For bulls, the most important thing now is how long it will take for the market to rebound or even reverse. Since the official bear market began in 2022, the market has maintained a pattern. Every year at the beginning and end of the year, there is a foolish market, especially this year, where the foolish market at the beginning has been more intense. However, it has not arrived yet. What is hindering the annual cycle law, or has the cycle completely changed?

First, let's talk about the issue of market cycles. In fact, Bitcoin has shifted from a four-year cycle to a macro financial cycle, becoming a plaything of Wall Street rather than following its own halving cycle. More selling pressure and growth come from ETF selling pressure and purchases between institutions.

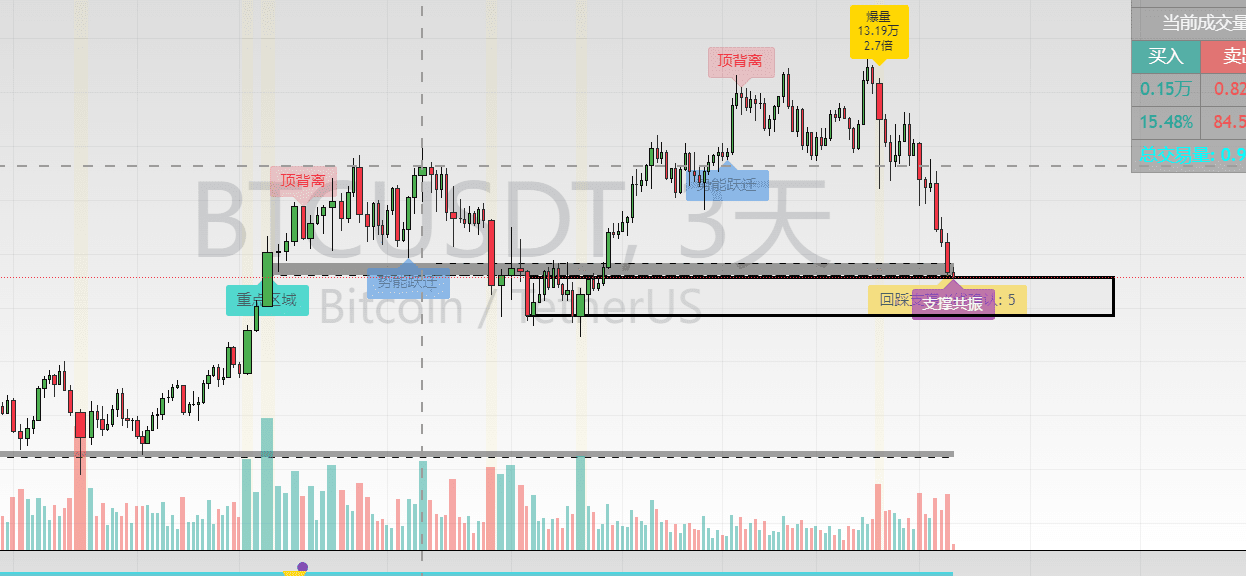

Technical aspect: Continued decline, but where might the real technical bottom appear?

At what position in the downward cycle will a certain amount of rebound be triggered? At least from today’s technical perspective, 85000 is a very important support level, but without a pin and buying volume, it feels a bit premature to call this position a bottom. Generally, I would try at critical positions in large cycles, but this time I am hesitant because there are no clear signs of a bottom from the smaller cycles.

