Written by: Anthony DeMartino - ADM

Compiled & Edited by: Janna, ChainCatcher

Since the beginning of this year, digital asset treasury companies have emerged as typical representatives in the wave of coin-stock integration, showing rapid growth momentum. However, these treasury-type companies have also exposed certain vulnerabilities while injecting liquidity into mainstream assets like Bitcoin and Ethereum.

This article originates from an analysis by Anthony DeMartino, founder of Sentora and general partner at the venture capital firm Istari, regarding the potential risks behind the prosperity of the DATs sector.

The original text is as follows:

In 2025, a new type of publicly listed company has attracted widespread attention from investors: Digital Asset Treasuries (DATs). These entities typically use cryptocurrencies like Bitcoin as core reserve assets, raising over $15 billion in funds this year alone, surpassing the scale of traditional venture capital in the crypto space. This trend has been spearheaded by companies like MicroStrategy and is gradually gaining momentum, with more enterprises accumulating digital assets through the public market. Although this strategy has generated significant profits during bull markets, it also contains inherent risks that could lead to painful liquidation waves, further amplifying volatility in both the stock and crypto markets.

(One) Operating Model of DATs

The establishment of DATs typically relies on innovative financing structures, including reverse mergers with NASDAQ-listed shell companies. This method allows private entities to go public quickly without undergoing the rigorous scrutiny of a traditional IPO. For example, in May 2025, Asset Entities and Strive Asset Management established a treasury company focused on Bitcoin through a reverse merger.

Other cases include: Twenty One Capital, supported by SoftBank and Tether, which created a $3.6 billion Bitcoin investment vehicle through a reverse merger with Cantor Equity Partners. After going public, these companies will raise funds through stock issuance and invest nearly all of the raised funds into digital assets. Their core mission is very clear: to buy and hold cryptocurrencies like Bitcoin, Ethereum, SOL, XRP, and even TON.

This model facilitates the intersection of traditional finance and cryptocurrency, providing investors with investment vehicles that offer 'leveraged exposure' without having to directly hold assets.

(Two) Rising Stock Prices and Premium Trading

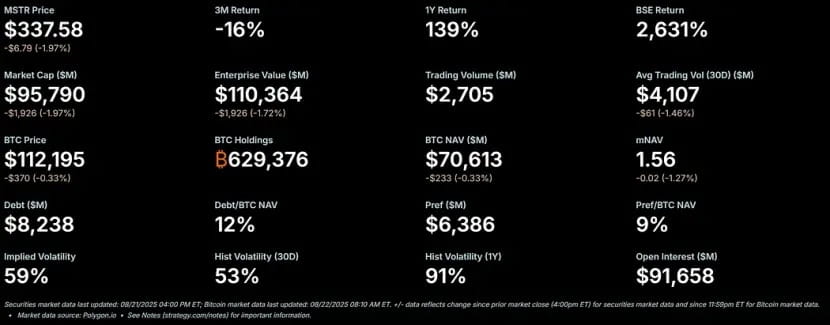

During the crypto bull market, DATs' stocks tend to rise significantly, often trading at a substantial premium to their net asset value (NAV). As a benchmark company for this model, MicroStrategy's stock price had a premium over its Bitcoin NAV exceeding 50%, and its multiple NAV (mNAV) ratio recently reached 1.56.

This formation of a premium stems from multiple factors: first, these companies can access low-cost public market funding; second, investors' enthusiasm for leveraged bets on cryptocurrencies; third, the market views these companies as vehicles to amplify stock returns.

When the stock price is above NAV, the dilution effect for shareholders from raising $1 will be lower than the value increment gained from asset purchases, thereby forming a virtuous cycle. In 2025, publicly listed companies and investors cumulatively acquired over 157,000 Bitcoins (worth over $16 billion), further propelling this momentum. Stocks of companies like Metaplanet, Bitmine, and SharpLink have all seen significant increases, often exceeding the price rises of their underlying cryptocurrencies.

(Three) Leveraging: Adding Fuel to the Fire

As premiums persist, DATs typically use leverage to amplify returns. They may issue convertible bonds or increase stock issuance to buy more digital assets, essentially borrowing against future appreciation. For instance, MicroStrategy has extensively used convertible notes, with its debt constituting 11% of its Bitcoin NAV.

This strategy amplifies returns in an uptrend but poses significant risks for companies in a down market. Leverage reduces a company’s resilience to shocks, potentially triggering margin calls or forced selling. Its appeal is evident: in a rising market, leverage can convert moderate cryptocurrency gains into explosive stock performance. However, the inherent high volatility of digital assets can lead to rapid depreciation in asset values.

