Mitosis and the Future of Secondary Liquidity Markets

Liquidity has always been the beating heart of finance. In traditional markets, the depth of liquidity determines efficiency, stability, and opportunity. Yet liquidity does not exist only in primary markets. Some of the most influential developments in finance came from secondary markets — places where exposure to primary capital could be priced, traded, and reallocated dynamically. Derivatives, ETFs, and structured notes all emerged from the need to create flexible secondary layers around liquidity. These innovations expanded efficiency and created massive new industries.

In decentralized finance, secondary markets for liquidity are still underdeveloped. Liquidity pool tokens exist, but they are fragmented, bespoke, and often illiquid themselves. Yield-bearing tokens circulate, but they lack standardization and credibility, leaving their markets shallow. Governance tokens provide influence, but not exposure to underlying liquidity. DeFi has excelled at building primary pools of liquidity but failed to create thriving secondary markets around them.

Mitosis is poised to change this. By standardizing deposits into Hub Assets, embedding enforceable governance, and tokenizing liquidity positions into miAssets and maAssets, Mitosis creates the conditions for robust secondary markets. These are not secondary markets for governance votes or yield receipts alone. They are secondary markets for liquidity itself — modular, standardized, and programmable. In this vision, liquidity becomes a traded commodity, and secondary markets become the engines of efficiency that turn DeFi into a sustainable financial system.

Why secondary markets matter

Primary liquidity markets are where assets are first deposited, paired, or loaned. They provide depth but little flexibility. Once capital is deposited into a pool, it is stuck until withdrawn. LP tokens are receipts but lack fungibility and standardized value. This traps liquidity, reducing efficiency and preventing dynamic reallocation.

Secondary markets provide the missing flexibility. They allow participants to trade exposure to liquidity without withdrawing capital. They enable institutions to enter or exit positions without disrupting pools. They create opportunities for speculation, hedging, and arbitrage. In traditional finance, secondary markets are where efficiency is achieved and risk is managed. Without them, markets remain shallow and brittle.

In DeFi, the lack of standardized secondary markets has led to inefficiencies. Protocols must constantly bribe liquidity with new incentives. Users must lock capital without flexibility. Communities must fragment across ecosystems. By failing to develop credible secondary markets, DeFi has limited its own scalability.

Mitosis and standardized liquidity tokens

The foundation of secondary markets is standardization. Without fungible, credible tokens, liquidity exposures cannot be priced or traded at scale. Mitosis provides this standardization through Hub Assets and position tokens.

When users deposit into branch vaults, Hub Assets are minted on the hub chain. These are standardized ERC-20 tokens that represent liquidity in a universal form. When liquidity is directed into governance strategies, participants receive miAssets or maAssets, representing collective or structured exposures. All of these tokens are fungible, auditable, and enforceable through the settlement layer.

This standardization makes them suitable for secondary markets. Traders know what the tokens represent, how they are reconciled, and what outcomes they reflect. Institutions can integrate them into portfolios. Developers can build protocols that use them as collateral. Communities can trade them to reallocate influence. Standardization transforms liquidity tokens from opaque receipts into financial instruments.

Secondary markets for governed liquidity

The most novel aspect of Mitosis secondary markets is that they enable trading of governed liquidity itself. miAssets represent community-directed liquidity pools. maAssets represent structured campaigns with transparent rules. Both are tied directly to governance outcomes.

This allows participants to trade exposure not only to yield but to decision-making. If a community directs liquidity into a certain strategy, its miAssets will reflect the value of that choice. If traders believe the decision is strong, they may bid up the tokens. If they think it is weak, they may discount them. Governance outcomes become priced in real time by secondary markets.

This dynamic adds depth and discipline. Communities must consider how their decisions will affect token values. Traders can speculate on governance outcomes, creating new opportunities. Institutions can acquire influence by buying position tokens. Governance is no longer symbolic but liquid, priced, and enforced through markets.

