Sober Options Studio × Derive.XYZ Joint Production

Written by Sober Options Studio Analyst Jenna @Jenna_w5

I. Macroeconomic Barometer: Increased Certainty of Interest Rate Cuts, Sino-U.S. Rebound and Year-End Uncertainty

Last week, the core theme of the market was the evolution of interest rate cut expectations from 'uncertain' to 'almost certain.' This increased certainty, along with positive signals from Sino-U.S. trade relations, jointly propelled a mild market rebound. However, in the face of liquidity tightening and policy decision risks at the end of December, the market still needs to remain cautious.

Increased Certainty of Interest Rate Cuts: From Uncertainty Shock to Market Rebound

Last week, the market experienced volatility triggered by uncertainty over rate cuts, followed by stabilization and recovery after expectations became clearer.

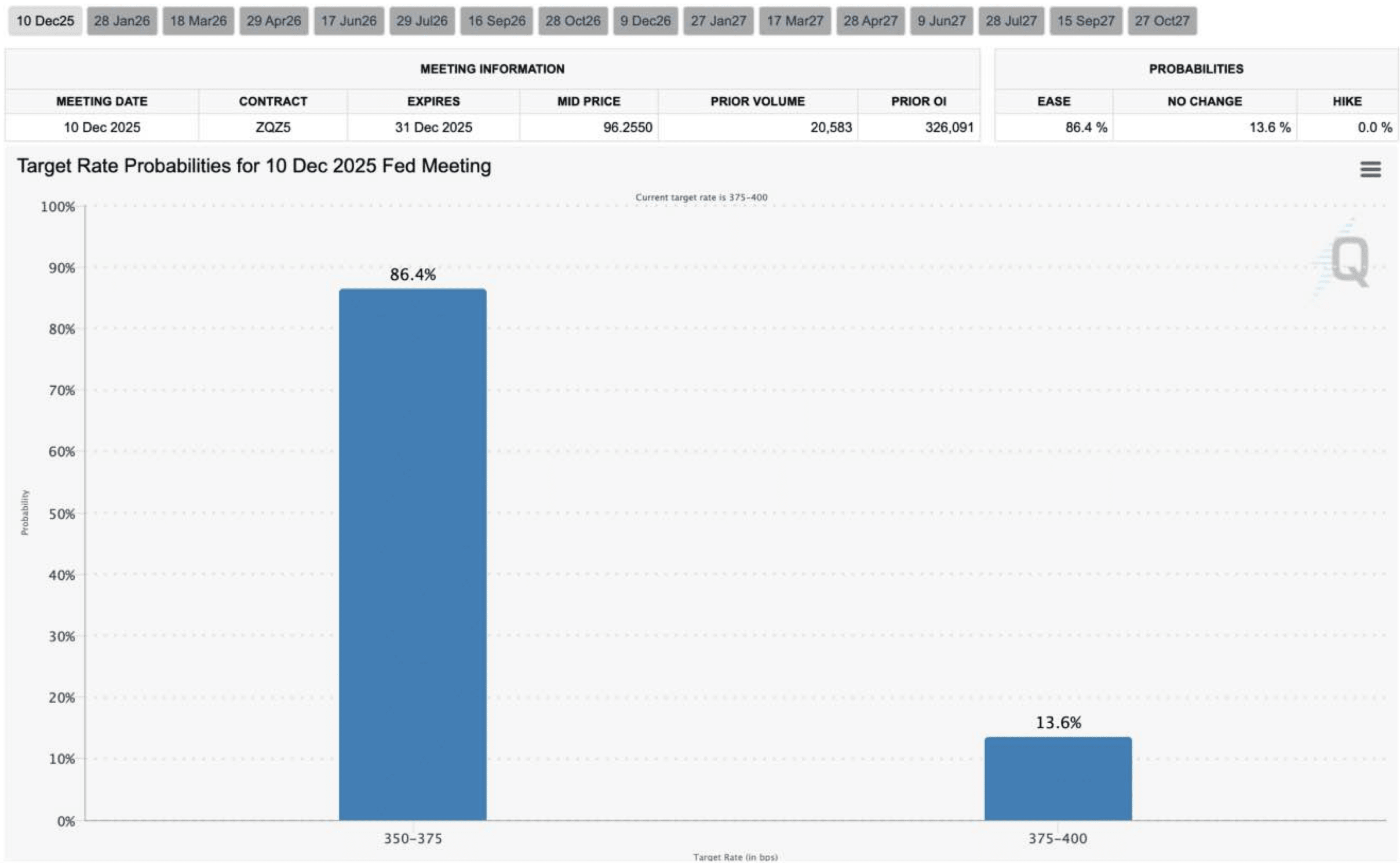

Background review: Previously, although the Federal Reserve had completed two rate cuts, the market's expectation of 'whether there will be a third rate cut this year' fluctuated between 50% and 70%, due to the U.S. government shutdown getting caught in a 'data fog.' This uncertainty has pushed up short-term risk premiums and intensified market volatility. Last week, according to CME Group FedWatch futures data, the market's expectation of another rate cut on December 10 has risen significantly to 86%, an increase of 15 percentage points from the previous week, indicating that rate cut expectations have become significantly aligned.

