An epic market crash, an algorithmic stablecoin rumored to have 'crashed 38%', and a trading giant mired in technical doubts. When the smoke cleared, we were surprised to find that the truth of the story was not simply 'the stablecoin malfunctioned,' but could be an extreme stress test of centralized exchange infrastructure. The core issue of this event pointed directly at Binance.

1. Event Review: An illusion of a 35% 'de-peg'?

1. Event Review: An illusion of a 35% 'de-peg'?

On October 11, 2024, the cryptocurrency market encountered a 'black swan,' with the prices of core assets like Bitcoin plummeting dramatically. In this chaos, the stablecoin USDe issued by Ethena Labs became the eye of the storm in public opinion.

● Rumors of 'decoupling' spread rapidly: Data shows that USDe's price on decentralized exchanges like Binance once fell to 0.65 USD, deviating from the theoretical peg price of 1 USD by as much as 35%. Market panic spread instantly, and USDe's market value evaporated by over 2 billion USD in a short time.

● Investors urgently 'extinguish the fire': In the face of a trust crisis, Ethena's investors, led by top venture capitalist Haseeb Qazi, personally stepped in to rebut. He pointed out a fact that most people overlooked through detailed data analysis: USDe did not actually decouple; it was merely a 'local fire' occurring within the Binance exchange.

Was this ultimately a definitive failure, or a misinterpreted accident? All clues point to Binance.

2. In-depth analysis: Fragmented liquidity and a malfunctioning 'firefighting system'

Why do different trading venues show such huge discrepancies in USDe prices at the same moment? The answer lies in fragmented liquidity and the paralysis of market maker arbitrage mechanisms.

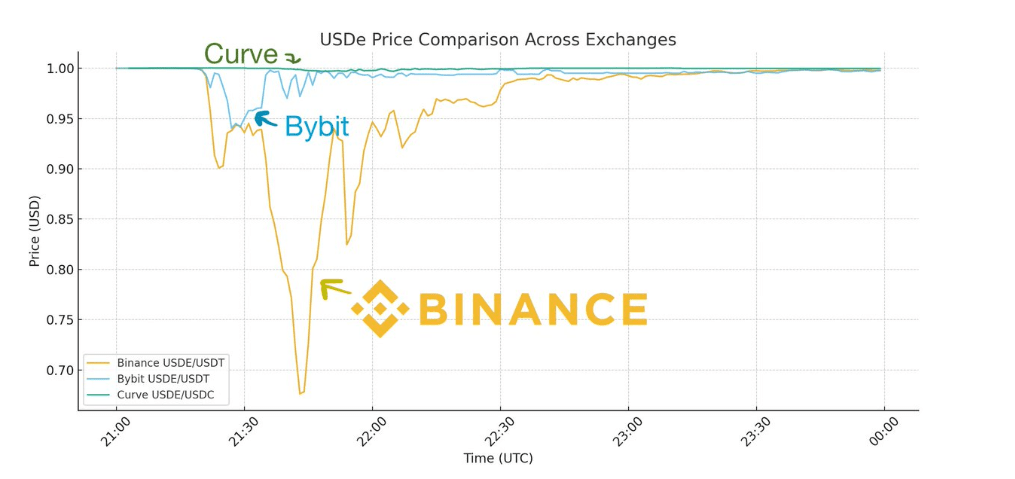

● The main battleground remains unscathed: Haseeb's core argument is that the primary liquidity pool for USDe is not on Binance, but rather on the decentralized trading protocol Curve. On Curve, USDe has hundreds of millions of USD in liquidity depth. Throughout the entire flash crash, USDe's price on Curve remained closely tied to 1 USD, with a maximum deviation of only 0.3%. This proves that its core redemption mechanism and market demand remain robust.

● Binance has become an 'island': In contrast, the liquidity pool for USDe on Binance is only a few tens of millions of USD. When the market crashes and a massive sell-off occurs instantaneously, the weak order book is easily breached. More critically, Binance's API interfaces frequently failed at the time, and the deposit and withdrawal channels were nearly paralyzed. This meant that even if there was sufficient 1 USD USDe on Curve, market makers could not arbitrage across markets by 'buying low on Binance and selling at parity on Curve'.

