The most important thing this month is the timing of the U.S. government's reopening, which is expected to be next Monday, October 17, U.S. time. This is faster than previously anticipated. Therefore, the September employment report can come out next week, and the October and November employment reports might be released on December 8, just before the rate cut meeting.

So this data will directly affect the Federal Reserve's rate cut pace. It was mentioned in the document on November 5 that there are two positives: one is that once the Treasury's TGA account is opened, there will be a cash inflow into the market; the other is the rate cut in December, although the rate cut depends on the data, as there are 'expectations' involved, so there might be one last effort, and we can only wait patiently.

Next, let’s discuss a significant event today: DEX-UNISWAP has announced the opening of the "fee switch". This event has had proposals in the past but was never passed, primarily due to legal and regulatory issues, as opening it might be recognized as a security by the SEC, hindering Uniswap's development. However, with the current favorable pro-crypto policies, the situation has relaxed, allowing the switch to be opened.

First, let’s popularize the "fee switch" concept. Because it is a decentralized exchange, to attract liquidity providers (LPs), incentives must be given. Previously, Uniswap’s fees were almost entirely allocated to LPs, with nothing retained for the protocol. Thus, the opening of the fee switch means that a portion of the protocol's fees will go to the protocol, rather than being fully distributed to LPs.

Another major criticism of Uniswap has been the "value capture" ability of the UNI token, i.e., the product is the product, and the token is the token, with no significant correlation, and UNI tokens themselves only have governance capability at most, empowering too much.

After enabling this switch, it can create empowerment, such as using protocol revenue to buy back tokens, creating deflation. Once the protocol has income, won't the team work harder?

The specific contents of this proposal are as follows, totaling 8 points:

1. Enable protocol fees and use them to burn UNI tokens;

2. Send Unichain sequencer fees to UNI burn address;

3. Burn 100 million UNI from the treasury, these UNI represent the protocol fees that would have been burned if the fee mechanism was enabled at the time of token issuance;

4. Introduce protocol fee discount auctions, which is a new way to enhance liquidity providers (LP) returns and internalize maximum extractable value (MEV);

5. Introduce an "aggregator hook" to transform Uniswap v4 into an on-chain aggregator for collecting protocol fees from external liquidity sources;

6. Labs is committed to promoting protocol growth and adoption, including signing contracts and pledging to only undertake projects that align with Uniswap governance interests. As part of this, Labs will stop charging fees for its interface, wallet, and API to significantly promote the distribution and adoption of the Uniswap protocol;

7. Transfer foundation activities to Labs, jointly committed to accelerating protocol development, with funding coming from treasury growth budget allocations;

8. Transfer the liquidity held by governance to the v4 version of Unichain and burn LP positions.

First, let's grasp the concept of immediately burning 100 million UNI tokens. Currently, the total supply of UNI is 600 million, which corresponds to 16.6% of the total supply, and further continuous burns will occur, resulting in deflation.

Current status of Uniswap's protocol fees across versions:

1. Uniswap V2

Fee rate and distribution mechanism

In V2, a default fee of 0.30% (i.e., 30 bps) is charged on each transaction.

The fees are instantly received by liquidity providers (LPs) based on their share in the pool. Specifically, the fees are automatically added to the pool's reserves, thereby increasing the value corresponding to the liquidity share.

Currently, most V2 pools have not enabled the "protocol fee switch", meaning all fees essentially go to LP.

If the protocol initiates the protocol fee, then a part may be deducted from the 0.30% for the protocol, resulting in a smaller amount for the LP. For instance, in official discussions, it was mentioned that if the protocol fee is initiated, possibly 0.05% is allocated for the protocol, leaving 0.25% for the LP.

2. Uniswap V3

Fee rate and distribution mechanism

V3 introduced multiple fee tiers for each trading pair, allowing LPs/trading pairs to select different fees based on their risk/liquidity characteristics.

Common fee rates include: 0.01% (1 bp), 0.05% (5 bps), 0.30% (30 bps), 1.00% (100 bps).

In V3, LP not only selects the fee rate but also chooses the price range to provide liquidity => Fees earned are only distributed when trades are activated within the price range they provided (i.e., trades enter the range they provided).

Regarding protocol fees, in V3, they can also be set for each pool, but most pools are still at 0 and not enabled.

How fees are distributed to LPs

When a swap occurs, the fees paid by the trader will be added to the pool's reserves and tracked through global state variables (like feeGrowthGlobalX128).

LP's fee share = "The liquidity provided by this LP in their selected range" ÷ "Total active liquidity in the pool at that range" × Fees generated when trades occur in that range.

If the price moves out of the range selected by the LP, that LP will not earn fees from new swaps during that period because their liquidity is "inactive".

Protocol fee portion

In the governance mechanism of V3, the protocol can set a proportion to withdraw a portion from swap fees as protocol fees, leaving the remainder for LP.

For example, the document states: If the setFeeProtocol parameter is set to N = 10, then the protocol fee rate is 1/N = 10%, meaning if the pool fee rate is 0.30%, the protocol fee is 0.03% (3 bps), and LP gets 0.27%.