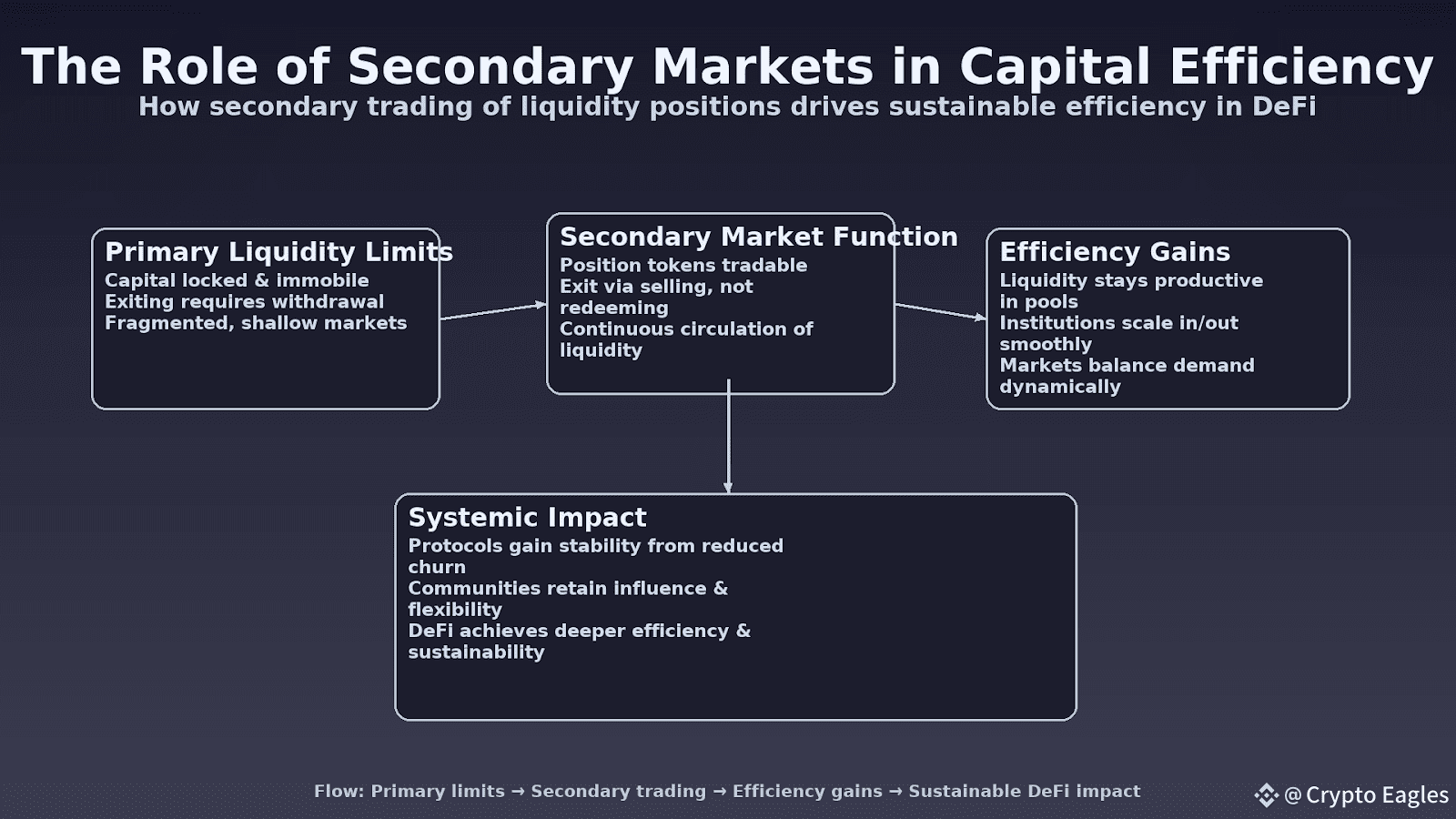

The role of secondary markets in capital efficiency

Secondary markets improve capital efficiency by allowing liquidity to circulate without being withdrawn. A user who wants to exit exposure does not need to redeem from the pool. They can sell their position tokens on the secondary market. Another user who wants exposure can buy without waiting for deposits

This circulation keeps capital productive. Liquidity does not have to flow in and out of pools constantly, reducing churn and slippage. Protocols benefit from more stable capital, as secondary markets absorb short-term demand shifts. Users benefit from flexibility, as they can adjust exposure dynamically. Institutions benefit from depth, as they can enter or exit positions at scale.

