What truly stops you from making money in this world is not the environment, not the market,

Instead, it's that thought in your heart: 'Forget it, I'm not worthy.'

Arthur Hayes' family office criticizes Pantera: 100000 turned into 56000, exposing the harsh truth of crypto funds

The hottest insider news in the crypto world recently is not about a certain project skyrocketing,

Rather, it was Akshat Vaidya, the investment director of Arthur Hayes' family office Maelstrom, who personally stepped out to criticize Pantera Capital—with actual loss data to back it up.

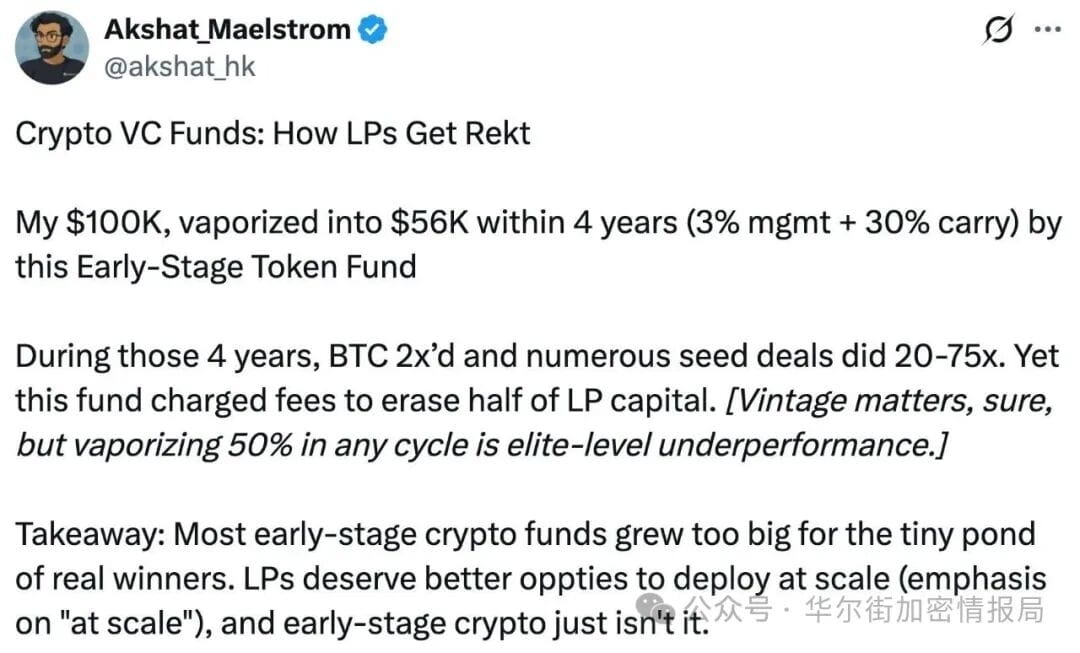

He revealed on X (formerly Twitter): Four years ago, he invested 100000 USD in Pantera's Early-Stage Token Fund, and now only 56000 remains, a 46% reduction in value.

What's more heartbreaking is: "During the same period, Bitcoin rose by 2 times, many crypto startups 20-75 times, while the fund I invested in lost half."

When this statement was made, the whole industry was in an uproar. Today, we will use this incident to help you see the truth about crypto funds, the issues in the industry, and the hidden worries of the next cycle.

01 | 100,000 turning into 56,000: The real returns of crypto funds.

This was the first time being publicly torn apart.

According to reports from several official media (Sina Finance, Weex, CryptoNewsZ, Odaily):

Akshat invested $100,000 LP share in Pantera, and after 4 years, the residual value is only $56,000, losing nearly half. How did the market perform during the same period?

Bitcoin doubled, many early projects increased by 20-75 times, and ETH and BNB strengthened.

However, Pantera's fund not only lost money but also underperformed the market, mainstream assets, altcoins, early-stage projects, and everything.

Why is this happening? Vaidya directly gives three core reasons:

02 | "The larger the scale, the worse the returns":

Akshat reveals the hidden rules of crypto funds.

Akshat stated very clearly: "Blockchain has no scale effect. The larger the fund, the harder it is to achieve high returns."

Why?

Reason one: The number of quality early-stage projects is limited.

Excellent Web3 startup teams are not numerous. And venture capital giants like Pantera raise funds in the hundreds of millions of dollars, to spend the money: they need to invest in more projects, relax standards, and take on some projects with high late-stage valuations.