3. Uniswap V4

Uniswap v4 supports variable fee rates: pools can adjust fees based on market conditions (like volatility, trading volume, blocks/each trade) up or down. Uniswap v4 pools can set any fee rate.

Estimated protocol revenue

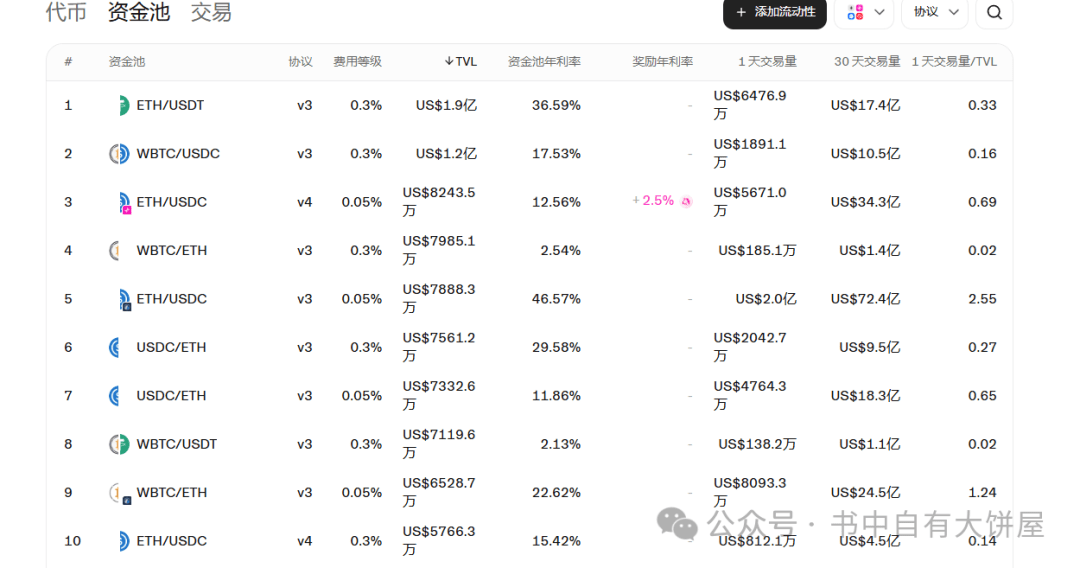

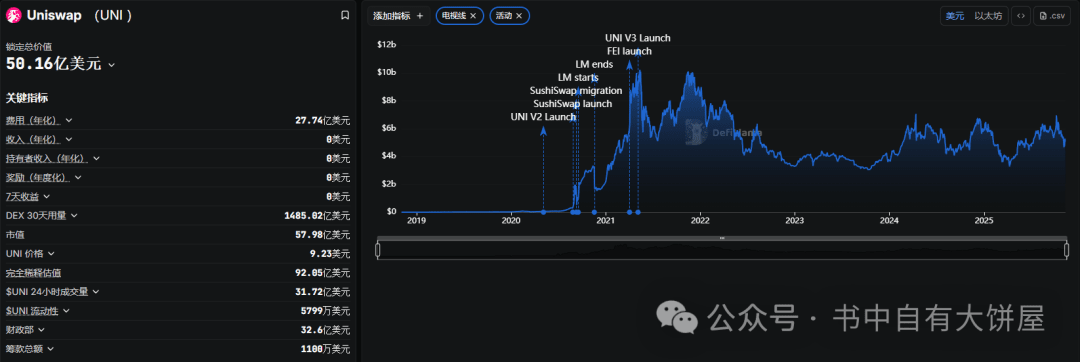

Currently, Uniswap’s total TVL is 5 billion USD, with data showing a 30-day DEX trading volume of 148.5 billion. If calculated at the V2 version rate of 0.05% (since V3 and V4 are variable), then the 30-day protocol revenue = 1485 * 0.05% = 74.25 million USD, which amounts to 890 million USD a year. Of course, due to the actual V2 pool having only 1.5 billion FDV, V3 having 2.6 billion, and V4 having 800 million, and because the income of V3 and V4 is dynamic, it should be lower than 0.05%. Therefore, conservatively estimating the income would still be around 500 million USD!

Of course, this revenue might be compared to centralized exchanges like Binance, where it could correspond to Binance's weekly fee income.

Even if this 500 million USD is not entirely used for buybacks and burns, but only 20% of it is used, that would still amount to 100 million USD a year. Currently, UNI's overall market capitalization is only 5 billion, with a total FDV of only 8 billion, expected to have a burn ratio of 1.25%. In comparison to BNB, which has a market cap of 130 billion and burns around 1 billion each quarter over 25 years, accounting for 3%. Though there is a certain gap, at least the first step has been taken.

In conclusion, the opening of this "fee switch" is undeniably a huge benefit. Of course, some might say that enabling the switch could diminish LP enthusiasm, but you should know that the current Uniswap is the largest ETH DEX. Compared to the lost 10% benefit, where else can you find such a substantial place with better liquidity? Moreover, if the project team actively improves the product and attracts more users, the overall return for LPs might actually increase.$UNI