@Plasma has always felt like a good idea that never fully reached its potential. When it first appeared, it seemed like a big step forward—something built for real scalability—but the blockchain world wasn’t ready for it yet. Over time, other designs became more popular, but Plasma stayed in the background, steady and quietly holding on. It never disappeared; it simply waited for the right kind of demand to catch up. That demand is finally here, shaped by the renewed focus on payments, wallet infrastructure, and cross-border value movement.

The shift didn’t happen overnight. The industry spent years chasing generalized computation, pouring talent and capital into rollups that could mimic a full operating system on-chain. It was a necessary phase, but it also exposed a truth that’s easier to see in hindsight: not every use case needs that level of flexibility. Many of the world’s most practical financial interactions hinge on one simple requirement—fast, cheap, reliable transfers. Nothing more complicated than moving balances from one party to another with minimal friction. As soon as this became obvious, Plasma stopped looking like a relic of early research and started looking like a pragmatic foundation for real-world payment flows.

The renewed momentum isn’t driven by nostalgia. It’s driven by the realization that payment infrastructure becomes more compelling when it’s predictable. @Plasma s design, with its emphasis on state transitions that can be verified without replaying full execution traces, lends itself to systems that must be both efficient and resilient. It strips away complexity without sacrificing security. That alone makes it relevant, but the story continues further when wallets and cross-border corridors come into view.

Consider the daily reality of a business operating across several countries. Currency exposure, settlement delays, compliance checks, fragmented rails—these challenges aren’t abstract. They affect cash flow, payroll, vendor relationships, and long-term planning. A system that can move value quickly and at low cost doesn’t merely save money; it reshapes operational strategy. Plasma-based architectures, particularly the modern reinterpretations being pursued today, meet these needs with an elegance that other scaling designs rarely match. They offer the ability to batch transactions, preserve user sovereignty, and maintain a secure bridge to a base layer without forcing every operation to touch the global chain.

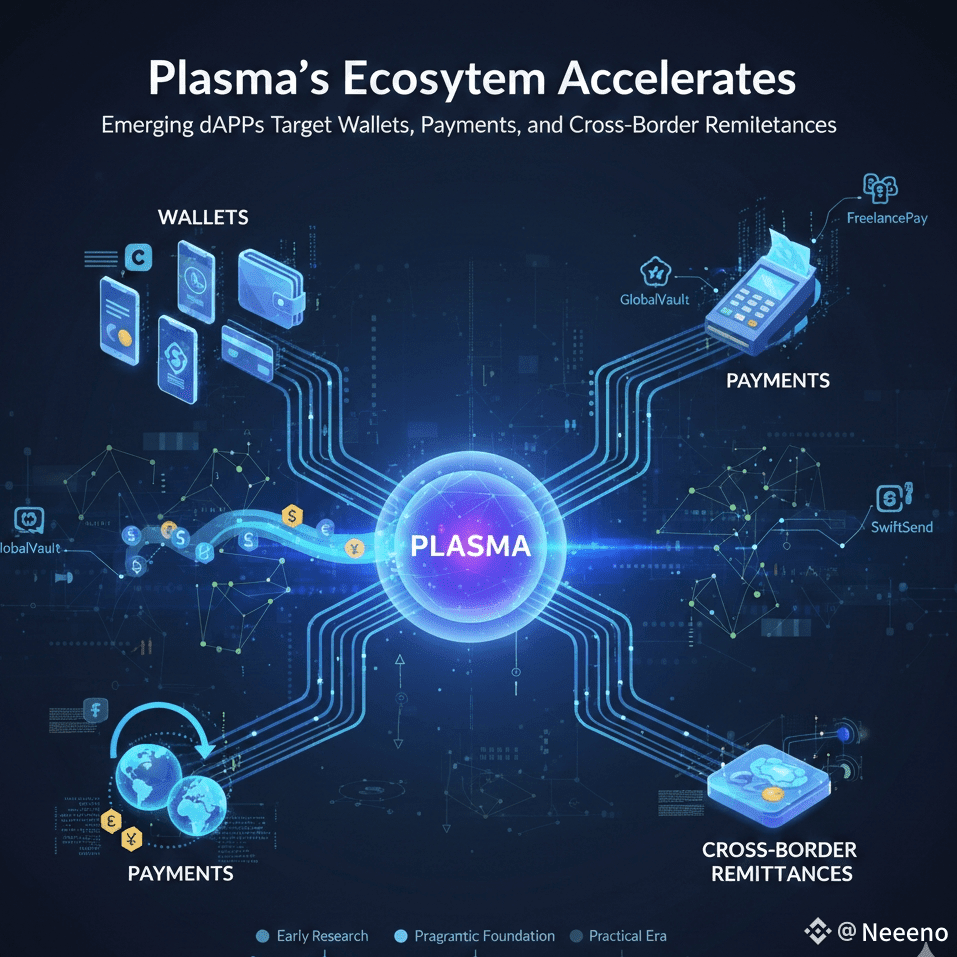

What makes this moment different is the maturity of the surrounding ecosystem. Wallets are no longer lightweight interfaces; they are evolving into full financial environments. Users expect seamless account recovery, consistent fee behavior, and instant settlement. Developers expect frameworks that let them build these experiences without navigating convoluted virtual machine logic. Payment-focused dApps expect rails that behave the same way every time. Plasma’s renewed role comes from its ability to support these expectations with a level of specialization that broader scaling frameworks struggle to match.

There is also a cultural shift underway.Here’s a simpler, clearer version:

Builders who once cared most about doing everything in the most flexible way are now focusing more on stability and smooth day-to-day operation. This doesn’t mean they’re giving up on new ideas — it just means they want those ideas built on systems that can handle normal use without issues. The renewed interest in Plasma fits perfectly with this way of thinking. . It allows for the creation of payment channels, micro-transaction layers, merchant solutions, and wallet-native settlement logic that behaves consistently in every environment. These are not experiments—they are stepping stones toward financial tools that people can actually depend on.

Cross-border transfers especially benefit from this clarity. When value needs to move between jurisdictions, the system’s guarantees matter more than its programmability. Banks and fintech companies care about traceability and finality. Here’s a simpler version:

Freelancers just want to get paid quickly without waiting on middlemen. Families sending money home care about speed, low fees, and knowing the transfer is safe. Plasma-based designs match these needs well — they give predictable withdrawals, easy-to-verify proofs, and big boosts in transaction capacity without making the user experience worse.

The conversation is no longer about Plasma versus rollups or Plasma versus any other scaling approach. The ecosystem has grown past those binaries. What matters now is matching the right tool to the right responsibility. Payments, wallets, and cross-border settlement happen to be domains where Plasma’s tradeoffs look less like compromises and more like advantages. The architecture is lean, but not fragile; flexible, but not overengineered. It brings a clarity of purpose that fits the moment.

As more teams build specialized payment flows and wallet abstractions, Plasma’s relevance becomes harder to ignore. What once felt like an unfinished chapter now feels like a framework entering its most practical era. The renewed attention isn’t a revival; it’s a rediscovery of what the architecture was always meant to do. And as the industry shifts toward a more grounded understanding of how digital value should move, Plasma’s simplicity and strength find their place again—quietly, confidently, and with a focus on solving problems that have been waiting for the right solution.