In fact, UNI can be considered a veteran in the cryptocurrency world and is recognized as a pioneer of DEFI. Uncle Meow first paid attention to UNI back in 2020, when DEFI protocols had not yet 'emerged'. Later, the launch of UNI directly changed everything, turning the cryptocurrency space from one focused on speculation over value into a true financial innovation island.

After UNI went live, various DEFI protocols appeared in the market, such as SUSHI, BAL, PANCAKE, etc., which are essentially upgrades and variants of UNI.

Subsequently, the UNI project team continued to innovate, transforming the low capital efficiency of broad liquidity market-making mechanism into the high liquidity narrow range mechanism of V3, and later to the customizable HOOK of V4. Each step has indeed been precisely on the path of DEFI innovation.

However, as the ancestor of DEFI, the performance of UNI's token has been very lackluster. The main reason is that the token empowerment is too weak. The UNI team focuses on optimizing the project. The DLMM of V3 and V4HOOK are indeed highly innovative, and recently UNICHAIN has further elevated the UNI project into the public chain track, broadening the tolerance for token valuation. However, after the bear market of 2022, the UNI token has not shown improvement, and people's views on UNI are more akin to 'a worthless mascot' rather than 'the stock of the project', until the repurchase mechanism of the UNI token was set in November, which changed the market's perspective.

UNI's Launch

The first version of Uniswap (v1) started operating in November 2018 (launched at DevCon 4), the second version (v2) was released in May 2020, and the highly anticipated third version (v3) was launched in March 2021. At the same time, Uniswap supports various Ethereum scaling solutions such as Optimism, Arbitrum, and Polygon. Uniswap is recognized as a pioneer of decentralized exchanges (DEX), first for promoting the constant product pricing curve X*Y=K in V2, and later for implementing concentrated liquidity and tiered trading fee functionality in V3. Since then, many other DEXs have adopted the constant product pricing curve. So, UNI is the ancestor of DEFI.

Battle with SUSHI for the top spot

In August 2020, Sushiswap launched as a fork of Uniswap, initiating a 'vampire attack': Uniswap LPs could stake Tokens to earn SUSHI rewards, and liquidity was automatically migrated.

Within a week, nearly $2 billion in Uniswap LP flowed into Sushiswap, bringing SUSHI's market cap close to $300 million. Sushiswap quickly grew and weakened Uniswap's dominance.

Uniswap LP relies solely on transaction fees and is vulnerable to impermanent loss; Sushiswap LP receives SUSHI incentives in addition to transaction fees and continues to enjoy dividends after withdrawal. In September, Sushiswap's TVL surpassed Uniswap, siphoning off 70% of its liquidity. Uniswap was forced to fight back, issuing UNI airdrops to early users in the same month and opening mining for the four core pools (USDT/ETH, USDC/ETH, DAI/ETH, WBTC/ETH). Liquidity quickly returned, TVL reached new highs, successfully consolidating its throne.

Therefore, the purpose of the UNI token's birth seems more like an airdrop gift for users, initially just used as a reward. However, the increasing heat of the DEFI track has also caused the UNI token to rise significantly, with an increase of up to 5000% that year, but it has not shown much improvement since the bear market until now.

In November, the UNI token mechanism was upgraded to include repurchase.

The upgrade of the UNI token is a key focus for everyone, as it seems the project team wants to turn this 'mascot' into a true 'value capture device'.

Past UNI token value:

Value Source: Only trading matching (AMM), with no systematic value reflow back to the token (concern over regulatory risks of dividend-style designs).

Governance Token UNI: Weak Value Capture (has governance rights, no real income anchor).

Post-upgrade UNI token value

Value Source: Diversification and 'Internalization'

Trading Protocol Fees (v2/v3/v4)

Unichain (Sequencer Fees)

MEV Internalization (PFDA)

External Liquidity Aggregation Fees (Aggregator Hooks)

Value Reflow Method: Unified Entry to Destruction Pool → Deflationary

Governance Token UNI: Strong Deflation + Strong Alignment

Therefore, in November, after announcing this repurchase upgrade, the token price of UNI increased by over 50%, proving that a significant part of the current value of the token comes from the project's positioning of its own token.

