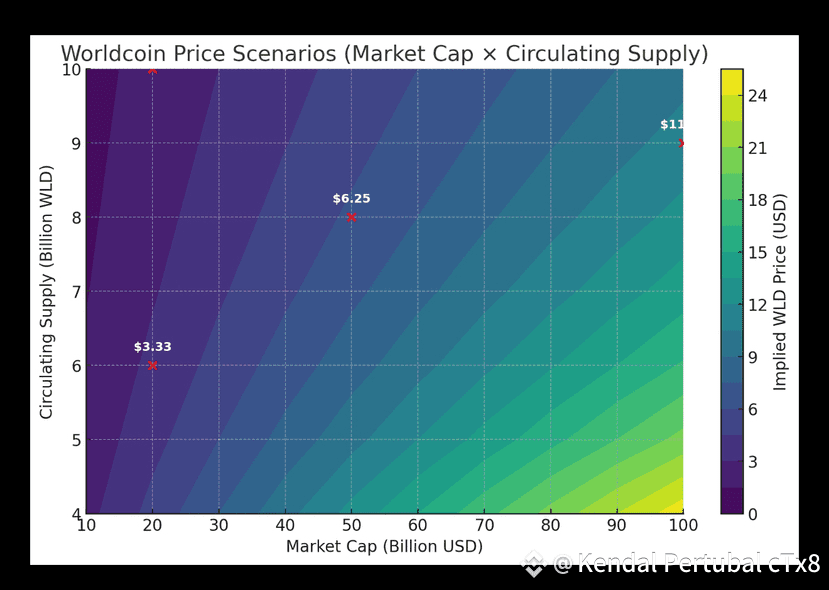

Base case: If WLD gets to a $20B market cap with ~6B circulating, price ≈ $3.33 (~1.7× from ~$1.93).

Optimistic: $50B cap with ~8B circulating gives ≈ $6.25 (~3.2×).

Cycle peak (aggressive but not crazy for a top-20 coin): $100B cap with ~9B circulating yields ≈ $11.1 (near its prior ATH; ~5.8×).

Dilution risk check: At $20B cap but 10B circulating (heavy unlocks), price is only ≈ $2.00 (flat vs now).

→ This shows how much supply expansion matters for upside.

How high can it go vs similar “big-supply, high-volume” coins?

Rather than cherry-picking peers, the cleanest way is this market-cap lens:

If WLD matures into a mid-tier L1/infra-style valuation (~$20–30B), you’re likely in the $2–$4.5 zone depending on how fast circulating supply climbs.

If it earns top-tier, cycle-frothy valuations (~$50–100B) and supply doesn’t fully saturate (≤8–9B out), you get a path to $6–$11.

Beyond $100B requires mainstream adoption + regulatory wins → mathematically still possible, but that’s the bull-of-all-bulls case.

Catalysts vs risks (why it would/ wouldn’t reach those caps)

Catalysts

Real-world identity integrations (exchanges, fintech, social apps) → utility + network effects

Institutional treasury/ETF-like attention → multiple expansion

Better privacy/compliance tooling → fewer regional shutdowns

Risks

Regulatory pushback on biometrics / data flows (cap on distribution + sentiment)

Token unlocks & emissions → headwind on price if demand doesn’t outpace new supply

Competing identity standards gaining traction