● A vivid metaphor: Haseeb compared Binance at the time to a 'burning building with all channels blocked'. The 'firefighters' outside (market makers and arbitrageurs), even if they saw huge arbitrage opportunities inside, could not enter to extinguish the fire. The result was that the 'fire' inside the exchange (price deviation) continued to spread, while the 'fire' outside had long been extinguished.

3. Binance's dual 'evidence': The collapse of infrastructure and risk models

If liquidity issues are natural disasters, then Binance's design flaws are unequivocal 'man-made disasters'. This incident exposed significant shortcomings in two key areas of Binance.

● Evidence 1: The inherent deficiency of lacking a 'primary market maker relationship'

Ethena established a primary market maker relationship with exchanges like Bybit, allowing market makers to directly mint and redeem USDe within the exchange to quickly stabilize price fluctuations.

However, Binance did not establish this relationship. On Binance, market makers must withdraw funds from Binance to conduct arbitrage, complete Ethena's official arbitrage process on-chain, and then deposit back into Binance.

In situations of extreme market volatility, network congestion, and API failures, this complex process cannot be executed at all. This made Binance a 'financial island' lacking internal stabilizing mechanisms.

● Evidence 2: Oracle flaws triggered a 'chain liquidation' tragedy

This is the most controversial point in this incident. Binance's liquidation system, when assessing the value of user collateral, only referenced the distorted USDe price on its own order book. When the internal USDe price at Binance suddenly plummeted to 0.8 USD or lower, Binance's risk system 'stupidly' assumed that all USDe collateral was worth only this price.

As a result, a large number of users who used USDe as collateral had their positions mistakenly judged as insolvent, triggering forced liquidations.

These forced liquidations further exacerbated the downward pressure on the market, creating a death spiral of chain liquidations. Ironically, Binance later admitted this was a fault of its system and announced full compensation for users who were mistakenly liquidated, totaling approximately 283 million USD. This move is tantamount to admitting the failure of its risk control model.

4. Insights and Warnings: When 'stability' relies on the exchange's 'unbroken chain'

The recent USDe turmoil leaves the industry with far more than just a war of words; it is a heavy warning.

● To exchanges: Infrastructure is the cornerstone of trust

As the industry leader, Binance's system stability affects the nerves of the entire market. This incident shows that competition among exchanges is not just about the number of listed coins and transaction fees, but more deeply about the robustness of infrastructure, the rigor of oracle design, and the intelligence of risk models. Any breakdown in one link could trigger a chain disaster. For Binance and its BNB ecosystem, this incident is a loss of trust.

● To project parties and investors: Re-examine the definition of 'stability'

For algorithmic stablecoin projects like Ethena, this incident is a severe test, but it also provides a counterexample. It proves that a project designed with ample collateral and sound arbitrage mechanisms can maintain stability in mainstream channels. However, investors must also clearly recognize that the 'stability' of any asset relies on the health of its trading environment. When you store assets in an exchange with weak infrastructure and fragmented liquidity, you expose yourself to additional risks.

● The mirror of history: True decoupling and price misalignment

As Haseeb compared, in 2023, when USDC decoupled due to the banking crisis, it could not be bought at a price of 1 USD on all trading venues, and the redemption mechanism was completely suspended. That was a true credit crisis and systemic decoupling. In contrast, the recent USDe incident is more like a local price misalignment caused by technical failures at specific exchanges. Recognizing this essential distinction is crucial for understanding the market truth.

Conclusion: The true 'black swan' may never have left.

Conclusion: The true 'black swan' may never have left.

The flash crash on 10.11 was an external shock, while the 'decoupling' illusion of USDe on Binance exposed a potential and more dangerous 'black swan' within the industry—the fragility of centralized exchanges' critical infrastructure.

When an exchange's API, oracles, and liquidation systems are overwhelmed under extreme market conditions, they turn from stabilizers of the market into amplifiers of risk. This time it was USDe and Binance; next time, who will it be? For every market participant, it's time to incorporate 'exchange infrastructure risk' into their core risk assessment framework.