UNISWAP On-chain Data

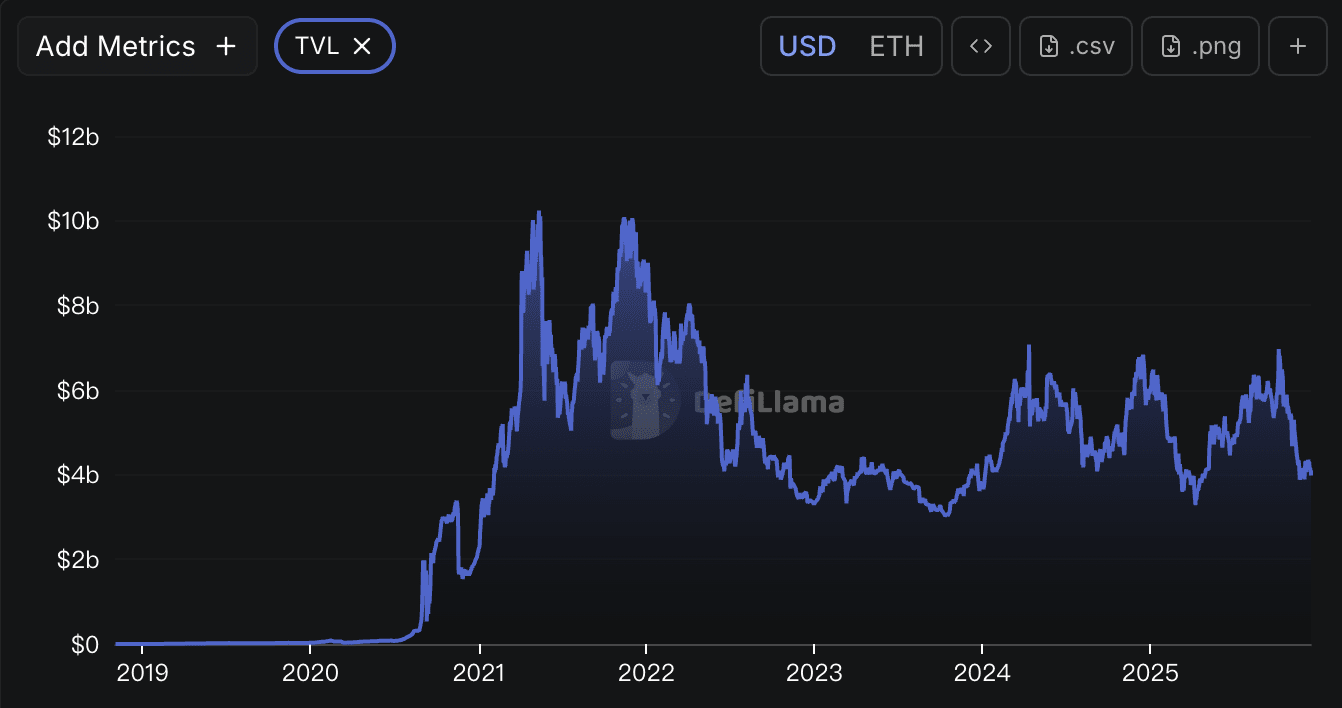

1. TVL (the most basic reflection of project value)

Currently, the TVL is around 4B and relatively stable, with no strong expectations for growth or decline.

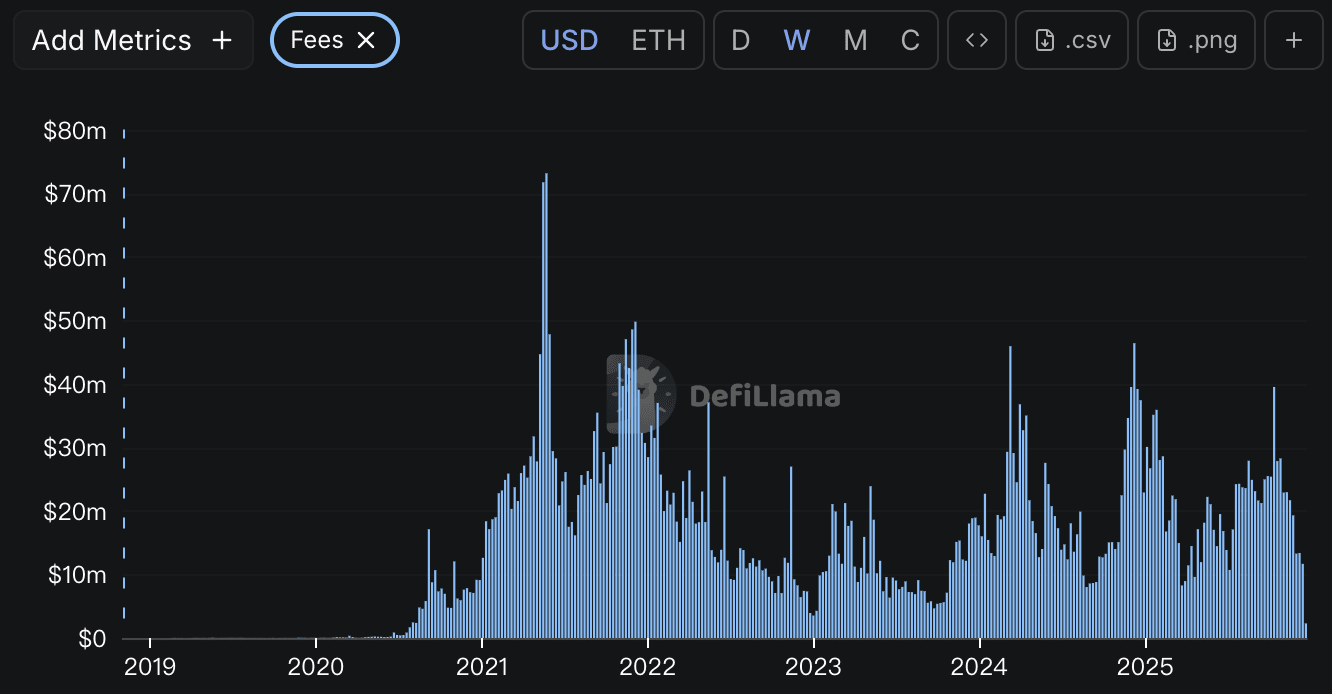

2. FEES (which can reflect user activity levels)

Current data shows a downward trend compared to October, indicating overall trading users' sentiment is low.