In this way, secondary markets extend the life and stability of primary liquidity. They become the safety valves and engines that make the system sustainable.

Secondary markets as innovation platforms

Once standardized position tokens exist, developers can build entire ecosystems on top of them. Derivatives can hedge against governance outcomes. Structured products can bundle different liquidity positions. Oracles can provide pricing feeds for decentralized prediction markets. Insurance protocols can underwrite risks associated with certain strategies.

Each of these innovations compounds composability. Position tokens become inputs for new systems, which in turn create new markets. Just as ERC-20 tokens unleashed an explosion of DeFi protocols, standardized liquidity tokens can unleash an explosion of secondary markets. The difference is that these markets are tied directly to capital flows and governance, making them more economically significant.

Institutional participation in secondary markets

Institutions thrive in secondary markets. They need predictable instruments, transparent pricing, and liquid exits. Mitosis provides these conditions. Hub Assets behave like standardized money-market instruments. miAssets and maAssets behave like structured products with governance backing. Settlement ensures reconciliation.

This gives institutions the confidence to enter secondary markets at scale. They can acquire exposure to governed liquidity without locking capital directly. They can integrate tokens into portfolios, use them as collateral, or trade them in structured markets. Institutions bring depth and stability, while secondary markets give them the flexibility they require.

The interaction between institutions and communities becomes particularly powerful. Communities retain governance, institutions provide capital, and secondary markets price the interaction. This balance creates a healthier ecosystem than systems dominated by mercenary capital or insider whales.

Risks of secondary markets

No secondary market is without risks. Liquidity could concentrate in certain tokens, creating systemic exposure. Speculation could drive bubbles, detaching prices from underlying value. Governance capture could occur if institutions accumulate too many tokens.

Mitosis mitigates these risks by enforcing transparency, standardization, and governance constraints. Position tokens are reconciled mechanically, preventing misrepresentation. Governance is enforced by settlement, preventing manipulation. Secondary markets operate on credible instruments rather than opaque receipts. While risks remain, they are manageable within the framework of enforceable architecture.

