Three years ago, Curve Finance redefined the gameplay of DeFi liquidity wars with a voting custody mechanism (veCRV). Today, Lorenzo Protocol is bringing this script to the on-chain asset management field—but this time the stakes are higher, as the contest is not for the allocation rights of liquidity pool emissions, but for the allocation rights of billions of dollars in quantitative strategies.

💰 From Curve Wars to Asset Wars: The table has changed, but the logic remains the same

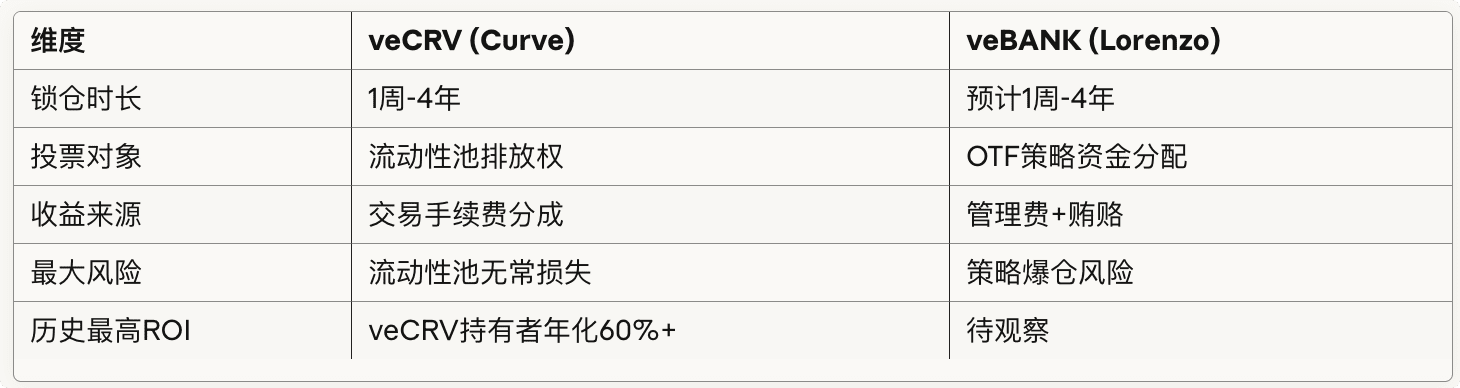

If you experienced the 'Curve War' of 2021, you will be very familiar with this model: Convex Finance aggregated the voting power of retail investors' veCRV and ultimately controlled nearly 50% of the governance power of the entire Curve ecosystem, with the voting influence of a single CVX token once reaching a 5x leverage. Protocols spent millions of dollars to 'bribe' CVX holders, just to have their stablecoin pools receive more CRV emissions.

Lorenzo's veBANK mechanism is essentially a clone of this flywheel's asset management version:

🔐 Lockup Period Design: Users stake BANK to obtain veBANK, the longer the lockup time (up to a maximum of 4 years modeled after Curve), the higher the voting weight. This is not a simple "lock-up mining," but rather a conversion of time commitment into strategic discourse power.

📊 Strategy Voting Rights: veBANK holders decide the capital flow of OTF (On-Chain Trading Fund). Assuming Lorenzo manages a TVL of $500 million, distributed across quantitative arbitrage, volatility strategies, and structured products in three OTF pools - the more voting rights one holds, the more funding their strategy pool can attract, leading to higher management fee income.

💸 Yield Enhancement Mechanism: Analogous to Curve's 2.5x boost, veBANK holders may enjoy protocol income sharing (such as 30% of management fees), priority access to whitelisting for new strategies, and even receive "bribery income" similar to Convex - a DeFi project pays tokens directly to veBANK voters to encourage Lorenzo to allocate more funds to its strategy pool.

⚙️ How does the flywheel turn? A data deduction.

Let me simulate the scenario of Lorenzo's ecosystem running one year later:

Initial State: Total supply of BANK is 2.1 billion, initial circulation is 425 million, unit price $0.05, market value approximately $21 million. Assuming Lorenzo manages assets (AUM) reaches $300 million, annual management fee rate is 2% (benchmarking traditional quantitative funds), annual income $6 million.

Step One - Lockup Incentives: The protocol allocates 40% of management fee income ($2.4 million/year) to veBANK holders. If you lock up 100,000 BANK (worth $5,000) for 4 years, assuming your veBANK voting share is 0.5%, you can receive $12,000 in protocol income each year - this is a nominal annualized yield of 240%, far exceeding simply holding the tokens.