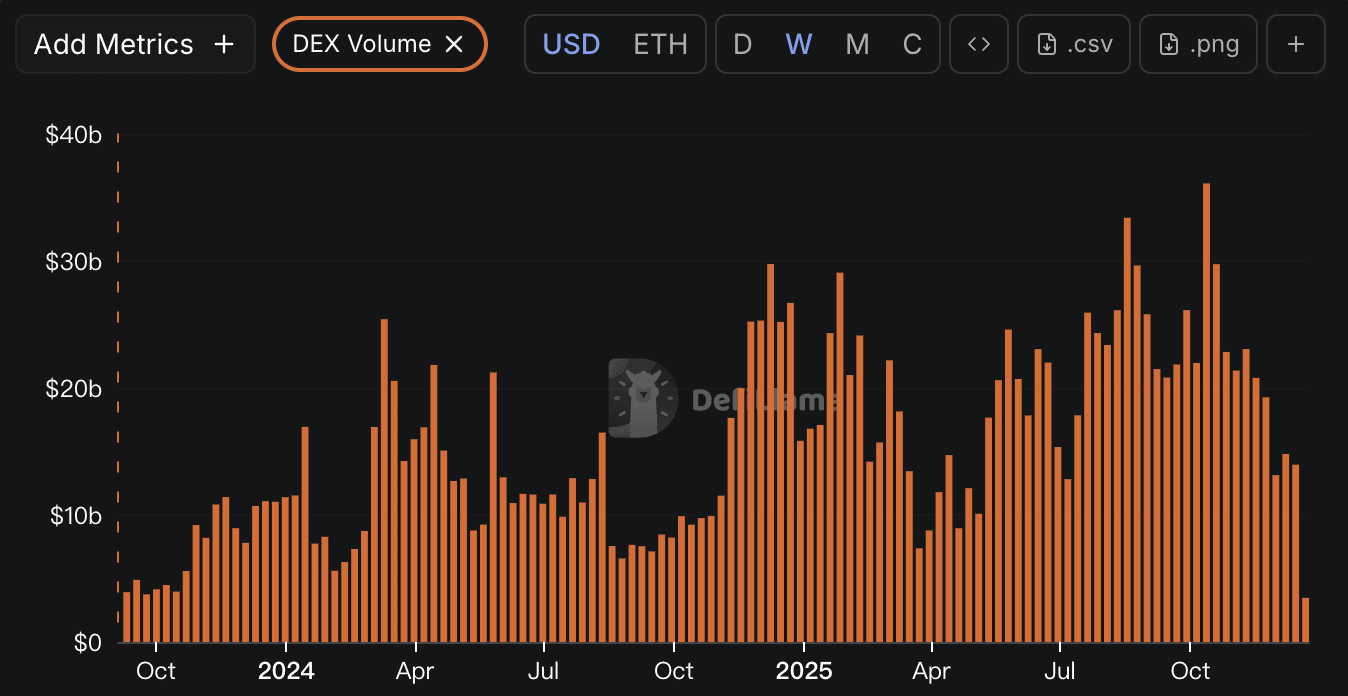

3. DEX Volume

Trading volume has dropped significantly due to the loss of liquidity.

Overall on-chain data shows that the on-chain performance of the UNI token has been very stable. It is currently also a leading DEFI project and has user stickiness (a DEFI project with top security). The benefits of this token upgrade need time to materialize.

Meow Uncle's Follow-up Views on UNI

I used to be very bearish on UNI. At that time, when UNICHAIN launched, it did not empower the UNI token as GAS, and I once thought the UNI project team had given up on the UNI token, so I did not hold any UNI. It was only after the repurchase plan was announced two months ago that it truly showed a willingness to empower the token.

Although this retrospective plan is unlikely to boost the token price in the short term, after all, there are too many trapped positions above, and users' views on DEFI tokens have not changed significantly from 2023 to now. No matter how well the project is done, its value is hard to reflect in the token price.

However, since there is an upgrade plan, it proves that the project team has not given up on its own token. If the UNI token truly wants to soar in the future, it still depends on the subsequent repurchase efforts, and more on the project's trading volume, FEE, TVL, and other data, as the fundamentals are the cornerstone of a token's value.

In the later bear market, I believe adding UNI to a dollar-cost averaging plan is a relatively reasonable investment logic. Currently, the price of UNI has also fallen back to the bear market low of 2023. We can wait for a true emotional low period to focus on the actual price low.