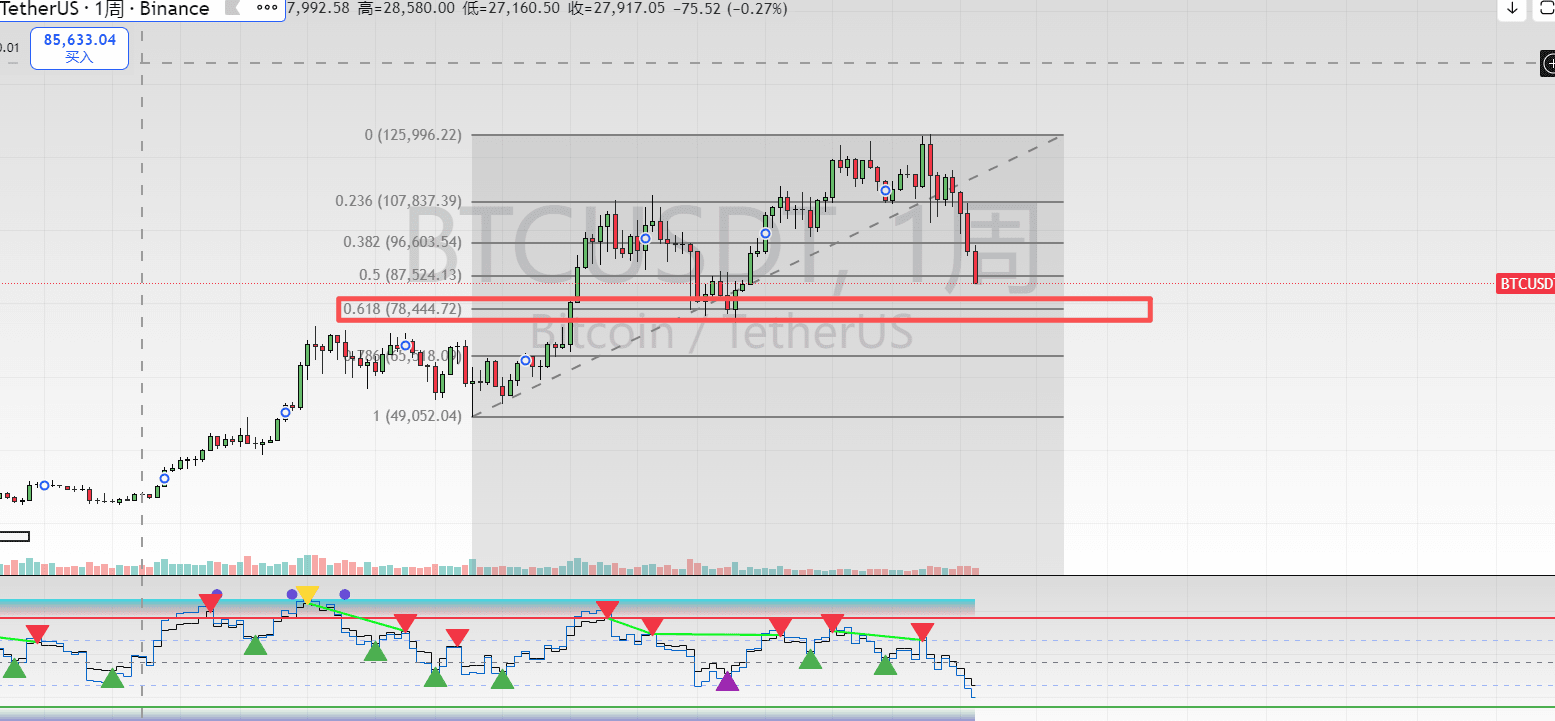

If we look at the technical side, around 78000 could be a huge opportunity, because there is a support near 78000 from the mining cost of miners outside the major Fibonacci 0.618 level. From the overall technical structure, the range of 85000-78000 is the key position for the entire bull market this year. Once it completely breaks down, the market enters a bear market. Even if it does not break down, if it breaks 85000, touches 78000, and then rebounds, the entire market will not see a V-shaped recovery, but will instead experience a very long period of bottoming and consolidation.

Macroeconomic structure: The liquidity withdrawal has ended, and the easing is approaching, but where has the current liquidity gone?