Market impact: The stability of rate cut expectations brings positive effects. As the policy path becomes clearer, short-term uncertainty premiums rapidly decline, leading to a rebound in market risk appetite, and asset prices such as cryptocurrencies gradually stabilize and rebound. The increase in certainty lays the foundation for a short-term recovery in the market.

The continuous warming of U.S.-China relations: The decline of risk premiums.

The positive progress in U.S.-China trade relations is another important pillar for the recovery of risk assets this week.

Policy dynamics: On November 26, following the U.S.-China summit call, the U.S. Trade Representative's office announced an extension of the tariff exemptions related to China's technology transfer and intellectual property under 'Section 301' to November 10, 2026.

Market significance: The extension of tariff exemptions effectively reduces the risk of further escalation of global trade frictions, thereby leading to a decline in macro systemic risk premiums. This move not only strengthens the valuation support for global risk assets but also has a positive effect on stabilizing the implied volatility of the medium- to long-term options market.

Year-end 'reefs': Liquidity constraints and Supreme Court rulings.

Although short-term sentiment has warmed, there are still two major uncertainties to closely monitor before the end of the year:

Liquidity is tightening: Every December, affected by Christmas and New Year holidays, institutional trading activity decreases, and market liquidity typically shrinks. A decrease in trading depth may amplify the impact of unexpected events on prices.

The Supreme Court is about to rule: The U.S. Supreme Court will make a ruling in December on the legality of former President Trump's implementation of large-scale reciprocal tariffs. Currently, conservative justices hold a majority, and some judges have previously expressed doubts about the legality of tariffs. The ruling will have far-reaching implications for the future direction of trade policy:

If the ruling deems the tariffs illegal, it will further stabilize market expectations;

If it supports the existing policy, it may reignite medium- to long-term policy uncertainty and raise corresponding risk premiums.

In summary, the current market recovery mainly benefits from the dual short-term positives of 'aligned rate cut expectations' and 'periodic easing of U.S.-China relations.' However, the natural tightening of liquidity at year-end and the pending tariff ruling by the Supreme Court remain potential tail risks. It is recommended that investors remain vigilant amidst optimism and adopt a strategy focused on defense and risk control.

II. Deep analysis of BTC & ETH options market data.

Combined with chart data provided by Amberdata & Derive.XYZ, the significant changes in market sentiment this week are reflected in the decrease of short-term IV and the normalization of the term structure, thanks to the certainty of macro rate cut expectations. However, the continued deep negative skew and deeply negative structure of VRP remind us that the demand for downside hedging has not faded, and pure selling strategies remain highly risky.

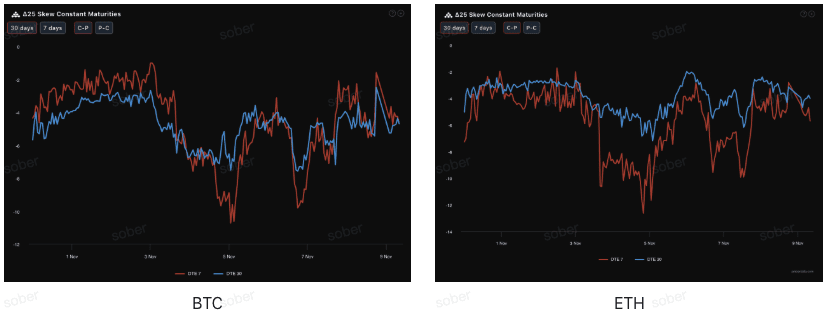

Skew: The negative range narrows, reflecting a mild improvement in sentiment.

Observing through Delta 25 Skew (implied volatility IV of call options - IV of put options), the magnitude of the negative value reflects the market's hedging demand for downside tail risks.

Normalization of deep negative values: The 25 Delta skew of BTC and ETH remains in the negative range, indicating that the demand for put options is still higher than that for call options, and the market continues to guard against tail downside risks. Compared to before, the magnitude of the negative skew has narrowed, reflecting a decrease in put option premiums, alleviating short-term panic, consistent with the improvement in macro sentiment.

Term structure: Both short-term (7 days) and medium-term (30 days) skews remain negative, with a greater correction in short-term skew, indicating that market concerns about near-term risks have eased, but the overall structure remains defensive.

