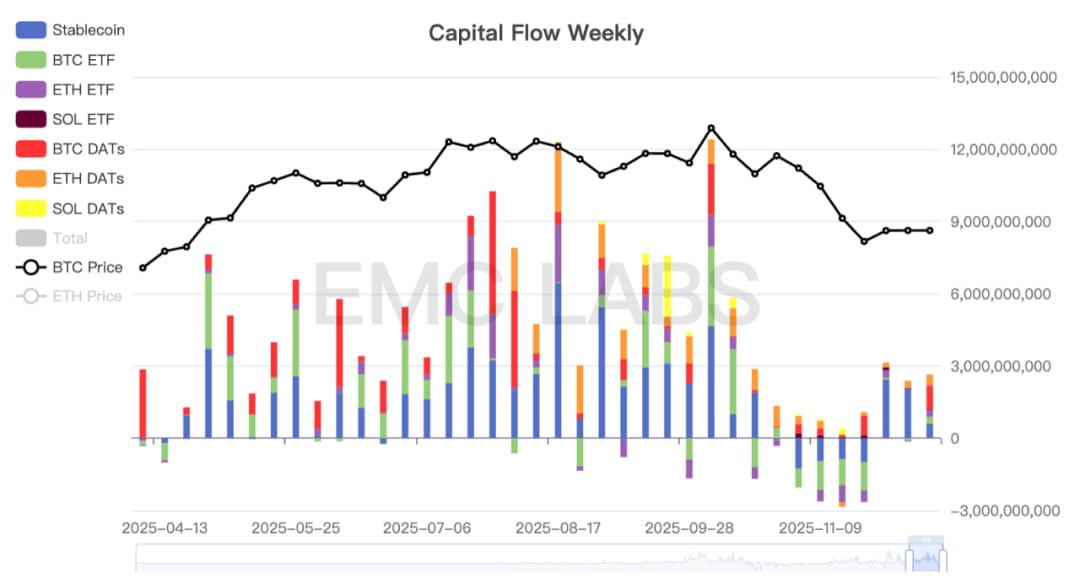

In terms of funds, the situation is relatively optimistic. Statistics show that there has not been a significant change in capital inflows this week, but last week, Strategy made a significant increase of over $900 million in BTC holdings, and Bitmine also significantly increased its ETH holdings, which undoubtedly boosted market confidence.

Crypto Market Fund Inflow and Outflow Statistics (Weekly)

Among them, BTC ETFs and ETH ETFs, which have significant pricing power over crypto assets, both recorded positive inflows, totaling over $500 million.

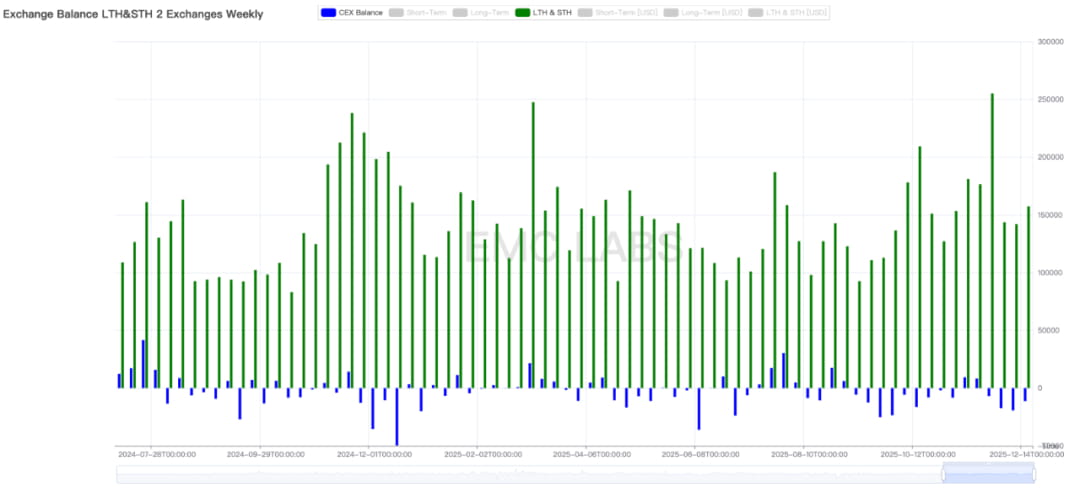

In terms of selling, the situation is slightly pessimistic. Last week, a total of over 157,000 units were sold by both long and short positions, exceeding the scale of the previous two weeks. Additionally, as selling increases, there has also been a slight decrease in the outflow from exchanges.

Exchange Selling and Inflow/Outflow Statistics (Weekly)

Exchange Selling and Inflow/Outflow Statistics (Weekly)

Meanwhile, long positions continue to sell off. The historical cycle curse still profoundly affects this group. If they cannot return to an accumulation state, the price of BTC is unlikely to stabilize.

There are also favorable advancements at the industry level. The CFTC has announced the launch of a digital asset pilot program, allowing regulated derivatives markets to use BTC, ETH, and USDC as collateral, accompanied by stricter monitoring and reporting mechanisms. The breakthrough of crypto assets as margin in derivatives scenarios is beneficial for the integration of DeFi and CeFi, increasing the application scenarios for Crypto, which is a long-term positive for Crypto. Moreover, the much-watched 'structural proposal' has also been reported by the media to have gained some traction, receiving unanimous support from both the Democratic and Republican parties. The final passage of this bill will benefit the further development of the crypto industry in the U.S. and will promote institutional allocation towards crypto assets.

Cycle Indicator

According to eMerge Engine, the EMC BTC Cycle Metrics indicator is 0, entering a 'downward period' (bear market).

EMC Labs (Yongxian Laboratory) was established in April 2023 by crypto asset investors and data scientists. It focuses on blockchain industry research and crypto secondary market investment, with industry foresight, insights, and data mining as core competencies, aiming to participate in the booming blockchain industry through research and investment to promote the welfare of humanity through blockchain and crypto assets.

For more information, please visit: https://www.emc.fund