Step Two - Strategy Competition: Three OTF strategy pools (Volatility Arbitrage Pool A, Market Neutral Pool B, CTA Trend Pool C) start competing for funds. The strategy providers in Pool A offer $5,000 worth of tokens each week to "bribe" votes from its veBANK holders to attract more allocations. If you allocate your voting rights to Pool A, you can earn an additional annualized bribe income of $52,000 (assuming Pool A needs to secure 30% of the total voting rights to attract $100 million in allocation).

Step Three - Flywheel Acceleration: As more funds flow into Lorenzo (due to the dual allure of strategy returns and governance income), AUM grows from $300 million to $1 billion, and management fee income simultaneously rises to $20 million per year. At this point, the yield share of veBANK rises from $2.4 million per year to $8 million, and the "implicit value capture" of a single BANK jumps from $0.0011 per year to $0.0038 per year - if the market assigns a 20x PS valuation, the theoretical price of BANK should reach $0.076, representing a 52% increase from the current price.

🎯 But this model hides three "time bombs"

⚠️ The Risk of Monopoly by Big Players: In the Curve ecosystem, the top 10 veCRV holders control over 40% of the voting rights. If a similar situation arises with Lorenzo, a few whale addresses could determine 90% of the capital flow - meaning the selection of OTF strategies would no longer be based on optimal returns but rather on "who bribes more." Worst case: A highly risky leveraged strategy receives large allocations due to sufficient bribes, ultimately leading to liquidation and chain reactions.

⚠️ The Prisoner's Dilemma of the Bribery Market: When "voting bribery" becomes the norm, strategy providers will fall into an arms race - even if a strategy has an annualized return of only 8%, they must allocate 5% to bribe voters, leaving only 3% for LPs. At this point, veBANK holders profit immensely, but the actual liquidity providers see their returns severely diluted, ultimately leading to capital outflow.

⚠️ The Fatal Paradox of Semi-Centralization: Lorenzo's quantitative strategies necessarily involve off-chain execution (high-frequency trading cannot be fully on-chain, block confirmation delays are fatal). If strategy providers commit malfeasance in off-chain operations (e.g., front-running, misreporting returns), veBANK voters cannot verify in real time - at this point, "decentralized governance" is merely superficial, and true power remains in the hands of strategy managers. The collapse of Three Arrows Capital in 2022 serves as a cautionary tale: even with well-designed governance tokens, failures in off-chain risk control can still destroy everything.

🔮 Three Price Path Predictions (Next 6 Months)

Path A - Flywheel Stalling ($0.02): If Lorenzo's AUM growth stagnates below $500 million, the management fee income cannot cover veBANK's yield promises, forcing the protocol to dilute tokens or reduce profit-sharing ratios, triggering a sell-off spiral. Probability: 30%.

Path B - Steady Growth ($0.08-0.12): Lorenzo successfully attracts 2-3 well-known market makers or quantitative institutions to join, with AUM exceeding $1.5 billion. The bribery market has begun to scale but is not out of control. The market value of BANK reaches the range of $30-50 million. Probability: 50%.

Path C - Escalation of War ($0.20+): A DeFi giant (such as Aave, Pendle) announces deep integration with Lorenzo, or a "Lorenzo version of Convex" second-layer protocol aggregates veBANK voting rights, triggering a frenzy of capital betting. Market impact of $100 million. Probability: 20%.

🧠 The Ultimate Question: Do investors really need "democratized" asset management?

In traditional finance, retail investors never vote to decide which stock BlackRock's fund managers should buy - because professional matters should be left to professionals. Lorenzo's veBANK model seems to empower the community, but it may actually evolve into "amateurs directing professionals": token holders may not understand the Sharpe ratio and maximum drawdown of quantitative strategies; they only care about who bribes more.

True innovation should be: using smart contracts to achieve "verifiable transparency" of strategies (such as publicly disclosing all transaction records on-chain and calculating risk indicators in real time), rather than dispersing decision-making power to potentially bribed and corrupted voters. Otherwise, Lorenzo is merely moving Wall Street's opaque operations on-chain, wrapped in a layer of "decentralization".

But that said, in a market where even meme coins can be pushed to a $1 billion market cap, who cares about logic? As long as the flywheel turns fast enough, leaving the scene before the music stops makes you the winner.