The result is that the average return rate is diluted.

Reason two: "Large funds" mean slower and more conservative.

Small funds dare to go all in on 20x projects, while large funds can only choose "stable projects" — but stability often doesn't explode.

Crypto is an industry that completely disregards stability.

Reason three: Structural contradictions: Fund sizes are growing, but high multiple opportunities are not increasing.

Scale expansion → Money is hard to spend: Limited opportunities → Can't achieve high multiples: High fees → Eat away returns.

So the result turned into Vaidya's accusation: "This is an industry that is not accountable to LPs."

03 | The behind-the-scenes killer that kills LPs:

It's that notorious "3/30," what Vaidya is most dissatisfied with and criticizes the most is Pantera's fee structure: 3% management fee + 30% performance fee.

This is much more expensive than the traditional venture capital "2/20." What impact does it have on LPs?

① Many years of management fees directly swallow the principal.

4 years = 12% management fee, if the project doesn't perform, the management fee will first consume a chunk of the LP.

② Performance fees with repeated commissions will dilute returns.

As long as the project rebounds a little, the fund can "lock in profits." If the project falls back, the losses are borne by the LP.

③ This is a type of "bull market fee structure."

What was reasonable in a bull market becomes a way to cut leeks in a mediocre cycle.

No wonder Vaidya would publish a complaint.

04 | This round of bull market only saw BTC, ETH, and BNB rise.

If altcoins don't rise, funds can't survive. Why is this round of bull market generally "very miserable" for institutions?

Because this round of market has an unprecedented feature: BTC is surging → Altcoins are collectively lying flat.

Including: some funds from a16z, Pantera, Multicoin, and Paradigm have been dragged down by the weakness of altcoins.

The reason is simple: early-stage funds rely on multiples to survive.

Instead of stable growth, they need: 30x, 50x, 100x.

But this round of altcoins overall did not have "chaos", most projects: did not launch, did not list, did not have liquidity, did not have narratives, did not have token growth.

Without these multiples, the fund's performance is naturally poor.

Some analysts even directly said: "If altcoins don't rise, many funds won't survive this cycle."

This is the cruel reality of the industry.

05 | Another harsh truth: Many funds are now struggling to raise capital.

The well-known Asian fund you mentioned, ABCDE, exited the crypto space this year, which is not an isolated case.

The entire industry is experiencing: LP tightening, institutional fundraising difficulties, altcoin freezing, declining yields, high-cost structures that are difficult to maintain.

In other words: the "money tide" of crypto funds is receding.

In the next few years, we may see a large number of funds collapse.

06 | But the story isn't that simple:

Akshat complains about Pantera while also promoting his new fund, yes, this is the most subtle point of the whole thing.

After Akshat complained about Pantera, he also promoted his family office Maelstrom and the new fund he is raising, focusing on crypto businesses that can generate cash flow in the real world, establishing a more reasonable and more cycle-resistant fund structure.

This is typical: both stepping on and lifting are for interests.

Even so, the questions he raised are still realities the industry must face.

07 | Final thoughts: This is a cycle reshuffling.

This is also a sign of industry maturity.

Vaidya's complaints reveal three truths to us:

Large funds ≠ High returns: Larger scale often means decreased efficiency.

High fee structures are no longer suitable for the current industry: LPs need a more reasonable way to align interests.

If there were no altcoin frenzy, the investment logic of funds would be reshaped: this is an industry structural upgrade. Future crypto funds,

It may lead to: more focus on cash flow, more focus on infrastructure, more emphasis on real users and income, less reliance on bull market speculation.

Perhaps this is the real beginning of the crypto industry maturing.

Conclusion

What you can't earn is not money, but cognition; what you can't overcome is not difficulty, but your old self.

Destiny is never something to wait for; it's something to choose.

Akshat's 100,000 → 56,000 is not just a tragedy for one LP, but a run on the entire crypto VC model; the collapse of the industry's return structure; and the reassessment of capital efficiency, with chain reactions after the weakening of the altcoin cycle.

In prosperous times, many problems are covered by the bull market. In cooling times, the problems truly reveal themselves.

This public "complaint" may prompt the entire industry to reflect:

In the next cycle, what kind of funds are truly worth holding for the long term?

In-depth observation · Independent thinking · Value goes beyond price.

Star #Wall Street Crypto Intelligence Bureau, don't miss good content ⭐

Finally: Many viewpoints in this article represent my personal understanding and judgment of the market, and do not constitute investment advice to you.