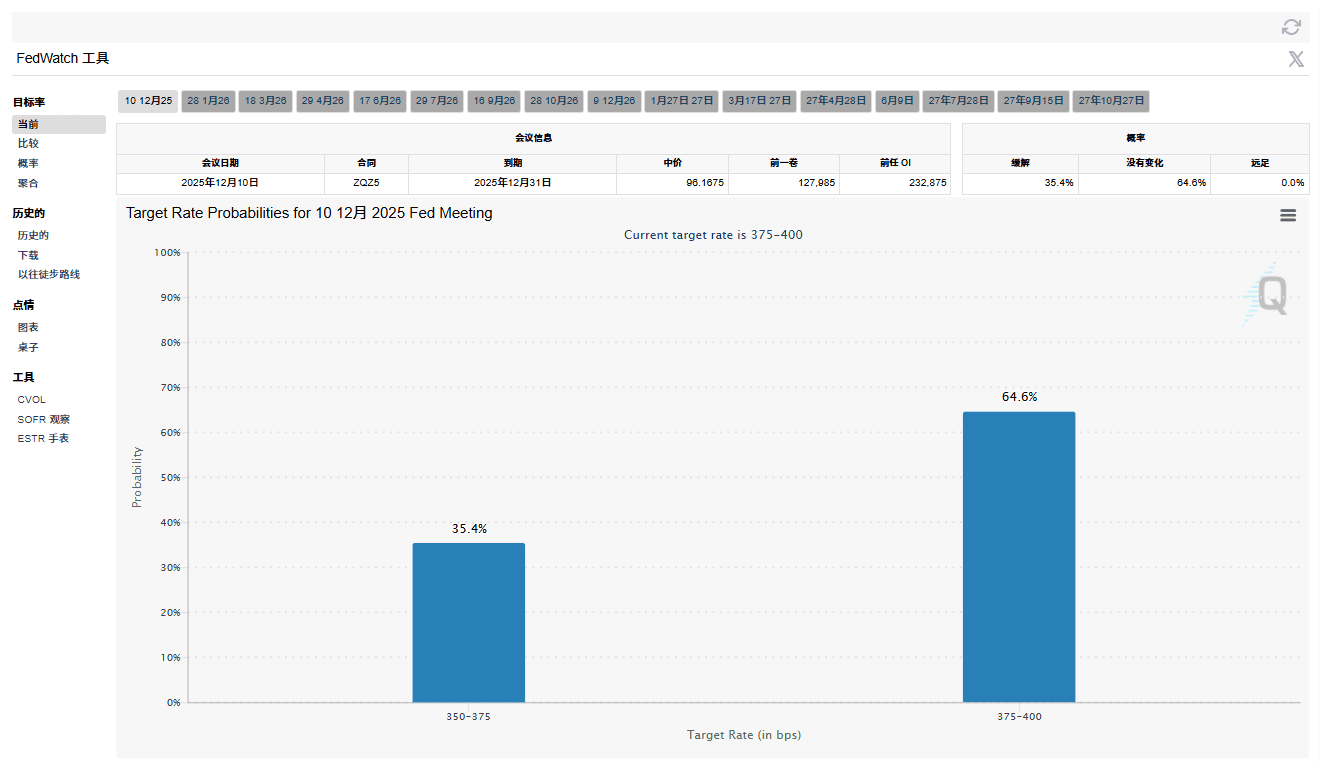

Current consensus: When will the interest rate cuts and balance sheet reduction end?

1. The pace of interest rate cuts: In the October meeting, it was passed with a vote of 10 to 2 to cut interest rates again by 25 basis points, lowering the target range for the federal funds rate to 3.75%–4.00%.

There is a clear divergence regarding whether to continue cutting interest rates in December. This latest non-farm data is not particularly friendly for a rate cut in December. The overall future tone is interest rate cuts and gradual easing, but in the short term, it is filled with uncertainty and even a lower probability of rate cuts. (Negative due to uncertainty)

2. Balance sheet reduction (quantitative tightening) is nearing its end (positive).

Institutions generally believe that starting in 2026, the Federal Reserve will be roughly in a phase of 'ending balance sheet reduction + slowly decreasing interest rates.'

For risk assets (U.S. stocks, crypto), the pressure of 'continued liquidity withdrawal' has decreased. If the market has money, it will eventually develop its own independent market.

The aforementioned technical aspects suggest that the market may see a reverse purchasing power, but at the same time, it indicates that it will not immediately bottom and may continue to decline. The downward structure technically needs favorable macroeconomic news to adjust the market. The question is, although we already know that the balance sheet reduction will officially stop on December 1st, the news of interest rate cuts remains uncertain for the market. In this structure, most institutions have chosen to pull back funds and wait for market adjustments to end or for the macroeconomic market direction to be confirmed.

For institutions, the darkness before dawn is difficult to endure. Therefore, the best approach is to abandon the left side and choose the right side, doubling down in the market once the macro direction emerges.

Therefore, the future direction and the views of institutions are quite crucial, as their actions will inevitably represent a direction for future market trends. I will express my views on how the direction should go in the second article.