Author: Anthony Pompliano, Founder and CEO of Professional Capital Management; Translated by Golden Finance

As expected, the Federal Reserve announced yesterday a 25 basis point cut to the benchmark interest rate. Federal Reserve Chairman Jerome Powell subsequently held a press conference, but the information disclosed was, in fact, already rumored online months ago.

Powell stated at the press conference: “In the short term, inflation faces upward risks, while employment faces downward risks.”

Throughout the press conference, Powell's demeanor fully displayed a sense of 'frustration'. He neither showed enthusiasm for attending the press conference nor exhibited any passion for the current challenges faced.

The Federal Reserve finds itself in its current predicament largely due to a shift in its policy logic: in previous years, the Fed adhered to a 'data-dependent' principle (i.e., formulating monetary policy based on economic data), but recently it has leaned more towards acting as an 'economic forecaster.' Originally, it only needed to base monetary policy on existing economic data and real-time indicators, but the Fed has chosen to venture into the 'predictive realm,' even taking action based on the presumption that 'tariffs will drive up inflation.'

The fact is as I have predicted from the very beginning: tariffs are not a driver of inflation. The 'high inflation' that the Federal Reserve was previously concerned about has never materialized. This means that the Fed's predictions themselves were flawed, and its stance of 'maintaining high rates for a longer time' is naturally untenable.

However, the Federal Reserve's situation is more complex than it appears on the surface—its board members have significant disagreements on the core issue of 'how current rates should be adjusted.' Navy Federal Chief Economist Heather Long interpreted this as follows:

'The situation is simply outrageous. Just look at the predictions of the 19 Federal Reserve officials regarding interest rate trends for the remainder of 2025; it is evident from just one chart that there is internal tension within the Federal Reserve:'

1 person advocates for an interest rate hike; 6 believe the current rate should remain unchanged; 2 support another rate cut; 9 lean towards two more rate cuts; and 1 person (presumably Stephen Miran, a recent appointee by Trump) advocates for a total equivalent to 5 rate cuts by the end of the year.

Currently, it seems likely that the Federal Reserve will cut rates two more times, in October and December. But clearly, the future game around interest rate policy will continue...

Imagine how extreme this divergence is: some were advocating for an interest rate hike yesterday, while others hope for five rate cuts by the end of the year. The members not only cannot reach a consensus on the 'number of rate cuts,' but there is even a fundamental opposition on whether 'rates should be raised or cut now.'

This phenomenon precisely highlights the inherent problem of 'human-led monetary policy': allowing individuals to control 'funding costs' (i.e., interest rates) is essentially impossible because humans often have limitations when making complex decisions. Moreover, the Federal Reserve's decisions are made collectively by a committee, making the decision-making process even more difficult—'collective decision-making' often leads to poor decisions as a 'necessary path.'

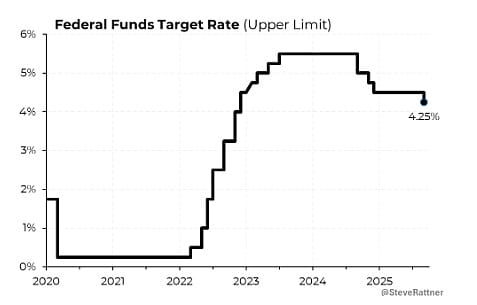

Worse still, if we look back at the interest rate trends since 2020, we find that the fluctuations are 'completely irregular.' Facing such great uncertainty, how should ordinary people plan their lives?

In just five or six years, funding costs have fallen from 2% to 0%, then surged to over 5%, and subsequently dropped back to around 4%—such volatility is indeed difficult to cope with. In fact, this unnecessary drastic fluctuation could have been avoided.

In contrast, Bitcoin: its monetary policy has not deviated from the track of 'programmatic monetary policy' since it was established in 2009, remaining consistent for 15 years. In my view, the Federal Reserve could fully learn from Bitcoin's mechanisms.

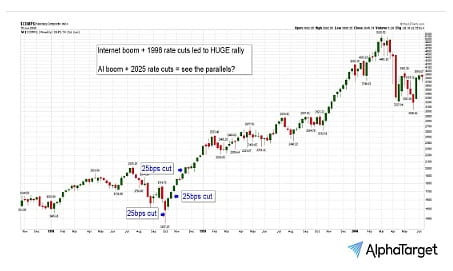

It is worth noting that in 1998, the Federal Reserve cut rates by 25 basis points, which subsequently fueled the crazy rise of tech stocks during the 'Dot Com Boom.'

As Puru pointed out, the current situation bears an astonishing similarity to 1998: the Federal Reserve is implementing rate cuts during the 'AI-related innovation boom.' If the Fed, as stated yesterday, cuts rates multiple times within this year, the stock market is likely to experience a significant surge.

Objectively speaking, the Federal Reserve's policy has always been 'behind the market curve.' Yesterday, they chose to 'retreat' and only cut rates by 25 basis points, which serves as an example. But for investors, this conservative move may ultimately be inconsequential—currently, the market is generally on an upward trend, so one only needs to hold assets and enjoy this wave of market movement.