(Four) Inevitable Decline: From Premium to Discount

The high volatility of the crypto market is well known; when cryptocurrency prices fall, DATs' stock prices may drop even more. If the price declines too rapidly or market confidence in such companies wanes, the premium on stock prices relative to NAV may quickly shift to a discount. Leverage positions further exacerbate this issue: a decline in NAV may force companies to de-risk, creating a volatility trap where bets that originally amplified returns may instead lead to greater losses for holders.

A stock price discount relative to NAV implies market skepticism regarding the company's asset management capabilities or ability to cover operational expenses during periods of asset value decline. Without intervention, this may lead to a chain reaction: loss of investor confidence, rising borrowing costs, and potential liquidity crises.

(Five) Choices in Crisis: Three Paths Forward

Assuming a DAT has sufficient cash reserves to cover operational expenses, when trading at a discount, it primarily faces three choices:

1. Maintain the status quo: the company continues to hold assets, waiting for the market to rebound. This approach can preserve cryptocurrency holdings but may lead to long-term dissatisfaction among shareholders, thereby exacerbating the decline in stock prices. So far, Strategy Company has maintained its Bitcoin holdings without selling during multiple bear markets.

2. Peer Acquisitions: If the discount widens significantly, some speculative buyers (typically other DATs) may acquire the company at a low price, essentially buying its underlying tokens below market value. This would promote industry consolidation but also preemptively release demand, weakening new buying flows, which is also one of the core drivers of the current upward trend.

3. Sell assets to repurchase shares: the company's board may sell part of its digital assets to repurchase shares, in order to narrow the discount and restore the stock price to a state of parity with NAV. This approach can actively manage the dynamics of premiums and discounts but essentially involves selling cryptocurrencies when the market is weak.

These three options highlight the fragile balance between asset preservation and shareholder value.

(Six) Selling Pressure: Motivation and Impact

DECISION-MAKERS in DATs often receive stock as their primary form of compensation. While this links their interests to stock performance, it also leads them to favor short-term solutions. As personal wealth is directly tied to stock prices, when stock prices experience a discount, the board faces significant pressure, tending to favor a strategy combining asset sales with stock repurchases.

This incentive structure may lead companies to prioritize short-term NAV parity over adhering to a long-term hold strategy, resulting in hasty decisions that contradict the original logic of reserve assets. Critics argue that this mechanism is similar to the historical asset cycle of 'prosperity to depression', where leveraged bets ultimately collapse in a devastating manner. If multiple companies simultaneously choose this strategy, it could trigger a chain reaction, leading to broader market turmoil.

(Seven) Broad Impact on Cryptocurrency Prices

The process of DATs stock prices shifting from a premium to a discount could have profound effects on the underlying cryptocurrency prices and often creates a negative feedback loop: when companies sell tokens to repurchase shares or cover leverage, they inject additional supply into an already declining market, exacerbating the price drop. For instance, banking analysis warns that if Bitcoin's price falls more than 22% below the average purchase price for companies, it could trigger forced selling.

This could trigger systemic risks: the behavior of large holders may affect market dynamics, amplify volatility, and potentially lead to cascading liquidations. However, some data indicates that corporate holdings have a relatively small direct impact on prices, and the market may overestimate the influence of digital asset treasury companies.

Nevertheless, in a high-leverage ecosystem, coordinated selling may further depress asset values, hinder new players from entering the market, and extend the bear market cycle. As the DAT trend matures, its liquidation wave may test the resilience of the entire crypto market, transforming the current prosperity of reserve assets into a cautionary tale for the future.

(Eight) Which Tokens Will Be Most Affected by the Discount Transformation?

Since the beginning of 2025, DATs focused on Ethereum have become important participants in the crypto ecosystem. They have accumulated large amounts of Ethereum (ETH) holdings through public market financing. While this has driven up Ethereum prices during bull markets, this model introduces additional risks during bear markets: when DATs' stock prices shift from a premium NAV to a discount NAV, boards may face pressure to sell Ethereum to finance stock repurchases or cover operational expenses, which could further exacerbate the price drop of Ethereum. The following analysis will combine historical context, current holdings, and market dynamics to assess potential price bottoms for Ethereum in such scenarios.

(Nine) Historical Background: Price Trends Before and After the First DAT Announcement for Ethereum

The first DAT announcement focused on Ethereum was made by BioNexus Gene Lab Corporation on March 5, 2025, marking the company's official transformation into an Ethereum asset strategy company listed on NASDAQ. Prior to this, on March 4, 2025, Ethereum's closing price was approximately $2,170, reflecting the market's consolidation amid widespread uncertainty following the 2024 bull market.

As of August 21, 2025, the price of Ethereum is approximately $4,240, reflecting an increase of about 95% since the announcement. In contrast, BTC's increase during the same period was only 28%. Additionally, the ETH/BTC exchange rate also hit a peak in 2025 (exceeding 0.037), highlighting Ethereum's outperformance.