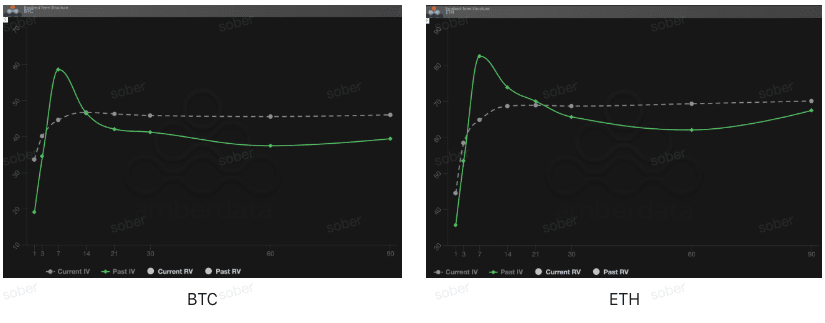

Term Structure: Presenting a 'hump' shape, focusing on FOMC event risk.

From the perspective of term structure, last week, the implied volatility curve of BTC and ETH was not in the typical Contango (near low, distant high) shape but showed a significant increase in near-term IV and a 'humped' structure with the distant end remaining high.

Curve anomaly: The current implied volatility curve is not in a standard Contango shape but shows a clear 'hump' around the 7-day mark, indicating that the market is pricing in the results of the December FOMC meeting.

Event-driven IV surge: Current IV is significantly higher than Past IV (green solid line) on the short end. This is not a normal market state but a typical 'event hedging' mode. The market is madly buying short-term options around the December interest rate meeting, leading to a significant increase in near-term IV. This structure often appears before major uncertainty events (the 'data blind box' interest rate meeting at this time).

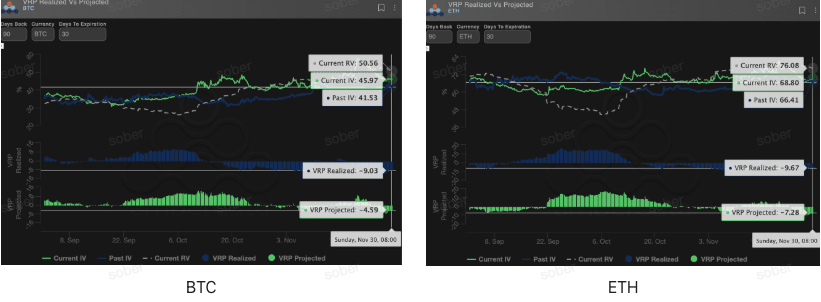

Volatility Risk Premium (VRP): Continues to be negative, and seller risk remains high.

VRP (Volatility Risk Premium = Implied Volatility IV - Realized Volatility RV) is an important indicator for measuring whether options pricing is reasonable. The current market is in a correction phase. Although IV has risen significantly to correct pricing deviations, the structural divergence of VRP data reveals potential risks: historical actual volatility far exceeds expectations, and the current high premium, seemingly attractive, may still be insufficient to cover future tail risks.

Realized VRP (Realized) deep negative alert: Realized Volatility (RV) continues to be higher than Implied Volatility (IV), leading to VRP being in deep negative territory, indicating that options pricing has not fully covered actual volatility risks.

Projected VRP turns from positive to negative: Projected VRP has turned from positive to negative, indicating that the market's expectations for future 30-day volatility are also becoming cautious. In a deeply negative VRP environment, naked selling options strategies are significantly risky, and it is recommended to adopt buying or risk-controlled spread strategies to cope with potential volatility.

III. Recommended options strategy: Bear Put Spread to lock in downside risks.

Based on the current macro uncertainty dissipating but year-end liquidity risks still persisting, continued deep negative skew, and deeply negative VRP market environment, we recommend using Bear Put Spread for defensive positioning.

Strategy objective:

Defend against potential downward risks triggered by year-end liquidity constraints.

Limit risks and costs, avoid the risks of deeply negative VRP for naked sellers.

Fully utilize the high premium of put options brought by deep negative skew to achieve low-cost entry.

Strategy construction (taking BTC/ETH as an example):

Buy a put option with a higher strike price, slightly out of the money (Slightly OTM) (Long Put).

Sell a put option with a lower strike price and the same expiration date (Short Put).

Expiration date choice:

Considering the impact of the Supreme Court ruling in December and the tightening of year-end liquidity, it is recommended to choose mid-term contracts with DTE of 30 days or 60 days to cover the entire uncertainty window.

Core advantage:

By selling puts with low strike prices to collect premiums, significantly reducing the cost of buying puts while locking in the maximum loss as the net premium expenditure. This is more cost-effective than directly buying put options (Long Put).

The current skew remains deeply negative, and selling puts can yield high premiums, further optimizing the profit and loss ratio of the spread.

IV. Disclaimer

This report is based on publicly available market data and options theoretical models, aiming to provide investors with market information and professional analytical perspectives. All content is for reference and communication purposes only and does not constitute any form of investment advice. Cryptocurrency and options trading have extremely high volatility and risks, which may lead to the total loss of principal. Before adopting any trading strategy, investors should fully understand the characteristics of options products, risk attributes, and their own risk tolerance, and must consult professional financial advisors. The analysts of this report bear no responsibility for any direct or indirect losses arising from the use of the content of this report. Past market performance does not predict future results; please make rational decisions.

Jointly produced: Sober Options Studio × Derive.XYZ