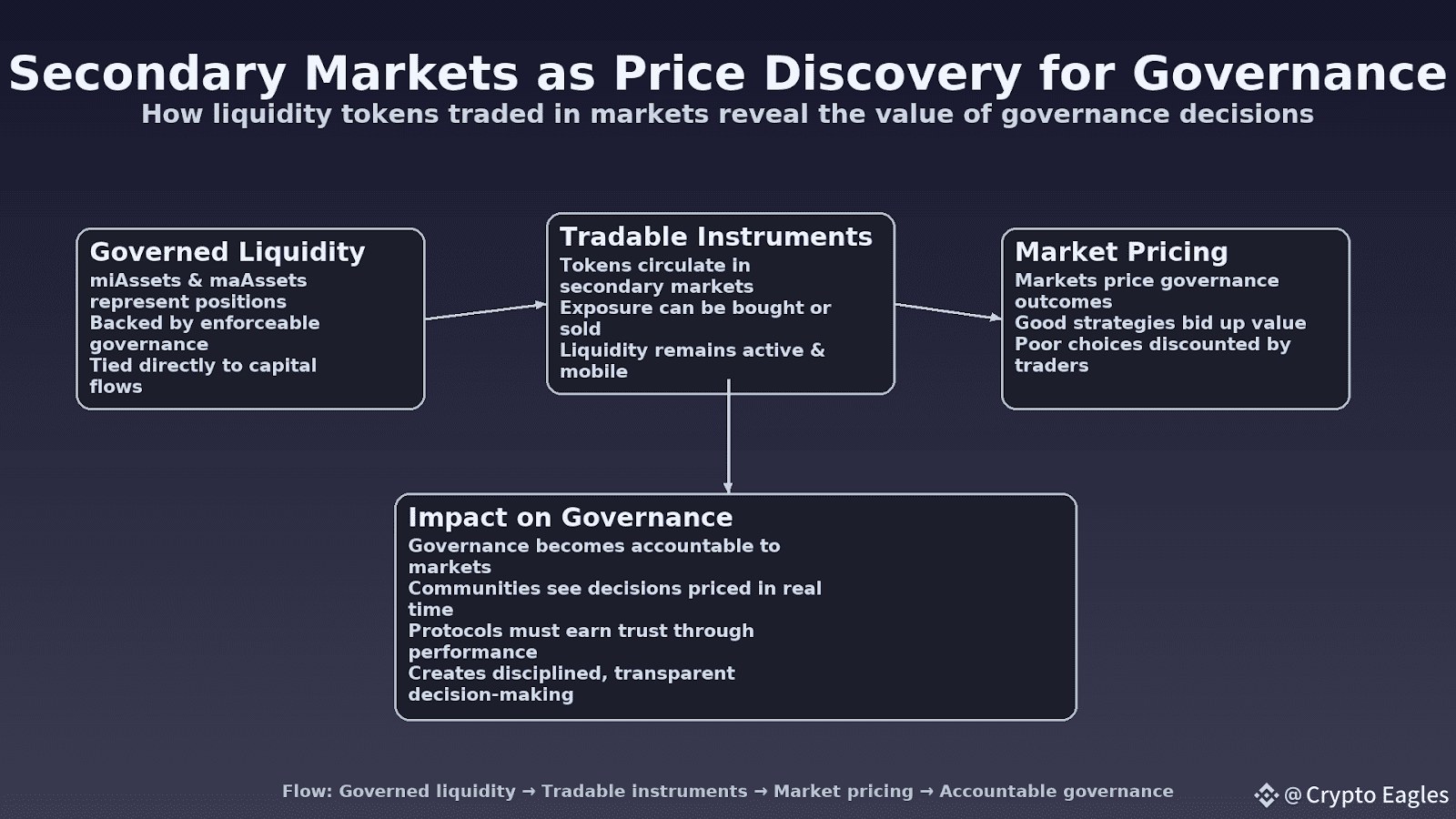

Secondary markets as price discovery for governance

One of the most transformative aspects of Mitosis secondary markets is that they provide price discovery for governance. Decisions are no longer hidden in forums or snapshots; they are priced in markets. Traders can see the market’s confidence in certain strategies reflected in token prices. Communities can measure the impact of their choices in real time. Institutions can evaluate governance outcomes through pricing signals

This creates a feedback loop. Governance is disciplined by markets, and markets are informed by governance. Poor decisions are punished, good decisions are rewarded, and communities learn through visible outcomes. Price discovery makes governance accountable in ways no forum or vote tally can achieve.

The vision of liquidity as a traded commodity

The long-term vision of Mitosis is a world where liquidity itself is a traded commodity. Hub Assets circulate as standardized instruments. Position tokens circulate as structured exposures. Secondary markets price, trade, and allocate these tokens dynamically. Developers build layers of innovation on top. Communities and institutions negotiate through markets.

In this vision, DeFi matures into a system where capital is not only pooled but circulated. Liquidity flows like energy across protocols, priced and allocated by markets rather than dictated by insiders. Governance is liquid, influence is tradable, and efficiency is achieved through circulation.

This vision mirrors the trajectory of traditional finance, where secondary markets created entire industries around derivatives, structured products, and asset-backed securities. But in DeFi, it is achieved transparently, programmatically, and collectively. Mitosis provides the architecture, and secondary markets provide the dynamism. Together, they form the future of liquidity economies.

Conclusion

The future of DeFi will not be built solely on primary pools of liquidity. It will be built on secondary markets that price, trade, and allocate liquidity dynamically. Mitosis makes this possible by standardizing deposits into Hub Assets, enforcing governance through settlement, and tokenizing liquidity into miAssets and maAssets. These tokens are not just receipts but instruments for secondary markets, capable of powering entire ecosystems of innovation.

Secondary markets are where efficiency is achieved, risks are managed, and value is created. With Mitosis, they become the foundation of a new financial architecture where liquidity itself is a traded commodity. This shift transforms DeFi from fragmented experiments into an integrated system of markets, where communities, institutions, and protocols all participate in the pricing and governance of capital.

Mitosis shows that the next great leap in DeFi will not come from another yield farm or incentive scheme, but from the creation of credible, standardized, and enforceable secondary markets for liquidity. In this future, liquidity is not just deposited; it is composed, traded, governed, and priced. That is the future Mitosis is building.