This wave of Ethereum's rise is driven by multiple factors, including inflows from spot Ethereum ETFs (over $9.4 billion since June), rising institutional adoption, and the enterprise buying brought about by the DAT trend itself. However, a significant portion of this increase is attributed to speculative capital inflows related to the DAT narrative, making a correction likely.

(Ten) Company's Ethereum Holdings and Supply Proportion Since the Start of the DAT Trend

Since BioNexus's announcement kicked off the Ethereum DAT wave, publicly listed companies have begun actively accumulating Ethereum as a reserve asset. As of August 2025, approximately 69 entities hold over 4.1 million Ethereum, valued at around $17.6 billion. Major participants include: BitMine Immersion Technologies (valued at $6.6 billion as of August 18), SharpLink (728,804 ETH), ETHZilla (approximately 82,186 ETH), Coinbase, and Bit Digital.

These companies hold over 3% of the total supply of Ethereum. Since the DAT trend for Ethereum began in March 2025, there had been almost no publicly listed companies using Ethereum as a reserve asset. For example, Coinbase's Ethereum holdings were primarily for operations, not strategic reserves. This 3.4% holding is essentially the new acquisition volume since the initiation of the DAT trend. If institutional and ETF holdings are taken into account, the institutional holding ratio of Ethereum is approximately 8.3% of the total supply, but the recent accumulation of core drivers still stems from enterprise buying related to DATs.

(Eleven) Price Drop Predictions for Ethereum When DATs Trade at a Discount

During bull markets, DATs' stock prices often carry a premium to NAV; however, in bear markets, the previous premium may reverse to a discount of 20%-50%, triggering three response paths: maintaining the status quo, being acquired, or selling assets to repurchase shares. Due to executive compensation tied to stock performance, they are more likely to sell Ethereum to narrow the discount, injecting additional supply into the market. For Ethereum, such selling may create a negative feedback loop, especially considering the concentration characteristics of a few companies holding large amounts of Ethereum.

1. Benchmark Scenario (Mild Discount, Partial Selling)

If Ethereum enters a retracement phase due to macroeconomic factors (such as rising interest rates) and the stock price of DATs falls to a discount of 10%-20%, companies may sell 5%-10% of their Ethereum holdings (approximately 205,000 - 410,000 ETH, valued at $870 million - $1.74 billion at current prices) to raise funds for stock repurchases. The average daily trading volume of Ethereum is around $15 billion - $20 billion, so this portion of selling may create 5%-10% downward pressure, causing the price to drop to $3,600-$3,800 (a decline of 10%-15% from the current $4,240). This scenario assumes that companies gradually sell off through over-the-counter (OTC) trading to minimize slippage.

2. Severe Scenario (Deep Discount, Coordinated Selling)

If the crypto market enters a full bear market (where premiums completely disappear and discounts widen to 30%-50%), multiple DATs may initiate liquidations simultaneously—especially if leverage positions (like convertible bonds) compel them to de-risk. If 20%-30% of corporate Ethereum holdings (approximately 820,000 - 1,230,000 ETH, valued at $3.5 billion - $5.2 billion) flood the market within a few weeks, it could exceed the market's liquidity capacity, causing prices to drop by 25%-40%. At that time, Ethereum prices could fall to $2,500-$3,000, approaching levels seen before the initiation of the DAT trend, but would not completely revert—thanks to ETF funding support and on-chain growth (for example, Ethereum's average daily trading volume reached 1.74 million transactions in early August). Taking into account the historical instances of institutional selling amplifying declines during the 2022 bear market and considering the current concentration of 3.4% in corporate holdings, Ethereum's volatility could further escalate.

3. Worst Case Scenario (Complete Liquidation)

If regulatory scrutiny intensifies (such as the U.S. SEC taking action against treasury companies) or a liquidity crisis erupts, forcing companies to sell off Ethereum on a large scale (potentially selling over 50% of their holdings, which is over 2 million ETH), the price could plummet to $1,800-$2,200, completely erasing the gains made since the initiation of the DAT trend and testing the 2025 low. However, the probability of this scenario occurring is relatively low due to factors such as potential peer acquisitions absorbing some supply, and the ETF holdings, which account for 8% of the total supply, providing a certain buffer.

The above predictions have taken into account the improvement in Ethereum's fundamentals, such as the accumulation of 200,000 ETH by whales in the second quarter of 2025, but still highlight specific risks associated with DATs. Ultimately, the extent of Ethereum's price decline depends on the scale of selling, market depth, and external catalytic factors, but in a scenario driven by discount-induced liquidation, a price retreat to the $2,500-$3,500 range is reasonable, exposing the fragility of the DAT model.